Choosing where to spend your retirement is an exciting decision, but focusing only on sunny highlights can lead to expensive regrets. Before packing up for a renowned retiree haven, you must look past the marketing brochures to uncover the hidden costs, environmental risks, and lifestyle challenges locals rarely mention. From crushing property tax burdens in Texas to soaring homeowner’s insurance premiums in Florida, every popular destination comes with significant compromises. Exploring the specific downsides of the ten most sought-after retirement locations helps you weigh your options realistically. Armed with current financial data and practical insights, you can protect your nest egg and confidently find the community that truly fits your long-term needs.

1. Florida: The Home Insurance Squeeze

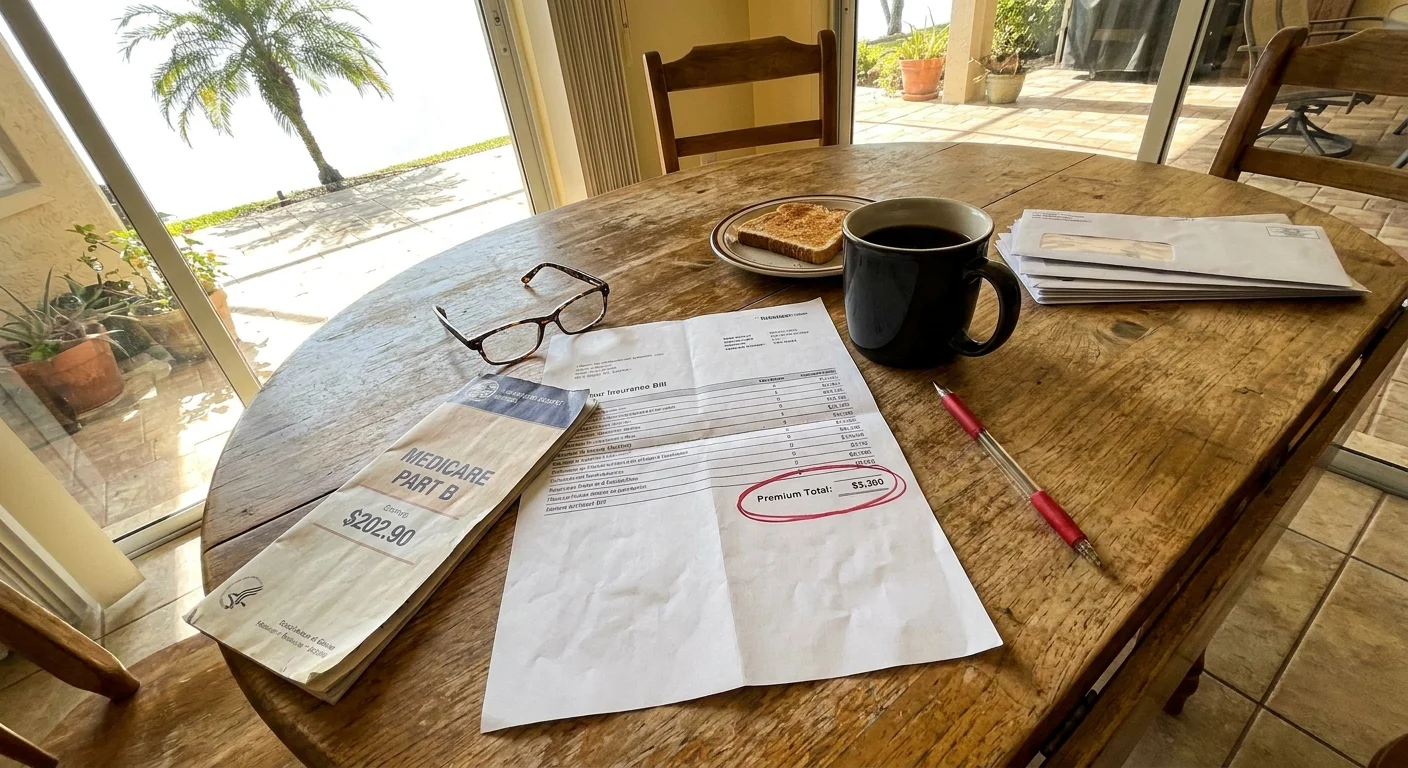

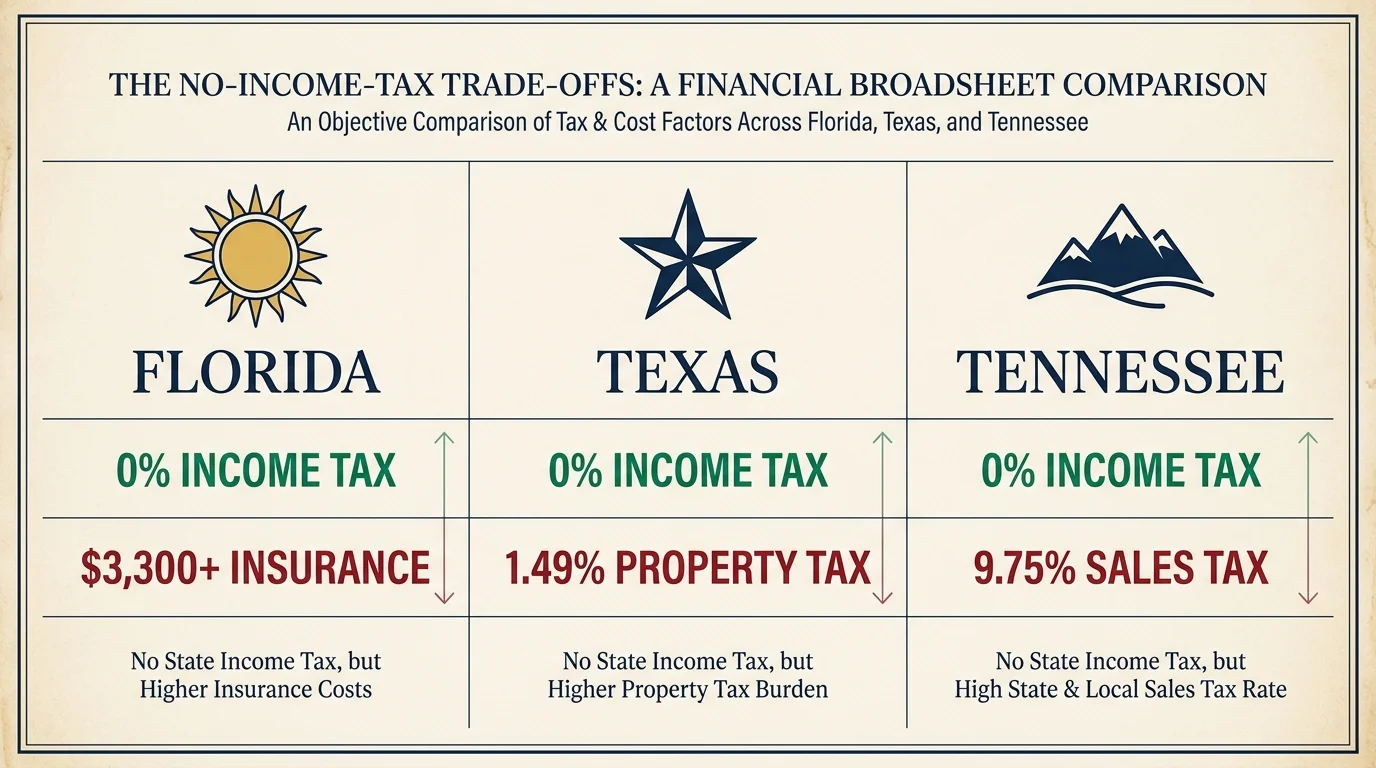

Florida remains a top destination for its zero percent state income tax and endless sunshine, but moving to coastal cities exposes your retirement budget to a volatile and rapidly deteriorating property insurance market. Recent market data indicates the average home insurance cost for Florida homeowners in 2026 routinely exceeds $3,300 statewide, but that figure hides the true danger. If you purchase a home near the coast, in a flood zone, or on a barrier island, your premiums can easily spike between $10,000 and $15,000 annually.

Living on a fixed income requires predictable expenses. With the standard Medicare Part B premium rising to $202.90 per month in 2026, piling a massive, unpredictable insurance bill on top of your healthcare costs can quickly destabilize your financial plan. If a major hurricane hits, insurers often pull out of the state entirely or drastically raise premiums the following year, leaving you stranded with fewer coverage options.

Beyond the financial strain, the physical reality of the “Sunshine State” can become stressful. The sweltering summer heat forces many seniors indoors for months at a time, and the intense crowding during the winter peak season makes navigating local roads, grocery stores, and medical clinics a frustrating daily chore.

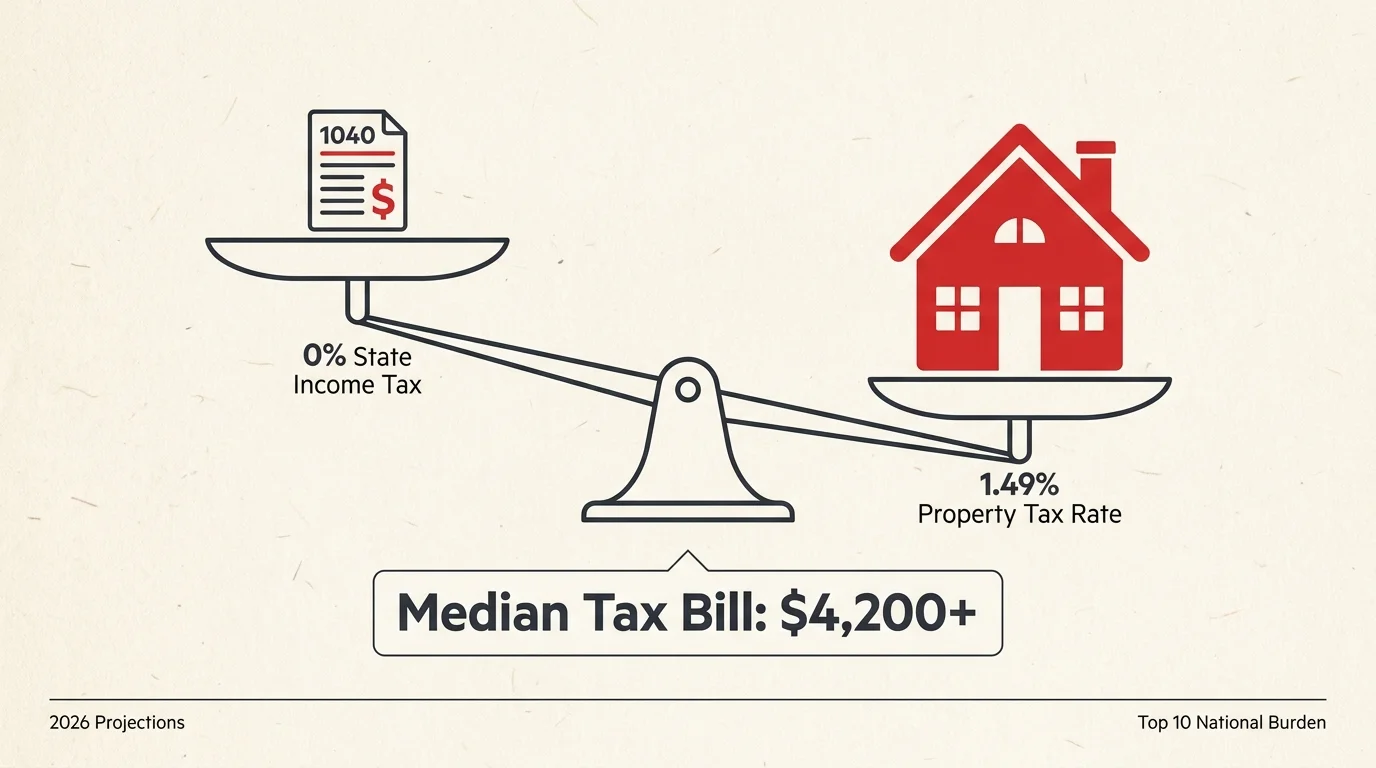

2. Texas: Crushing Property Taxes

The Texas Hill Country and Austin suburbs boast a comparatively low cost of living on paper. Like Florida, Texas attracts retirees by proudly advertising no state income tax. But what the state government gives with one hand, local municipalities take with the other through aggressive property tax assessments.

In 2026, the effective property tax rate in Texas remains one of the highest in the nation at roughly 1.49%, firmly planting the state in the top ten highest property tax burdens nationwide. Depending on your home’s assessed value, a median tax bill regularly exceeds $4,200 annually, and in high-demand metro areas, it climbs much higher. Because property taxes are based on housing values rather than your income, a sudden boom in the local real estate market can skyrocket your tax bill, even if your pension or Social Security check remains exactly the same.

Additionally, retirees in Texas must navigate extreme summer heat and lingering concerns regarding the reliability of the state’s power grid during severe weather events. For older adults who rely on uninterrupted air conditioning or electrically powered medical equipment, grid vulnerability is a serious safety consideration.

3. Tennessee: The Silent Sales Tax Drain

Many retirees flock to Nashville, Chattanooga, and the Smoky Mountains to avoid state income tax while enjoying four mild seasons and beautiful scenery. While you will save money on your traditional income tax return, you will pay a steep premium at the cash register. Tennessee relies heavily on consumption taxes to fund state operations.

Tennessee enforces a base sales tax rate of 7.00%, but when combined with county and city taxes, the total rate reaches up to 9.75% in 2026. This high sales tax takes a heavy toll on everyday purchases—from home maintenance supplies and electronics to dining out and vehicle purchases. For retirees attempting to stretch a modest 2.8% Social Security Administration (SSA) cost-of-living adjustment (COLA) in 2026, a nearly 10% tax on everyday consumption steadily and silently erodes purchasing power.

4. Arizona: Searing Heat and Water Scarcity

Cities like Scottsdale, Mesa, and Phoenix draw active adults with top-tier golf courses, low humidity, and a vibrant retiree culture. However, the desert environment brings extreme environmental and utility challenges that are worsening over time.

Arizona’s summer heat is relentless. Temperatures frequently top 110 degrees for weeks at a time, confining many older adults indoors from June through September. This seasonal reality severely limits outdoor social activities and drives air conditioning bills through the roof. Furthermore, long-term water scarcity continues to threaten the region’s rapid development. Water conservation restrictions are becoming a permanent reality for residents. As water access becomes more expensive for municipalities to secure, utility rates and overall housing costs are expected to climb, adding unpredictable inflation to your housing budget.

5. North Carolina: Overwhelmed Infrastructure

Mountain towns like Asheville and Hendersonville have surged in popularity due to their moderate climate, artsy culture, and access to the Blue Ridge Parkway. Unfortunately, the rapid influx of new residents has far outpaced local infrastructure.

Retirees frequently encounter heavy traffic on narrow mountain roads, limited public transportation, and long wait times for specialized medical appointments. More alarmingly, the vulnerability of this region was exposed by recent extreme weather events. The catastrophic damage from Hurricane Helene demonstrated that even inland, higher-elevation areas are not immune to historic flooding, mudslides, and prolonged power outages. The massive demand for housing has also driven mountain home prices far above the national average, pricing out middle-class retirees who thought they were moving to an affordable haven.

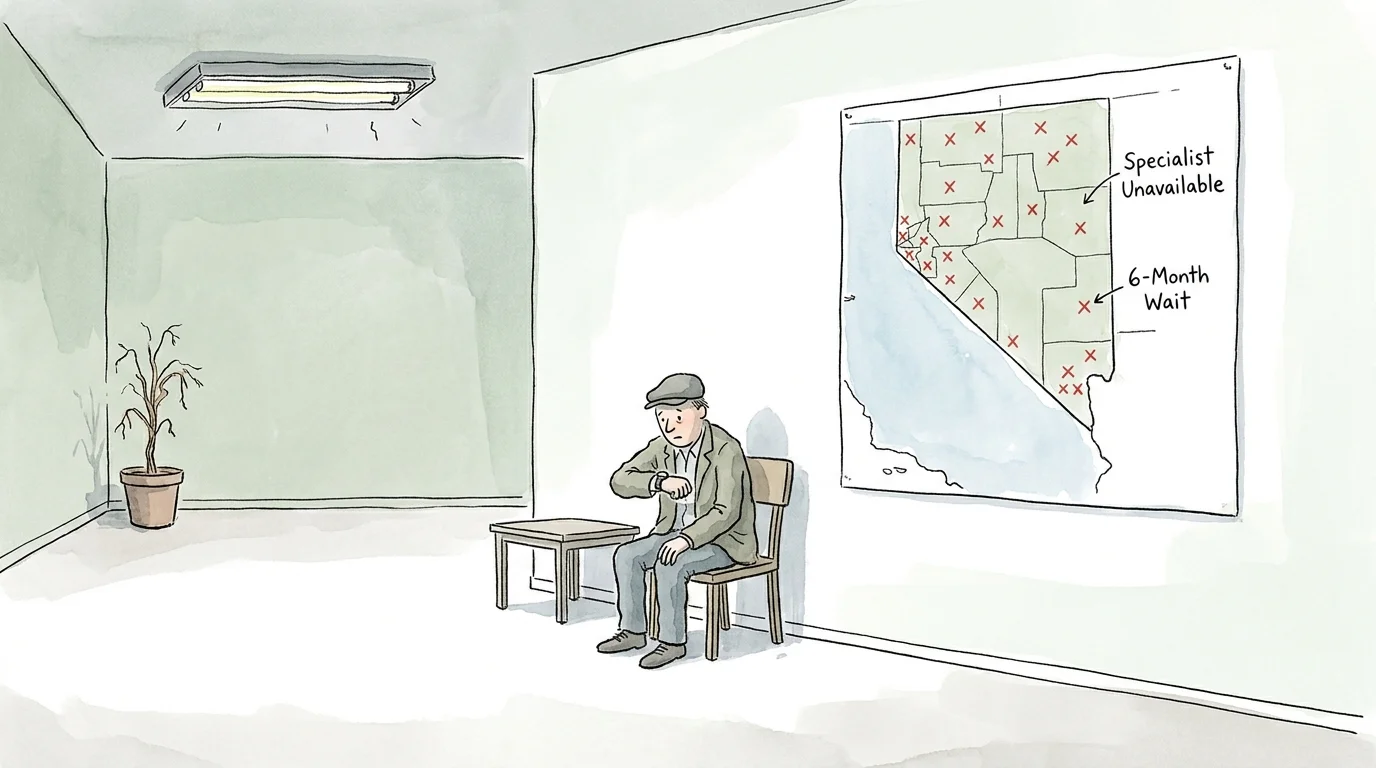

6. Nevada: Healthcare Quality and Specialist Shortages

Las Vegas and Henderson offer incredible tax advantages and abundant entertainment options. Like Texas and Florida, Nevada levies no state income tax, allowing you to keep more of your investment withdrawals. However, Nevada consistently struggles in national rankings for healthcare access and quality.

The state faces a significant, ongoing shortage of specialized physicians. If you develop a complex medical condition—such as specialized cardiac or neurological needs—you might face waiting months for an appointment or traveling out of state to California or Utah to receive top-tier treatment. When you are aging, proximity to world-class healthcare is paramount. Furthermore, combining the soaring desert temperatures with a rapidly rising cost of housing driven by out-of-state buyers means Nevada’s affordability advantage is shrinking fast.

7. South Carolina: Oppressive Humidity and Flooding

Charleston, Beaufort, and Myrtle Beach offer historic charm, fantastic food, and beautiful coastal access. While South Carolina is generally tax-friendly for retirees—it fully exempts Social Security benefits and offers generous deductions for pension income—it does not offer a complete income tax pass like its neighbor to the south.

The most significant downsides, however, are environmental. The summer humidity is thick and oppressive, creating an environment ripe for mold, mildew, and fatigue. Coastal flooding has become a chronic, daily issue in historic districts, with “nuisance flooding” occurring even during standard high tides on sunny days. If you settle on the coast, you will face the constant seasonal threat of hurricanes, requiring you to carry specialized, costly flood and wind-hail insurance policies just to protect your property.

8. Colorado: High Altitude Health Risks

Colorado Springs and the Denver suburbs appeal to highly active seniors seeking mountain views, hiking trails, and endless outdoor recreation. However, the physical reality of living at high altitude cannot be ignored. The elevation can exacerbate underlying cardiovascular and respiratory conditions, making the transition physically difficult for older adults.

The thin air can turn a simple walk to the mailbox into an exhausting chore for those with compromised lung function or heart disease. Beyond the physical toll, Colorado is expensive. Housing costs remain persistently high, and the state levies a flat income tax rate of 4.40%. Additionally, the long, snowy winters can pose significant slipping hazards for seniors and increase social isolation when driving conditions become dangerous.

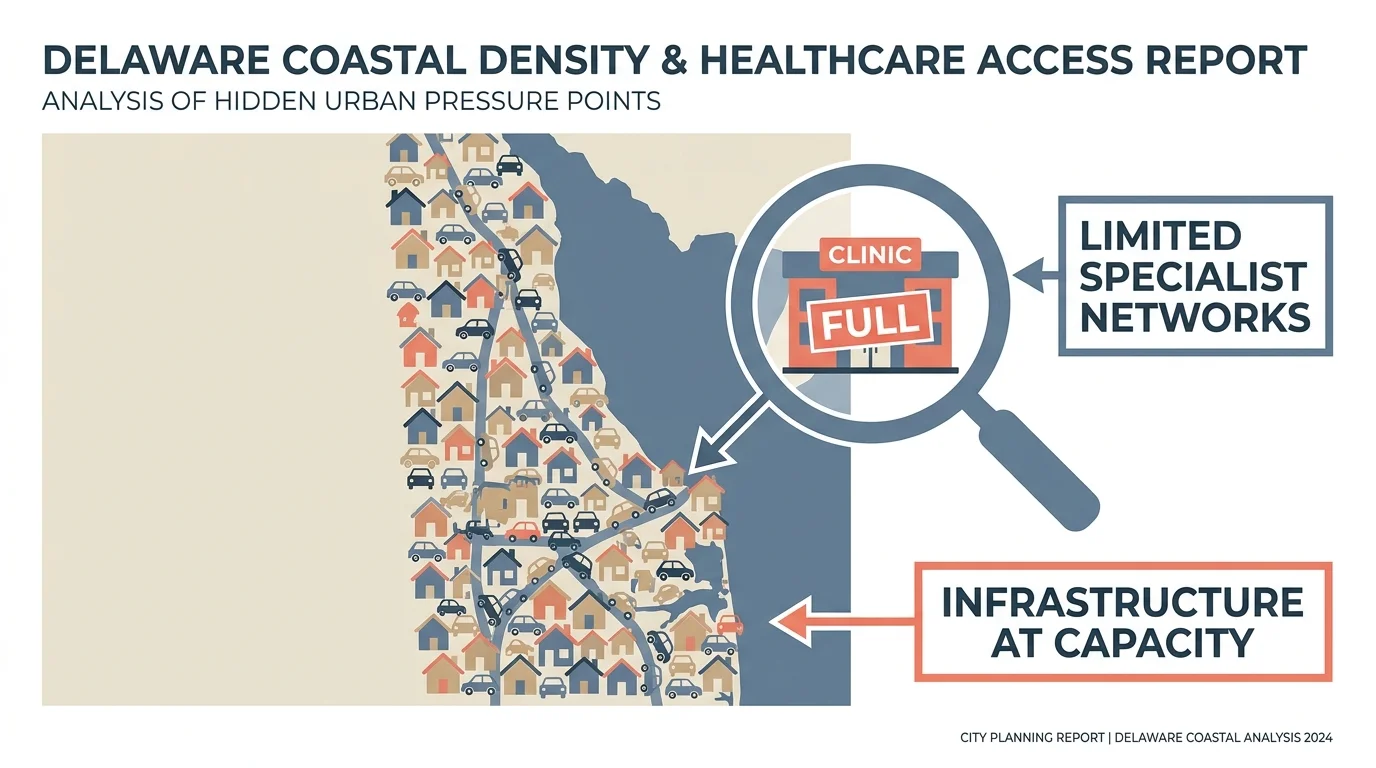

9. Delaware: Crowding and Limited Medical Networks

Coastal Delaware towns like Rehoboth Beach and Lewes attract East Coast retirees looking to escape the high taxes of New Jersey and New York. Delaware boasts zero state sales tax and low property taxes, making it incredibly budget-friendly. The major trade-off is the seasonal population explosion.

During the summer months, quiet beach towns transform into gridlocked tourist hubs, making simple tasks like grocery shopping, visiting the pharmacy, or dining out a major, traffic-filled hassle. Medical care is another pressing concern. While general practitioners are available, the local coastal healthcare system is relatively small. Retirees needing advanced surgical care or specialized oncology often have to drive two hours to Philadelphia or Baltimore. When facing a medical emergency, you want comprehensive medical centers in your backyard, not two states away.

10. Utah: Skyrocketing Costs and Environmental Stress

St. George, Utah, has become a massive hub for retirees drawn to its stunning red rock landscapes, mild winters, and proximity to Zion National Park. Unfortunately, its massive popularity has priced out many prospective movers. Housing costs have skyrocketed over the past five years, officially removing St. George from the list of hidden, budget-friendly retirement spots.

Furthermore, Utah faces severe environmental constraints. Extreme summer heat and deep, ongoing drought conditions mean water conservation is a strict requirement. Retirees who move from the Midwest or East Coast dreaming of lush green lawns or expansive gardens must adapt to a stark, tightly regulated, water-restricted desert reality.

Quick Summary: Tax Trade-Offs in Popular Retirement States

To help you visualize how these different tax systems impact your wallet, review this breakdown of state income tax, sales tax, and property tax burdens. Always verify how these structures interact with the 2026 IRS standard deduction—which sits at $16,100 for single filers and $32,200 for married couples filing jointly—before making a final move.

| State | State Income Tax | Max Combined Sales Tax | Major Tax Downside |

|---|---|---|---|

| Texas | None | Up to 8.25% | High property taxes (~1.49% median rate) |

| Tennessee | None | Up to 9.75% | Highest combined sales taxes in the nation |

| Florida | None | Up to 8.00% | Exploding home insurance premiums |

| Colorado | 4.40% flat rate | Up to 8.30% | State income tax takes a bite from non-exempt income |

| Nevada | None | Up to 8.375% | High sales tax and rising housing costs |

What Can Go Wrong: The Relocation Regret Trap

Many retirees view moving as a fresh start, but failing to perform deep due diligence leads to a phenomenon known as “relocation regret.” Here are the most common pitfalls retirees face when they move to a popular destination:

- Isolating yourself from your support network: Moving thousands of miles away from family and lifelong friends looks easy on paper, but social isolation is a leading cause of depression in older adults. If you require surgery or in-home care, having no local support system creates an immediate crisis.

- Misjudging the true cost of healthcare: Your taxes might be lower, but if you have to fly back to your home state twice a year to see a specialist, or pay exorbitant out-of-network fees because your Medicare Advantage plan does not cover local doctors, you are losing money.

- Renting before buying: Many retirees buy a home immediately upon arriving in a new state, only to realize they hate the summer heat, the tourist traffic, or the local culture. It is always safer to rent for six to twelve months in a new city before liquidating your assets to purchase a home.

- Ignoring extreme weather costs: Paying cash for a home in Florida or the Carolinas does not free you from housing expenses. You must factor in wind mitigation upgrades, flood insurance, and emergency evacuation funds.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

When to Consult a Professional

Because moving across state lines complicates your tax situation, estate plan, and healthcare coverage, consulting a professional before you hire a moving company is highly recommended. Consider seeking help in the following scenarios:

- You have a complex income stream: If you receive income from pensions, real estate, part-time consulting, and standard IRA withdrawals, a Certified Public Accountant (CPA) can help you model exactly how a new state will tax your specific mix of assets.

- You rely on Medicare Advantage: Medicare Advantage (Part C) plans are highly regional. If you move across state lines, you usually trigger a Special Enrollment Period. An independent Medicare broker can tell you if your preferred coverage even exists in your new zip code.

- You need to update your estate plan: Estate laws, probate rules, and power of attorney requirements vary wildly by state. An estate planning attorney in your new location should review your will or trust to ensure it remains legally binding.

Frequently Asked Questions

Do I have to pay state taxes on my Social Security income?

It depends entirely on where you live. The vast majority of states do not tax Social Security benefits at the state level. However, a small handful of states still tax some portion of Social Security depending on your adjusted gross income. If you rely heavily on these benefits, verify the state’s specific tax code via the Internal Revenue Service (IRS) and the local state department of revenue.

How do property taxes affect retirees on fixed incomes?

Property taxes can be devastating to a fixed budget because they are tied to local real estate values, not your personal income. If you move to a state like Texas, a booming housing market will increase your home’s assessed value, triggering a larger annual tax bill even if your retirement income has not changed. Look for states that offer property tax freezes or substantial homestead exemptions for seniors.

Will Original Medicare cover my medical care if I move to a different state?

Yes. Original Medicare (Part A and Part B) is a federal program and is accepted by any provider nationwide that takes Medicare. However, if you are enrolled in a Medicare Advantage plan, you are bound by regional provider networks. Moving out of your plan’s service area requires you to select a new plan or return to Original Medicare.

Next Steps for Your Relocation Plan

Identifying the downsides of popular retirement locations does not mean you shouldn’t move; it simply means you need to plan with your eyes wide open. Do not let pristine golf courses and sunny marketing materials blind you to the realities of local taxes, insurance markets, and healthcare infrastructure. Take the time to build a sample budget based on real, local costs. Rent a property in your target city during its worst weather season—whether that is the dead of a humid summer or the peak of a snowy winter—to see how you tolerate the environment.

By conducting thorough research, testing out the location, and consulting with financial professionals, you can confidently choose a community that supports both your lifestyle desires and your long-term financial security.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.