According to recent data from the Centers for Disease Control and Prevention (2026), the average 65-year-old American can expect to live another 19.7 years. That translates to roughly two decades of waking up on a Tuesday morning with the absolute freedom to decide exactly how you want to spend your time. Yet, the old cliché of a sudden “hard stop”—trading your briefcase for a golf club and never looking back—is fading quickly. Today’s older adults are actively constructing dynamic, multi-chapter routines that seamlessly blend leisure, meaningful work, and proactive health management.

Going from a structured forty-hour workweek to zero obligations can be profoundly jarring. Without the built-in social network of an office or the clear objectives of a career, many new retirees find themselves adrift. Fortunately, the blueprint for a successful post-career life has evolved. Retirees in 2026 are proving that this phase of life is less about slowing down and more about intentional pacing.

The Rise of “Unretirement” and Purpose-Driven Work

For decades, society viewed retirement as a permanent exit from the workforce; however, working in your later years is now widely embraced as a lifestyle choice that provides mental stimulation, social interaction, and vital financial padding. A February 2026 survey by AARP revealed that 7% of retirees had actively reentered the labor force within the previous six months alone, with basic expenses being the primary driver for many.

Many find that transitioning to a part-time role, consulting, or picking up app-based gig work offers the scheduling control they never enjoyed during their peak earning years. Earning extra income also serves as a powerful buffer against rising living costs. If you choose to blend work and retirement, you unlock several distinct advantages:

- Maintaining cognitive sharpness: Tackling new challenges, learning updated software, and solving problems in a work environment keeps your mind agile and engaged.

- Delaying portfolio withdrawals: Earning enough to cover your basic living expenses allows your retirement accounts to continue growing tax-deferred, reducing the risk of outliving your money.

- Expanding social circles: Work naturally forces you to interact with people from diverse age groups and backgrounds, which combats the isolation that often accompanies the transition out of a primary career.

- Testing a passion project: Many retirees use this time to monetize a hobby or consult in a field they always found fascinating but never had the time to pursue.

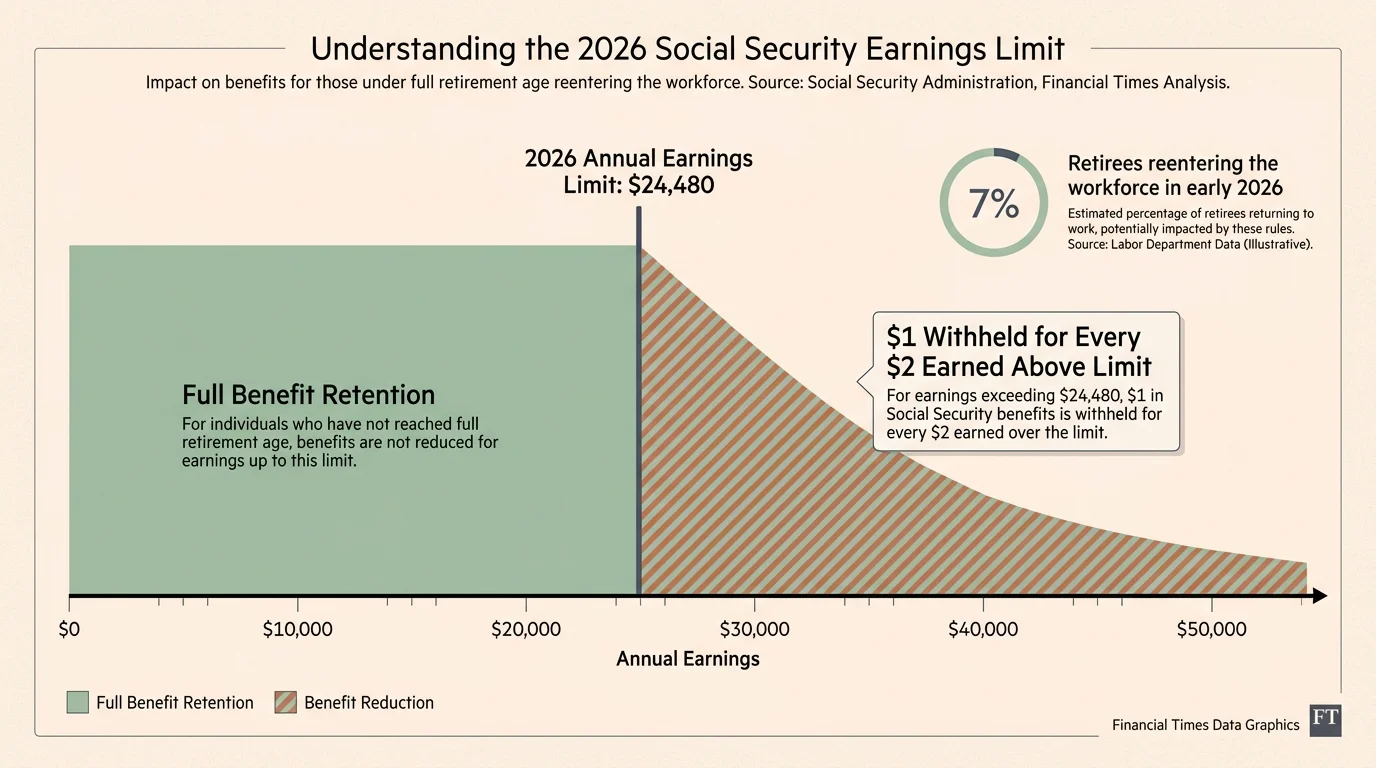

Before you jump back into the workforce, you need to understand how earned income impacts your government benefits. If you are under your full retirement age in 2026, the Social Security Administration allows you to earn up to $24,480 before your benefits are temporarily reduced—meaning $1 is withheld for every $2 earned above that specific limit. Once you reach full retirement age, the earnings limit disappears entirely, allowing you to work as much as you want without penalty.

Prioritizing “Healthspan” in Daily Habits

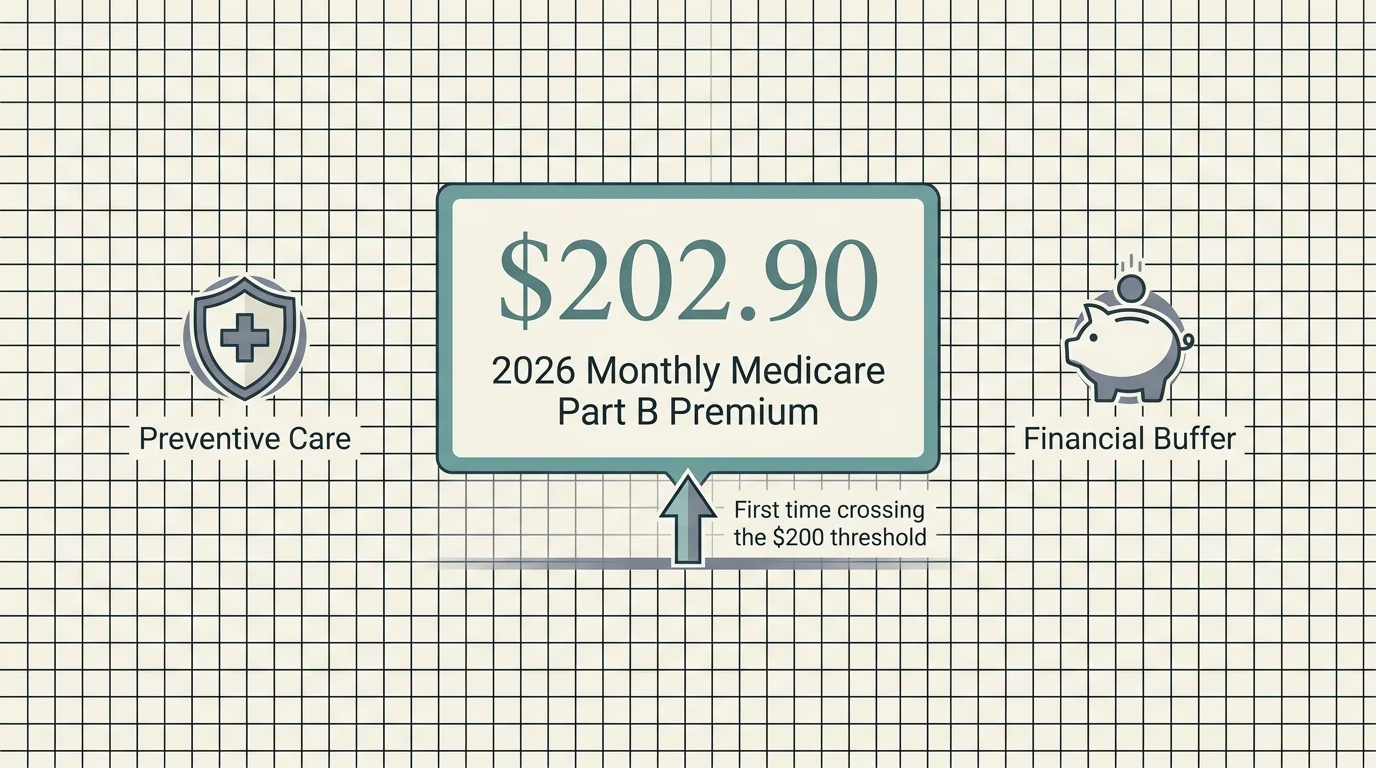

While lifespan measures how long you live, healthspan measures how many of those years are spent in good health, free from chronic disease and disability. Because the base Medicare Part B premium has crossed the $200 threshold for the first time—rising to $202.90 per month in 2026—preventive healthcare is both a medical necessity and a crucial financial strategy. Modern retirees are dedicating specific, non-negotiable blocks of their daily schedule to maintaining their physical independence.

Rather than viewing exercise as a chore, you should treat it as your new part-time job. A balanced routine typically includes cardiovascular work for heart health, resistance training to preserve bone density, and flexibility exercises to prevent falls. Beyond the gym, routine optimization involves meal planning around nutrient-dense whole foods and protecting your sleep schedule. By actively managing your healthspan, you directly reduce your long-term medical costs and preserve your ability to travel, play with grandchildren, and enjoy your accumulated wealth.

Structuring the Unstructured Day

The most successful retirees treat their free time with the same respect and intentionality they once gave their careers—but with vastly different priorities. A common strategy is to divide the day into specific zones to ensure a balanced mix of productivity and relaxation.

Consider dedicating your mornings to high-energy tasks: working out, engaging in deep-focus hobbies like writing or woodworking, or tackling complex financial reviews. Afternoons can be reserved for social connections, volunteering, or part-time work. Evenings naturally transition into restorative downtime. Creating this rhythm prevents the days from blurring together and ensures you are making tangible progress on your personal goals.

| Lifestyle Element | Traditional Retirement Model | The Modern 2026 Routine |

|---|---|---|

| Schedule | Completely unstructured; treating every day like a weekend. | Time-blocked days with dedicated hours for health, learning, and socializing. |

| Income | Relying entirely on a fixed pension, Social Security, and portfolio withdrawals. | A hybrid approach including part-time income, consulting, or gig work. |

| Healthcare | Reactive; visiting the doctor only when an illness or injury occurs. | Proactive; viewing daily exercise and nutrition as primary wealth preservation. |

| Social Life | Passive socializing; hoping friends reach out or relying solely on family. | Active community building; joining clubs, volunteering, and mentoring. |

Navigating 2026 Financial and Tax Realities

Reinventing your routine requires a solid understanding of the financial scaffolding that supports it. The landscape has shifted significantly in 2026, presenting both new challenges and unique opportunities for those who stay informed.

The Social Security Administration announced a 2.8% cost-of-living adjustment (COLA) for 2026, bringing the average monthly retirement benefit to $2,071. While this increase helps, inflation in housing and medical costs means your daily budget must remain flexible. If you are still contributing to retirement accounts through part-time work, 2026 offers expanded catch-up opportunities. The standard workplace plan contribution limit for workers under 50 is $24,500; however, if you are 50 or older, you can add an $8,000 catch-up contribution. Even better, workers ages 60 to 63 can utilize a “super catch-up” limit of $11,250, pushing their total potential contribution to $35,750.

On the healthcare front, prescription drug costs have become more manageable. As part of ongoing changes to Medicare Part D, 2026 introduces a strict $2,100 out-of-pocket cap for covered medications. Once your spending hits this threshold, you enter the catastrophic coverage phase, meaning your plan covers the entire cost of covered drugs for the remainder of the year. Additionally, the maximum Part D deductible is capped at $615.

Tax strategies have also evolved. Beyond the standard deduction and the traditional extra deduction for those 65 and older, a new temporary provision introduced for the 2025-2028 tax years offers eligible seniors an enhanced $6,000 deduction per person ($12,000 for a qualifying married couple filing jointly). This enhanced deduction begins to phase out for single filers with a modified adjusted gross income over $75,000 and joint filers over $150,000, making tax-efficient withdrawal planning more critical than ever.

When DIY Isn’t Enough

While many retirees successfully manage their daily schedules and basic budgets independently, certain complexities demand professional oversight. You should seek out a fiduciary financial planner or tax professional in the following scenarios:

- Optimizing Social Security and Part-Time Income: If you are navigating the earnings limit while claiming early benefits, a professional can help you avoid accidentally forfeiting large portions of your check to taxes and withholding penalties.

- Managing Medicare Surcharges (IRMAA): Because Part B and Part D premiums are tied to your income, a sudden spike in earnings from gig work or a large Roth conversion can trigger the Income-Related Monthly Adjustment Amount. A tax advisor can help you smooth out your income to avoid these hidden cliffs.

- Coordinating Required Minimum Distributions (RMDs): Once you reach RMD age, you must withdraw a specific amount from your tax-deferred accounts annually. If this income pushes you into a higher tax bracket or reduces your eligibility for the new enhanced senior deduction, a professional can introduce strategies like Qualified Charitable Distributions (QCDs) to mitigate the impact.

Avoiding Common Errors

Even with the best intentions, it is easy to stumble during the transition out of the full-time workforce. Recognizing the most common pitfalls allows you to adjust your routine before small missteps become permanent regrets.

The first major error is failing to budget for the reality of “everyday weekends.” When you no longer spend forty hours a week at a desk, you have significantly more time to spend money. Whether it is lingering over an expensive lunch, taking up a costly new hobby, or booking spontaneous travel, discretionary spending can easily outpace your withdrawal strategy if you are not carefully tracking your cash flow.

Another frequent mistake is isolating socially. During your working years, social interaction is practically mandatory. In retirement, it requires proactive effort. You must consciously schedule lunches, join local organizations, or volunteer; otherwise, the convenience of staying home can quickly morph into chronic loneliness.

Finally, many retirees fail to update their estate plans and beneficiaries to reflect their new lifestyle. As you transition into this phase, your legacy goals may shift. Ensuring your designated beneficiaries are current and your healthcare directives are clearly established provides peace of mind that allows you to fully enjoy your daily routine.

“A successful retirement isn’t just about the money. It’s about knowing what you want to do with your time and having the purpose to get out of bed every morning.” — Jean Chatzky, Financial Editor and Author

Designing a fulfilling retirement in 2026 requires you to be an active participant in your own life. By embracing flexible work, prioritizing your physical health, and organizing your days with intention, you transform a period that was once defined by slowing down into a vibrant season of growth. Take the time to evaluate your current habits, make small adjustments to your schedule, and lean into the opportunities that this modern era provides. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Helpful Resources for Your Retirement Planning

- Social Security Administration (SSA) – Verify current COLA adjustments and earnings limits.

- Medicare.gov – Review 2026 Part B premiums and the new Part D out-of-pocket caps.

- Internal Revenue Service (IRS) – Access the latest information on the enhanced senior deduction and standard tax brackets.

- AARP – Explore research on part-time work, unretirement trends, and healthy aging.

- National Council on Aging (NCOA) – Find programs and insights to improve your healthspan and economic security.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.