The traditional hard stop at age 65 is disappearing as more Americans test-drive their post-career years before making a permanent commitment. Stepping directly from full-time work into an unstructured schedule often leads to boredom and financial anxiety. Instead of leaping into the unknown, you can sample different routines, locations, and income strategies through transitions that protect your mental health and savings. Whether you try part-time consulting, relocate to an active adult community, or spend half the year abroad, experiencing these options on a trial basis reveals what truly suits you. This gradual approach allows you to adjust your financial plans, Medicare strategies, and daily habits while maintaining your career safety net.

The Phased Downshifter

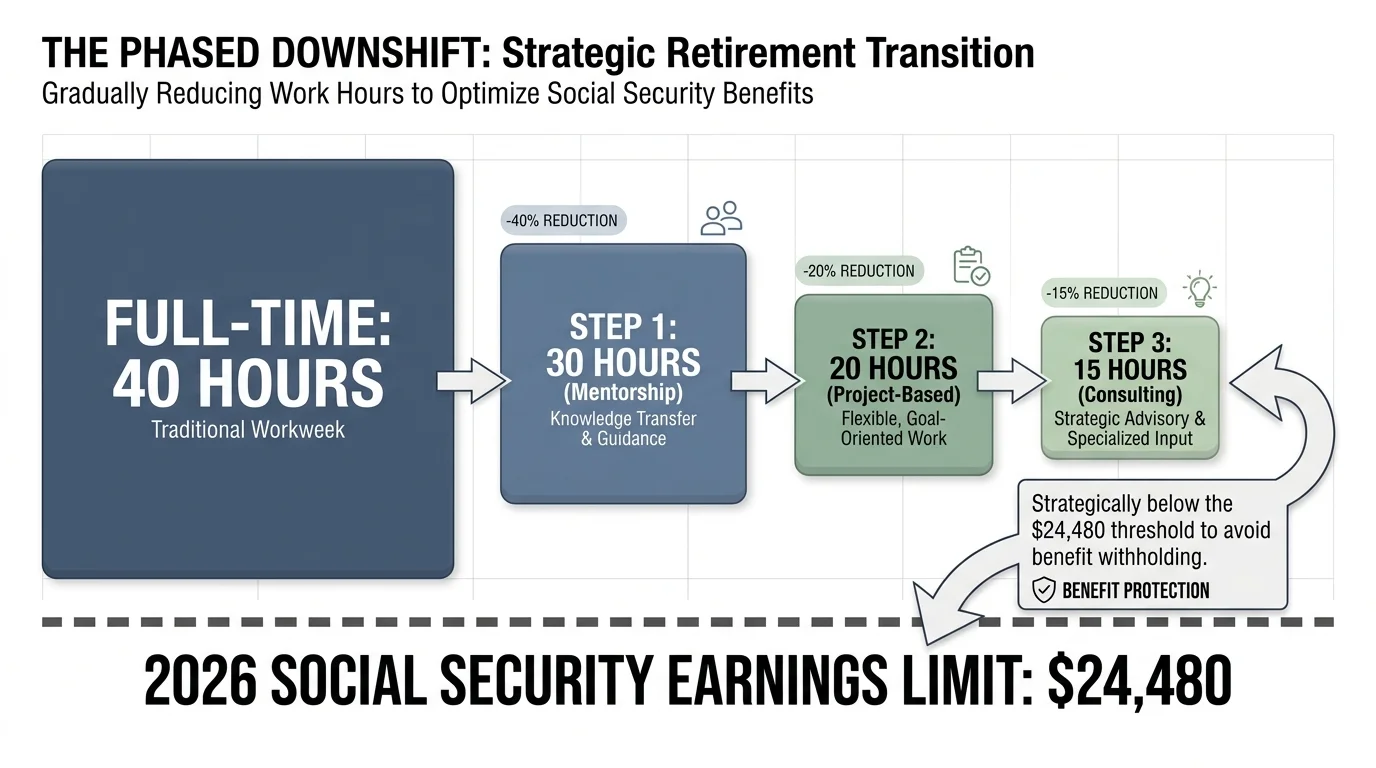

Stepping away from a 40-hour workweek does not require handing in a sudden resignation. A phased downshift involves negotiating a gradual reduction in hours with your current employer over one to three years. You might drop from five days a week to three, shift into a mentorship role, or transition to a project-based contract. Recent employment data suggests that more than 22% of adults aged 65 and older remain in the workforce, many choosing part-time arrangements to ease the psychological transition into retirement.

Testing this lifestyle allows you to maintain social connections at work while exploring how you want to spend your newfound free time. You continue generating income, which preserves your investment portfolio and allows your tax-advantaged accounts to grow.

If you implement a phased approach while claiming early benefits from the Social Security Administration, you must watch your income closely. For 2026, the Social Security earnings limit is $24,480 for individuals who have not yet reached their full retirement age. Earn above that threshold, and the government temporarily withholds $1 in benefits for every $2 in excess earnings. Downshifting allows you to purposefully calibrate your salary to stay below this penalty threshold.

The Encore Consultant

Decades of institutional knowledge possess tremendous value in the open market. The encore consultant tests retirement by launching a freelance or advisory business based on their career expertise. This setup provides ultimate flexibility; you choose your clients, set your own hours, and dictate your vacation schedule.

Consulting also unlocks powerful tax advantages. As an independent contractor, you can deduct legitimate business expenses, home office costs, and technology upgrades. Furthermore, self-employment income allows you to fund a Solo 401(k) or SEP IRA, dramatically accelerating your savings rate in your final working years.

“Whether it’s fly-fishing, taking your camper to the Everglades, or just traveling, everyone has got a little retirement dream.” — Jean Chatzky, Financial Editor and Author

Consulting provides a productive outlet while funding those specific retirement dreams. By taking on just two or three clients a year, you build a bridge between full-time employment and a complete halt in earned income.

The Snowbird Simulator

Escaping harsh winters for warmer climates sounds idyllic, but the reality of owning two properties often entails unexpected stress and double the maintenance. Before you commit to purchasing a second home in Florida, Arizona, or South Carolina, simulate the snowbird lifestyle by renting a furnished property for a single season.

Testing the dual-location lifestyle exposes the logistical hurdles of managing mail, paying out-of-network healthcare costs, and leaving your primary residence empty for months. Renting also grants you the freedom to test different communities each year until you find the perfect fit.

Taxes play a massive role in this decision. Establishing a legal domicile dictates where you pay state income taxes. The Internal Revenue Service (IRS) sets standard federal tax parameters—such as the 2026 standard deduction of $32,200 for married couples filing jointly—but states handle income, property, and estate taxes quite differently. A trial run gives you time to assess whether the tax benefits of a new state outweigh the costs of relocating your official domicile.

The Expat Experimenter

Favorable exchange rates and affordable healthcare draw thousands of American retirees to countries like Portugal, Costa Rica, and Mexico. Uprooting your life to move overseas permanently carries significant risk. The expat experimenter approaches this dream by securing a short-term rental abroad for three to six months to test the local infrastructure, language barriers, and healthcare access.

Living abroad temporarily highlights exactly what you will miss about home. You may discover that spotty internet, unfamiliar banking systems, and distance from grandchildren outweigh the benefits of cheap coastal living.

A crucial factor to test is your healthcare strategy. Medicare generally does not cover medical services received outside the United States. During your trial period, you must secure a robust travel medical policy. You also cannot simply drop your U.S. coverage while testing expat life. You must continue paying your standard Part B premiums—which cost $202.90 per month in 2026 for most beneficiaries—to avoid severe, permanent late-enrollment penalties if you ever return to the U.S.

The Purpose-Driven Volunteer

Many retirees discover that leisure activities fail to provide a lasting sense of fulfillment. The purpose-driven volunteer tests retirement by treating unpaid work with the dedication of a structured career. Before retiring completely, dedicate your weekends and evenings to a nonprofit organization, animal shelter, or community board.

A trial phase reveals whether a specific organization aligns with your values and energy levels. Volunteering builds a fresh social network outside of your corporate life. Organizations like AARP and various local senior centers depend heavily on the specialized skills that experienced professionals bring to the table. By testing this routine early, you ensure you have a meaningful place to channel your energy on day one of retirement.

The RV Nomad

The freedom of the open road calls to many soon-to-be retirees. The vision involves selling the family home, buying a luxury motorhome, and visiting national parks year-round. This lifestyle shift represents an enormous financial commitment, as high-end recreational vehicles depreciate rapidly and require constant maintenance.

Test the nomadic lifestyle by renting an RV for a four-week cross-country trip. A trial run exposes the unglamorous realities of the road: emptying black water tanks, navigating narrow campground spaces, managing fuel costs, and living in exceptionally close quarters with your spouse.

If you thrive during the trial, you can proceed with confidence. If you discover that three weeks in a rolling house is your absolute limit, you just saved yourself a six-figure mistake.

The Active Adult Communitarian

Age-restricted 55+ communities offer golf courses, pickleball tournaments, fitness centers, and instant social circles. However, living under the strict guidelines of a Homeowners Association (HOA) requires a significant adjustment. Before selling your current home and buying into an active adult community, secure a short-term lease within the neighborhood.

Renting allows you to experience the actual community culture. You can test the noise levels, evaluate the quality of the amenities, and determine if the social scene feels welcoming or cliquish. This trial period also allows you to review the HOA’s financial health and restriction documents without the pressure of a looming real estate closing.

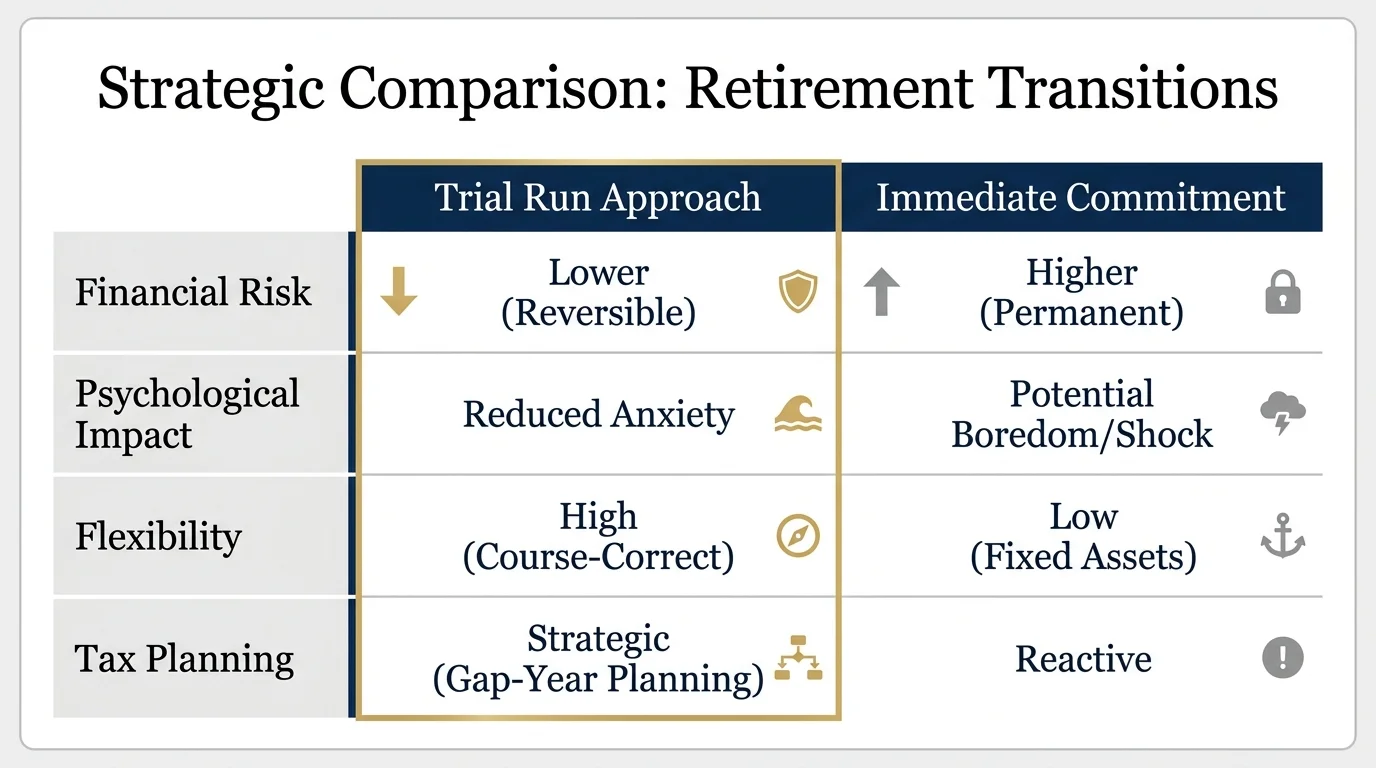

Comparing Your Options: Trial Run vs. Immediate Commitment

Understanding the difference between a calculated test and a permanent leap helps you manage expectations and protect your assets. Here is how a trial approach stacks up against immediate commitment across various factors:

| Lifestyle Factor | Trial Run Approach | Immediate Commitment Risk |

|---|---|---|

| Housing & Relocation | Renting a home or RV for 1-3 months to test the environment. | Paying high real estate transaction costs; potential buyer’s remorse. |

| Income Replacement | Scaling back hours or taking 1-2 consulting clients. | Full reliance on portfolio withdrawals; sequence of returns risk. |

| Healthcare Coverage | Testing private travel policies while maintaining domestic Medicare. | Dropping U.S. coverage entirely, leading to lifetime Medicare penalties. |

| Social Connections | Building new networks while retaining workplace friendships. | Sudden isolation and loss of professional identity. |

What Can Go Wrong When Testing Lifestyles

While testing retirement routines protects you from massive errors, trial periods carry their own distinct risks if managed poorly.

- Underestimating Healthcare Gaps: If you transition to part-time work and lose employer-sponsored health insurance before age 65, navigating the Affordable Care Act marketplace can result in premium shock.

- Tax Complications: Working remotely from a “test” location in another state can trigger unexpected tax liabilities. Earning income across multiple state lines complicates your tax filings and may require you to pay partial income taxes in your destination state.

- Trial Burnout: Trying to juggle a phased retirement plan while simultaneously traveling or starting a consulting business can lead to exhaustion. Testing too many variables at once defeats the purpose of finding a peaceful transition.

When to Consult a Professional

Navigating the transition away from full-time work involves complex financial maneuvers. Consider engaging a professional under the following circumstances:

- Modeling Roth Conversions: If you step down to part-time work, your income drops, creating a window for low-tax Roth conversions before your Required Minimum Distributions (RMDs) begin. A tax professional can calculate exactly how much to convert without bumping you into a higher bracket.

- Evaluating Social Security Timing: Balancing part-time consulting income against the Social Security earnings limit requires precise planning to avoid benefit withholding.

- Establishing Domicile: If your snowbird trial goes perfectly and you want to make the move permanent, a certified financial planner and an estate attorney must help you sever ties with your high-tax state legally.

“Your IRA is an IOU to the IRS.” — Ed Slott, CPA and IRA Expert

Slott’s warning rings especially true during your transition years. Engaging an advisor helps you pay that tax debt efficiently while your income is temporarily lower during a phased retirement.

Frequently Asked Questions

Does working part-time mean I lose my Social Security benefits?

If you claim Social Security before your full retirement age and continue working, your benefits are subject to an earnings limit. For 2026, you can earn up to $24,480. If you earn more, the SSA withholds $1 for every $2 over the limit. However, these withheld benefits are not permanently lost; your monthly payout is recalculated and increased once you reach full retirement age.

Do I still need to pay Medicare premiums if I live abroad half the year?

Yes. If you drop Medicare Part B while living abroad and later decide to return to the United States, you will face a 10% premium penalty for every full 12-month period you were eligible but not enrolled. Maintaining your Part B coverage, which is $202.90 per month in 2026, acts as an insurance policy for your future return.

How long should I test a retirement lifestyle?

A true trial requires at least three to six months. A two-week trip feels like a vacation, but staying in one place for three months exposes the reality of routine tasks like grocery shopping, navigating local healthcare, and experiencing changing weather patterns.

Testing these routines puts you in the driver’s seat. You gain the freedom to change your mind without suffering massive financial penalties or lifestyle regrets. Try the routine, run the numbers, and adjust your course until you find a daily rhythm that genuinely excites you.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.