Relocating for retirement often sounds like a dream, but choosing the wrong destination can devastate a fixed income. Many popular spots disguise hidden costs like surging property taxes, skyrocketing home insurance premiums, and aggressive state taxes on your benefits. If you rely on fixed income sources like Social Security, these financial surprises can force you out of your new home before you even settle in. By analyzing 2026 economic data, you can uncover exactly which scenic retreats mask a steep cost of living. Knowing these financial landmines ahead of time protects your nest egg and ensures your retirement years remain secure, comfortable, and genuinely stress-free without ever forcing you to return to work.

1. Honolulu, Hawaii: The Ultimate Price for Paradise

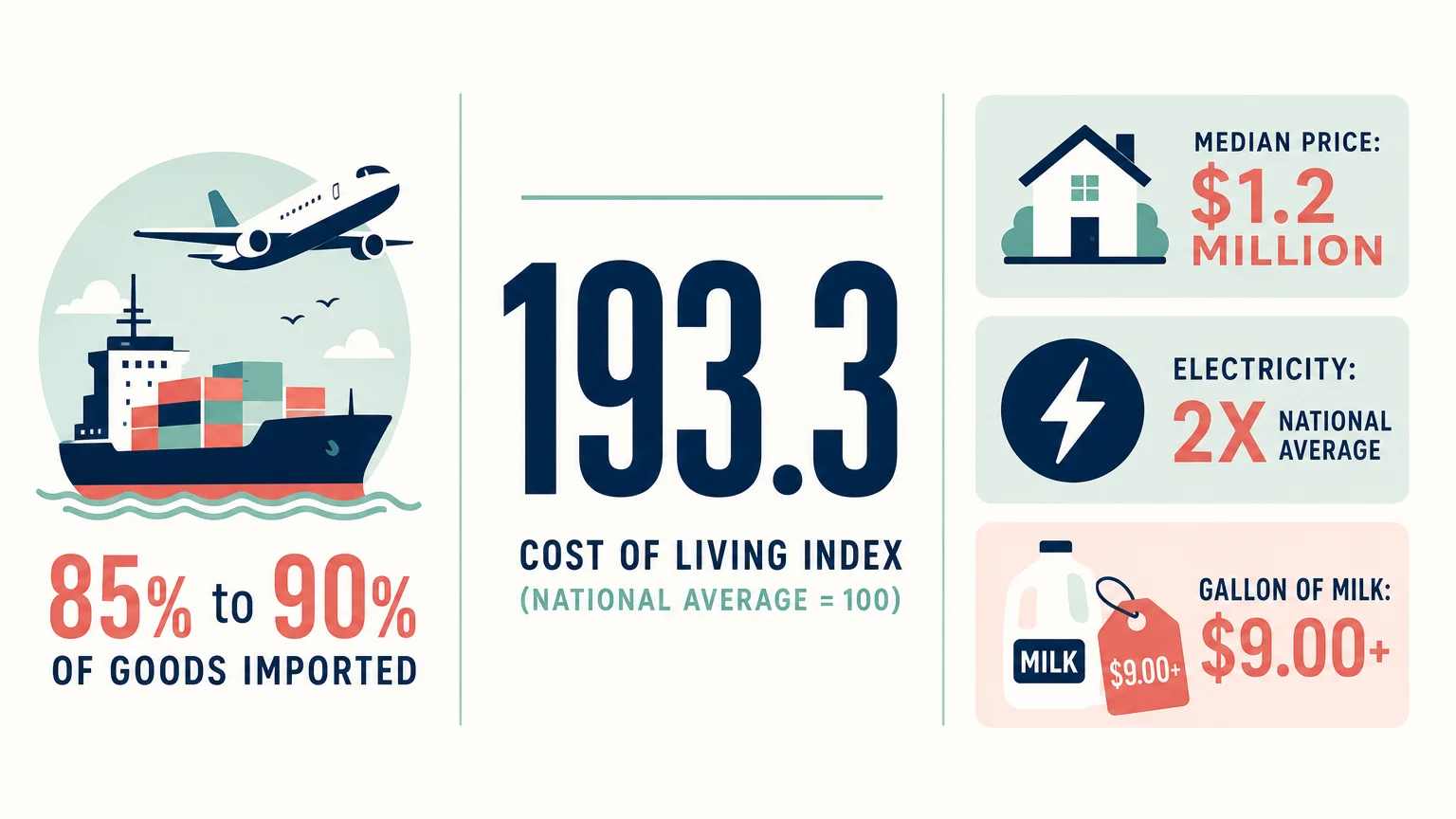

Retiring in Hawaii is the ultimate American dream for many, but the financial reality of Honolulu is staggering. Because Hawaii is an isolated volcanic archipelago, roughly 85% to 90% of all consumer goods must be shipped or flown in from the mainland. This logistical hurdle means that freight costs are baked into every single purchase you make—from a gallon of milk to replacement car parts.

Recent economic data reveals that Hawaii’s cost of living index sits at a staggering 193.3, which is nearly double the national average. The median price for a single-family home on Oahu exceeds $1.2 million, and electricity rates are more than double the national average. If you are surviving on a fixed income, living in Honolulu demands a radical downsizing of your lifestyle. You will likely trade a spacious mainland home for a small condo, limit dining out, and constantly monitor your utility usage just to keep your budget intact.

2. Naples, Florida: The Rising Cost of Sunshine

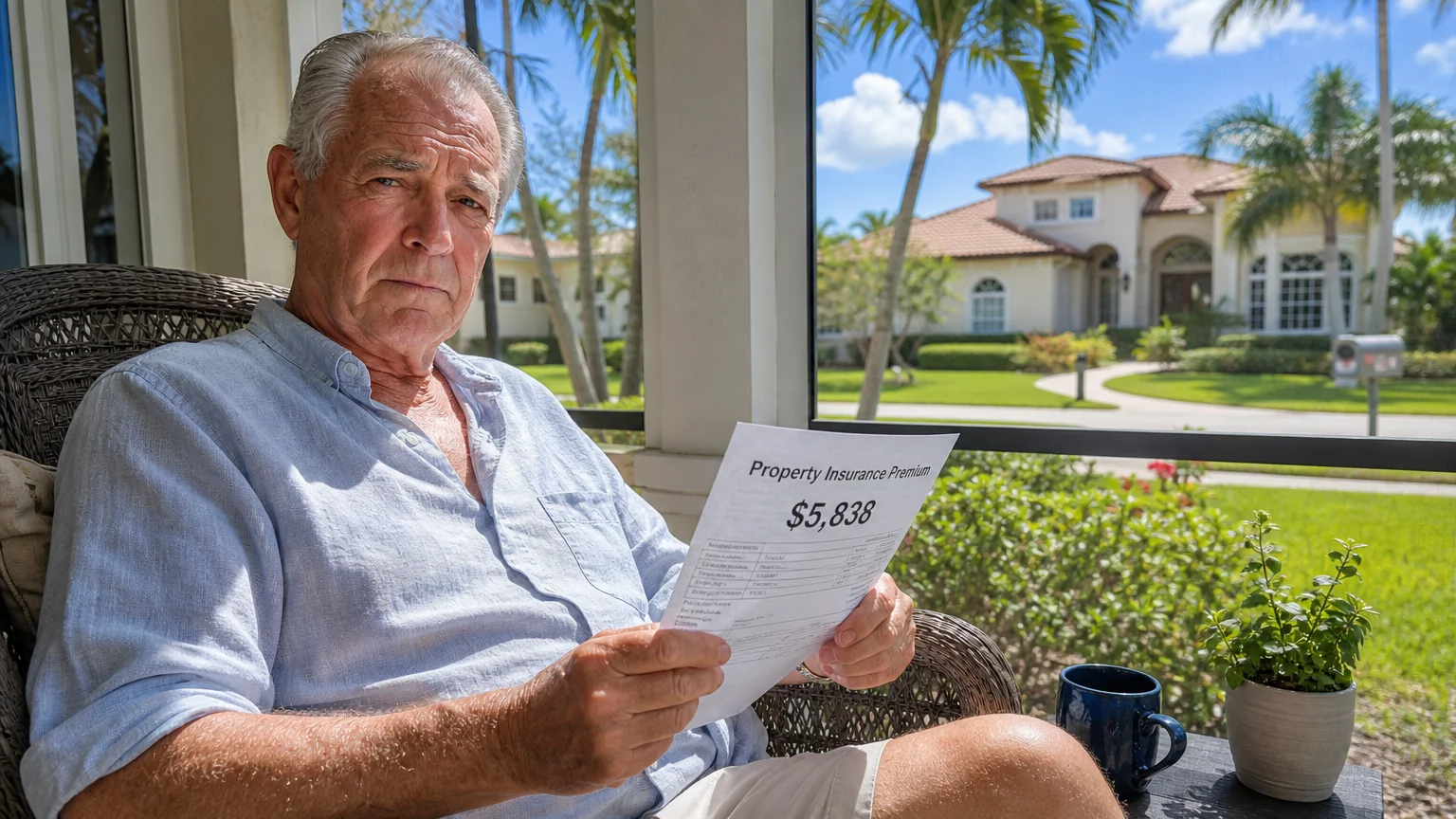

Florida has long been the traditional gold standard for American retirement due to its warm winters and lack of state income tax. Naples, situated on the pristine Gulf Coast, attracts retirees with its luxury shopping and pristine golf courses. However, the cost of residing in this sunshine state has reached a critical breaking point regarding property insurance.

Florida’s property insurance market remains highly volatile. The statewide average home insurance premium has surged to roughly $5,838, which is drastically higher than the national average. Because Naples is located in a prime hurricane zone with highly valued real estate, your individual premium could easily exceed that state average. For a retiree relying strictly on fixed monthly payouts, an annual insurance spike of several thousand dollars can drain emergency cash reserves entirely. Furthermore, high demand has driven up local service costs, meaning everything from landscaping to basic home maintenance comes with an inflated price tag.

3. Scottsdale, Arizona: A Snowbird Haven Turned Millionaire’s Market

Scottsdale lures retirees with world-class resorts, beautiful desert landscapes, and warm, dry winters that are gentle on aching joints. But over the last decade, this Phoenix suburb has transformed aggressively into a millionaire’s market. A recent analysis by GoBankingRates ranks Scottsdale as one of the top most expensive retirement cities in the country.

The city’s ballooning wealthy population, combined with strict zoning laws that heavily restrict affordable housing and apartments, keeps real estate prices exceptionally high. If you plan to rely solely on your Social Security check and a modest IRA distribution, the sheer cost of property taxes, homeowners association (HOA) fees, and premium healthcare services in Scottsdale will rapidly erode your purchasing power. Retirees looking for the Arizona climate are often better served exploring neighboring, less restrictive communities.

4. San Diego, California: Unforgiving Taxes and Utility Bills

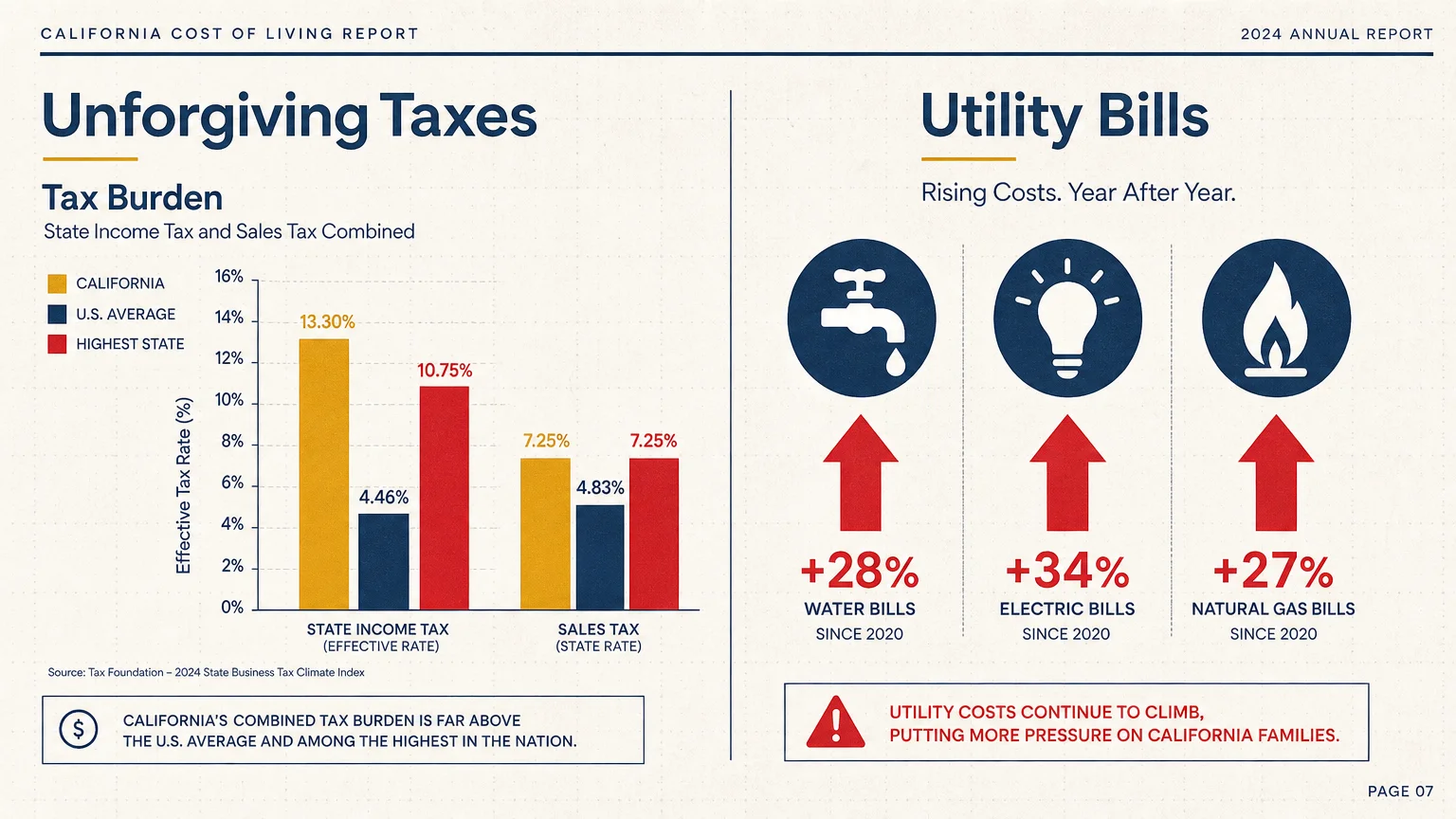

San Diego boasts arguably the most perfect year-round weather on the planet. Unfortunately, that perfect weather comes heavily taxed. California famously levies the highest state income taxes in the nation, with a top marginal rate that can reach 13.3%, plus an additional payroll tax pushing the absolute maximum to 14.4%. While a fixed-income retiree likely won’t hit the top bracket, the baseline cost of existing in California is still steep.

Beyond state taxes, San Diego residents face astronomical utility costs and gasoline prices. Running your air conditioning during seasonal heatwaves, or merely paying for water in a drought-prone region, consumes a massive portion of a fixed monthly income. Unless you have a remarkably large pension or heavily funded trust, the day-to-day carrying costs of living in San Diego will put immense strain on your finances.

5. Santa Fe, New Mexico: Double Taxation on Social Security

Santa Fe is a cultural gem. It offers a vibrant arts scene, distinct historic architecture, and gorgeous mountain vistas that appeal to creatively minded retirees. Yet, many retirees move to the Southwest only to be blindsided by New Mexico’s tax policies.

As of 2026, New Mexico remains one of only eight states that still taxes Social Security benefits. When you combine the state taxation of your primary retirement income with Santa Fe’s notoriously high housing costs—driven by strict historic building codes and heavy tourism—the financial math becomes difficult. If you fall in love with the high desert, you must carefully calculate whether your fixed budget can actually withstand this double taxation on your benefits.

6. Charleston, South Carolina: Hidden Risks and Surging Premiums

Charleston offers quintessential Southern charm, incredible culinary experiences, and deep historical roots. It is visually stunning, but living near the Atlantic Ocean introduces massive hidden risks that can easily upend a fixed income.

The most immediate financial threat to a retiree in Charleston is water. Flood insurance is essentially mandatory for most desirable neighborhoods, and hurricane deductibles can require you to cover tens of thousands of dollars out-of-pocket before insurance kicks in. Furthermore, as Charleston’s popularity skyrockets, local property assessments rise with it. A home you purchase today might be reassessed at a significantly higher value next year, leading to a property tax bill that massively outpaces your annual Social Security cost-of-living adjustment.

7. Bozeman, Montana: Harsh Winters and Housing Shortages

Active retirees who love hiking, skiing, and wide-open spaces frequently target Bozeman for their golden years. However, a massive influx of out-of-state wealth has created a severe housing shortage, driving rents and home prices into the stratosphere over the past five years.

Beyond the cost of acquiring a home, Bozeman’s bitter winters require substantial heating budgets and specialized seasonal home maintenance (like professional snow removal and roof ice dam prevention). To make matters worse for fixed-income planners, Montana is another one of the eight states that continue to tax Social Security benefits in 2026. Paying state income taxes on your benefits while simultaneously battling sky-high winter utility bills is a guaranteed way to deplete your savings.

8. Asheville, North Carolina: High Healthcare and Housing Strain

Nestled in the Blue Ridge Mountains, Asheville has long been celebrated as a progressive, artsy, and scenic retirement haven. However, its immense popularity has severely strained local infrastructure. The housing inventory remains incredibly tight, pushing median home prices far beyond what a typical fixed-income budget can safely support.

Additionally, retirees often find that healthcare logistics are complicated in this mountain region. While there are quality medical facilities, finding specialists taking new Medicare patients can require long wait times or travel to larger metro areas. When your budget is tightly fixed, the combination of rising local property values and the potential need to travel for specialized medical care creates a storm of ongoing financial stress.

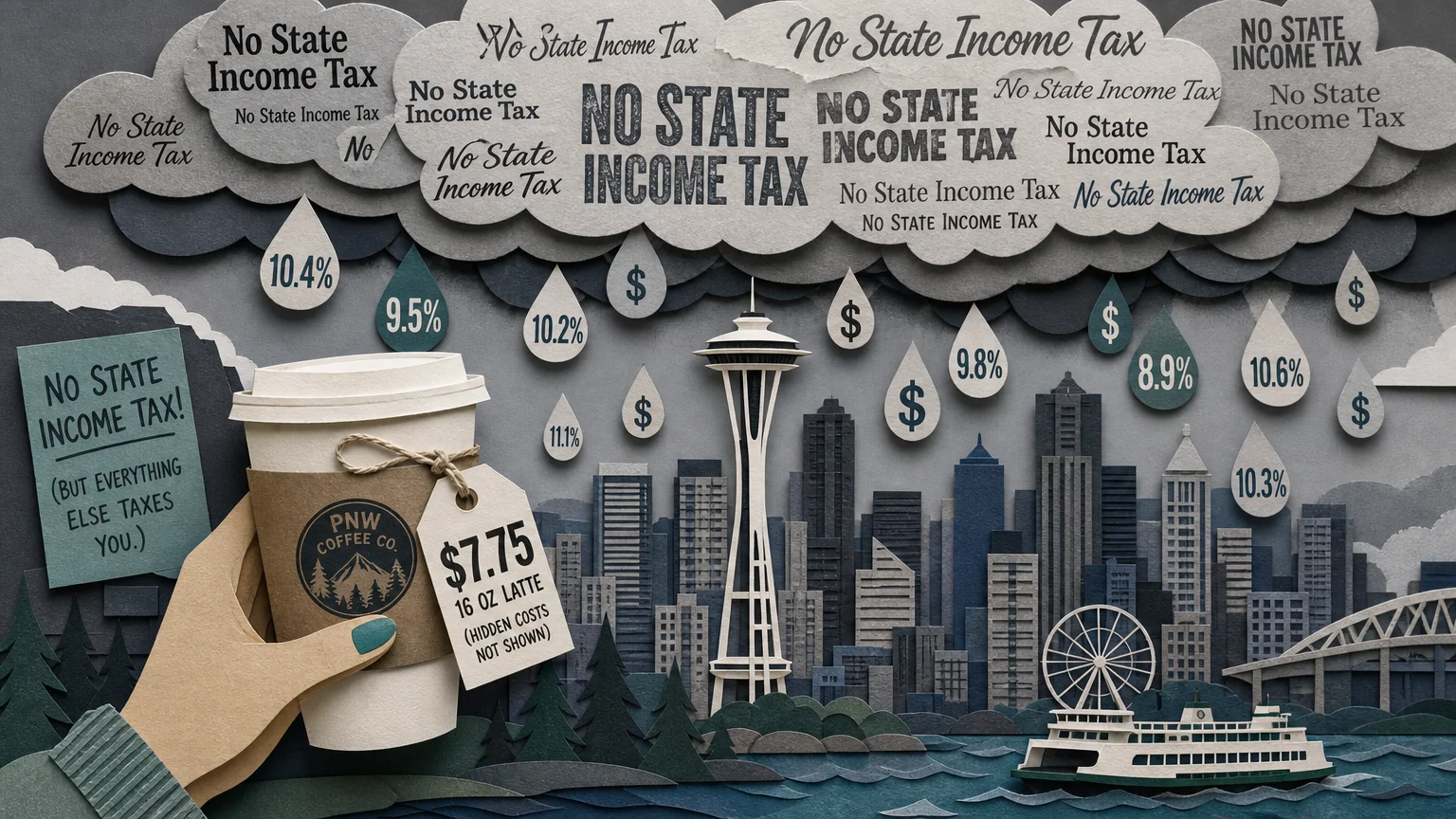

9. Seattle, Washington: No Income Tax Doesn’t Mean Cheap

Washington State appeals to many retirees because it does not levy a traditional state income tax on wages (though it does aggressively tax high-end capital gains). But do not let the lack of income tax fool you; Seattle’s overall cost of living is punishing.

While basic goods might be slightly cheaper than in Honolulu, day-to-day expenses for groceries, transportation, and professional services in Seattle are astronomical. Moreover, the famous gloomy, wet winters often drive retirees to seek sunny winter escapes (snowbirding). Funding travel and a temporary rental in a second location for three months out of the year is an incredibly difficult feat when you are strictly managing a fixed income.

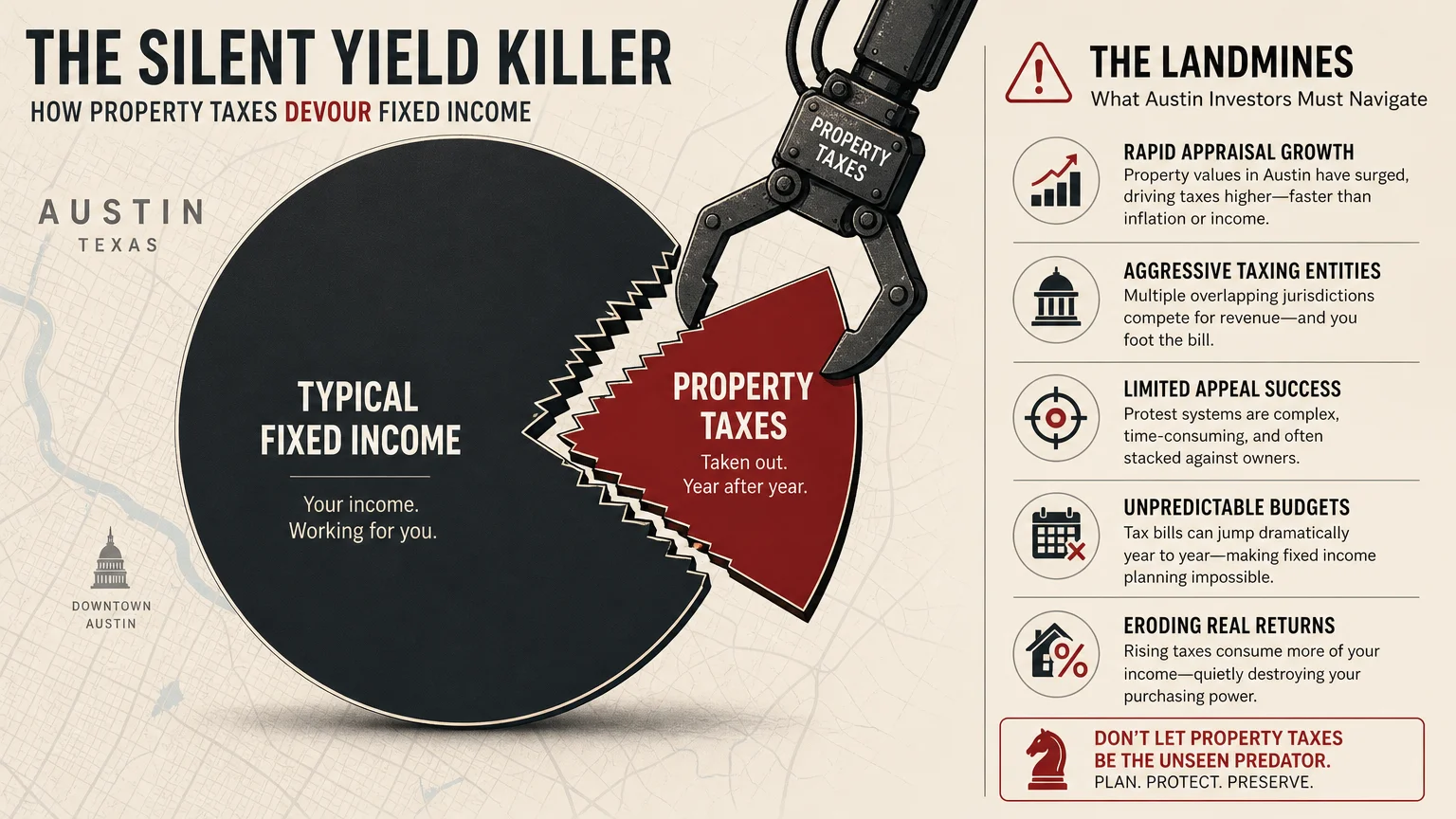

10. Austin, Texas: Property Taxes That Devour Fixed Incomes

Texas is famous for having no state income tax, and Austin’s vibrant music scene, robust economy, and excellent dining make it an exciting destination. But the absence of a state income tax means local governments must generate revenue elsewhere—and they do so through aggressive property taxes.

Austin’s real estate values have exploded over the past decade. Even if your mortgage is completely paid off, the annual property tax bill can feel like you are paying rent directly to the city. As home values continue to climb, property taxes are reassessed upward. Fixed-income retirees in Austin frequently find themselves “house rich but cash poor,” ultimately forced to sell and relocate simply to escape the crushing weight of their rising tax burden.

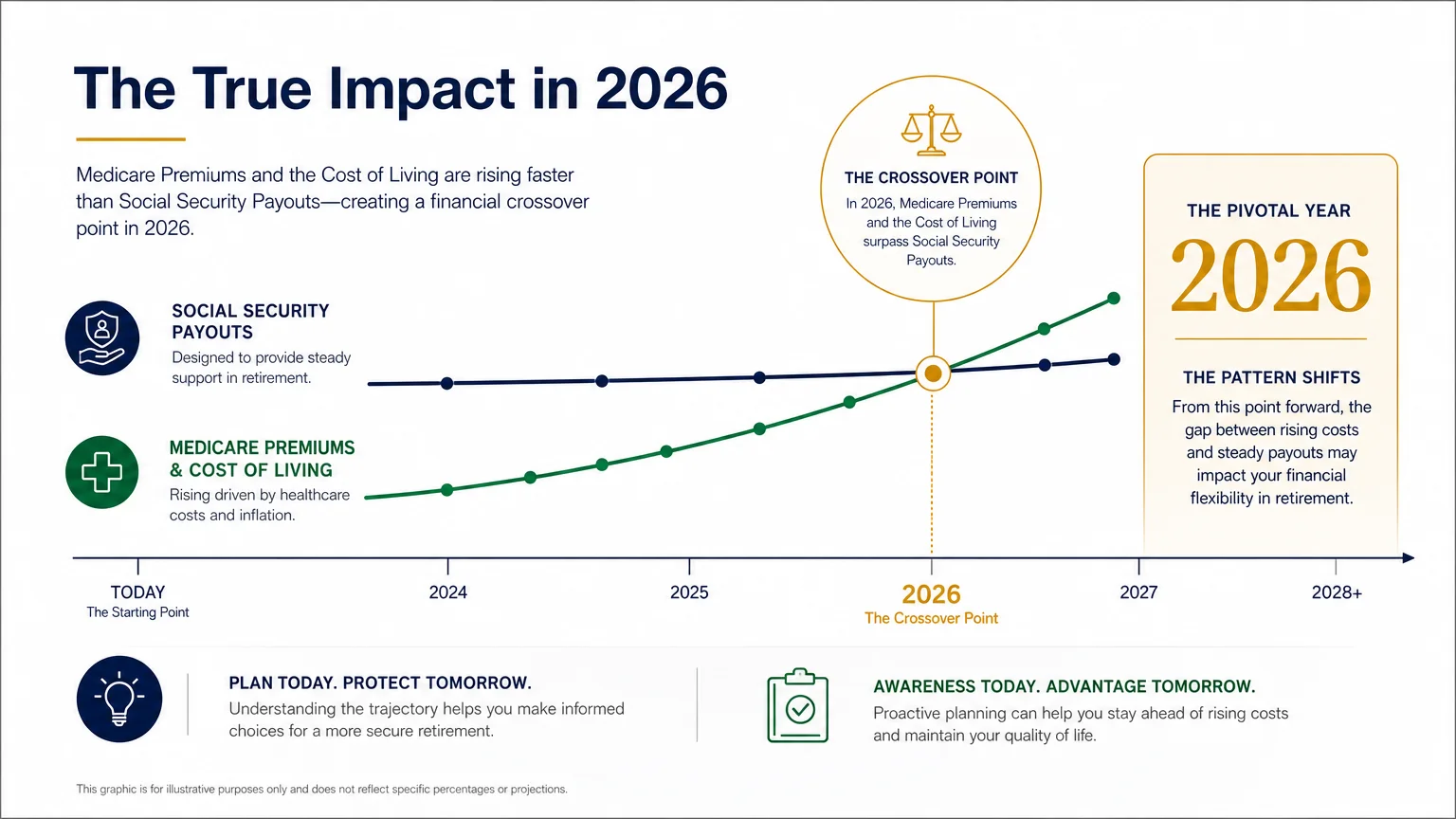

The True Impact of Medicare and Social Security in 2026

When planning a relocation, you must measure your destination’s cost of living against the actual baseline of federal retirement benefits. In 2026, the Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA). While any benefit increase is welcome, a 2.8% bump rarely covers the aggressive, localized inflation found in high-demand retirement hot spots.

Simultaneously, federal healthcare costs continue to climb. The standard Medicare Part B premium for 2026 rose to $202.90 per month, and the annual Part B deductible increased to $283. If your Social Security COLA adds $50 to your monthly check, but your Medicare premiums and local utility bills rise concurrently, your net gain is entirely wiped out.

Your actual take-home income is also dictated by tax brackets. For 2026, the federal standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. If you move from a tax-friendly state to one that aggressively taxes your property and benefits, the federal standard deduction will not be enough to shield your fixed income from local financial strain.

| Category | 2026 Baseline Amount | Why It Matters for Relocation |

|---|---|---|

| Medicare Part B Premium | $202.90 / month | If your destination has high living costs, paying this premium (plus potential IRMAA surcharges) will heavily squeeze your fixed budget. |

| Social Security COLA | 2.8% increase | A minor federal bump will not cover the hyper-inflation of property taxes and insurance found in popular coastal destinations. |

| Standard Deduction (Single) | $16,100 | Moving to a state with heavy local income taxes offsets the value of this federal tax protection. |

| Standard Deduction (Joint) | $32,200 | While a larger deduction helps federally, high local property taxes in cities like Austin can wipe out your tax savings entirely. |

Avoiding Common Relocation Errors

Retirees frequently make emotional decisions when choosing a relocation destination. Falling in love with a vacation spot is easy; affording it 365 days a year is much harder. To protect your fixed income, keep these vital strategies in mind:

- Never Buy Before You Rent: Always rent in your target destination for at least six months—preferably during the worst weather season. This exposes you to the true cost of utilities, the reality of the local climate, and the actual price of day-to-day groceries before you lock up your liquidity in real estate.

- Investigate Shadow Costs: Look beyond the listing price of a home. Investigate historical property tax increases, mandatory flood insurance premiums, and the financial health of the local Homeowners Association (HOA). An HOA with poorly funded reserves will inevitably pass massive special assessments down to you.

- Verify Healthcare Networks: A low cost of living often correlates with rural isolation. Ensure that your specific Medicare Advantage or Medigap plan is accepted by top-tier specialists in your new zip code.

“Taxes will be the single biggest expense in retirement. It’s not about what you make; it’s about what you keep.” — Ed Slott, CPA and Retirement Tax Expert

When DIY Isn’t Enough: Hiring a Relocation Team

Moving across state lines permanently changes your legal and financial landscape. If you are relocating to a state with complex tax laws or high living costs, trying to manage the transition entirely by yourself is incredibly risky. Consider hiring professionals in these specific scenarios:

- Establishing Tax Domicile: If you are moving to a state with zero income tax (like Florida or Texas) but plan to keep a property in your former state, hire a CPA. High-tax states will aggressively audit your move to prove you still owe them taxes. A CPA ensures your transition of domicile is legally ironclad.

- Navigating Medicare Networks: Health insurance is deeply localized. Work with an independent, licensed Medicare broker in your new state to confirm your current coverage transfers smoothly, or to find a new plan that includes your required local specialists.

- Stress-Testing Your Portfolio: Before signing a mortgage in a high-cost area, ask a Certified Financial Planner (CFP) to run a Monte Carlo simulation. This mathematical stress test will prove whether your fixed income can actually survive a 20-year retirement in an expensive destination.

Frequently Asked Questions

Which states do not tax Social Security benefits in 2026?

As of 2026, 42 states (plus the District of Columbia) do not tax your Social Security benefits. Only eight states still impose taxes on these benefits: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont. West Virginia completely eliminated its tax on benefits in 2026.

What is the standard Medicare Part B premium for 2026?

The standard monthly premium for Medicare Part B is $202.90 in 2026. Keep in mind that if you have a high income, you may be subject to an Income-Related Monthly Adjustment Amount (IRMAA), which will increase your premium.

Does a lower cost of living mean worse healthcare?

Not necessarily, but it is a major factor to investigate. Highly rural areas often boast cheap real estate and low taxes, but they may lack major hospital systems or specialized care facilities. Always verify the distance to a Level 1 trauma center and check specialist availability before finalizing a move.

Before packing your bags and heading for a tropical beach or a mountain retreat, take the time to run the hard numbers. Your retirement destination should provide peace of mind, not financial anxiety. Consult Social Security Administration (SSA) guidelines, review your coverage options at Medicare.gov, and build a localized budget based on current data.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.