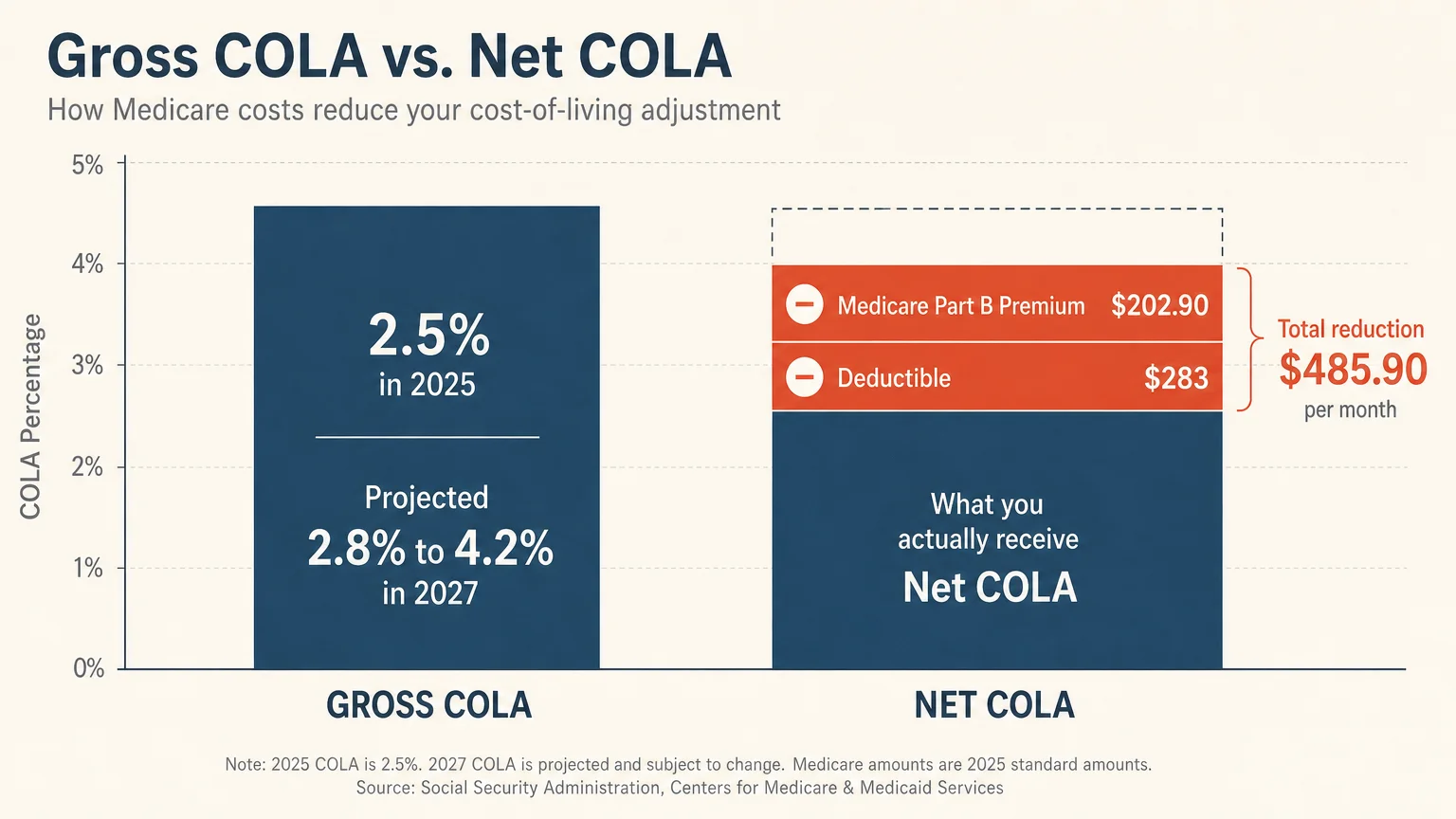

Retirees face a severe purchasing power crisis as projected 2027 Social Security cost-of-living adjustments struggle to match skyrocketing healthcare expenses. With Medicare Part B premiums jumping nearly 10% to $202.90 a month in 2026, relying solely on the government to offset your rising costs guarantees a financial shortfall. Taking control of your personal inflation rate requires immediate action. By actively managing your healthcare coverage, optimizing tax strategies, and creating inflation-resistant income streams, you can build a personalized safety net that outpaces official estimates. You do not have to accept a declining standard of living. Implementing these five targeted financial moves today will secure your purchasing power regardless of what the Social Security Administration announces next October.

The Reality of the 2027 Social Security COLA

The Social Security Administration relies on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the year to determine the following year’s COLA. In 2025, beneficiaries received a modest 2.5% increase. As we look ahead to the 2027 announcement, early estimates from groups like The Senior Citizens League and independent analysts project an adjustment anywhere from 2.8% to 4.2%, depending on whether recent inflation spikes persist.

However, focusing purely on the top-line percentage creates a false sense of financial security. Your “gross COLA” is the official number announced in October, but your “net COLA” is the actual money that hits your bank account after mandatory healthcare deductions.

In 2026, the standard Medicare Part B premium surged to $202.90 per month—an increase of nearly 10% from the previous year—while the annual Part B deductible climbed to $283. If your living expenses grow faster than the generalized inflation index, your real-world standard of living declines. Building your own COLA means creating independent mechanisms to bridge that gap.

1. Plug the Medicare Premium Leak

Medicare costs act as a silent drain on your retirement income. Because Part B premiums are deducted automatically from your Social Security benefits before the money is ever deposited into your account, a significant premium hike can consume your entire COLA raise. To build your personal inflation shield, you must aggressively manage your healthcare expenses.

Every fall during the Medicare Annual Enrollment Period (AEP), re-evaluate your Part D prescription drug coverage and Medicare Advantage plans. Insurance companies change their formularies and network providers annually. A medication that cost you a $10 copay last year might be moved to a higher tier, suddenly costing you $50 or more per month. By utilizing the official plan finder on Medicare.gov, you can input your exact prescriptions and find the most cost-effective coverage for the upcoming year.

Furthermore, high-income retirees must stay vigilant regarding the Income-Related Monthly Adjustment Amount (IRMAA). For 2026, if your modified adjusted gross income from two years prior exceeded $109,000 as a single filer or $218,000 as a married couple filing jointly, you are required to pay an IRMAA surcharge. This surcharge can push your monthly Part B premium from $202.90 to $284.10, or even as high as $594.00 for the highest earners.

If you experienced a life-changing event—such as full retirement, a divorce, or the death of a spouse—that caused your income to drop significantly, you do not have to accept the surcharge passively. File Form SSA-44 with the Social Security Administration to request a new IRMAA determination based on your current, lower income. A successful appeal instantly restores hundreds of dollars to your monthly budget, acting as a massive, self-created COLA.

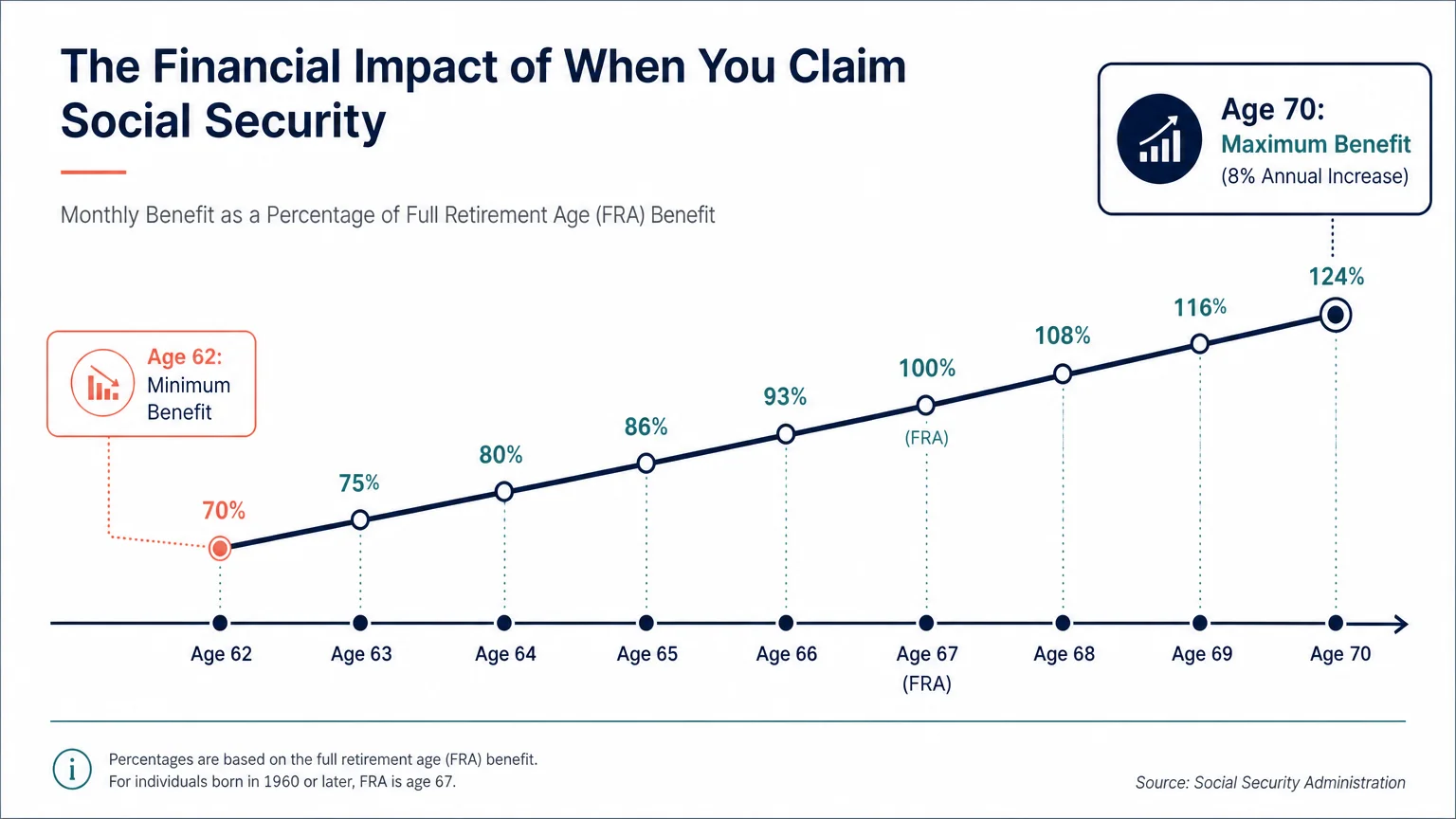

2. Maximize the Ultimate COLA: Delayed Claiming

If you have not yet filed for Social Security, the most mathematically powerful inflation hedge you possess is patience. Social Security is one of the few guaranteed income streams backed by the federal government that adjusts for inflation automatically.

Your base benefit amount is determined by your highest 35 years of earnings, calculated at your Full Retirement Age (FRA). However, for every single year you delay claiming past your FRA up to age 70, your benefit increases by a guaranteed 8%. This is known as the delayed retirement credit.

Consider the compounding math. If your FRA benefit is $2,000 per month, waiting three years until age 70 increases your base payout to $2,480—a 24% boost. When a future COLA is applied, it multiplies against this larger base figure. A 3% COLA on a $2,000 benefit yields an extra $60 per month. That exact same 3% COLA applied to a $2,480 benefit yields an extra $74.40 per month.

Over a twenty-year retirement, the compounding effect of delayed claiming creates tens of thousands of dollars in additional, inflation-protected income. While drawing from your investment portfolio early to bridge the gap between retirement and age 70 requires careful planning, the guaranteed return of delayed Social Security provides unparalleled protection against soaring costs.

3. Create an Inflation-Protected Yield Reserve

Allowing your cash reserves to sit in a traditional checking account earning negligible interest is a guaranteed way to lose purchasing power. To build a robust personal COLA, your safe money must work actively to offset inflation.

“Inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital.” — Warren Buffett, Investor and CEO of Berkshire Hathaway

You can protect your capital by structuring an inflation-protected yield reserve using specific fixed-income vehicles:

| Asset Type | How It Fights Inflation | Best Used For |

|---|---|---|

| Series I Savings Bonds | Interest rates are pegged directly to inflation, protecting the principal’s buying power. | Long-term cash reserves; funds cannot be accessed for the first year. |

| TIPS (Treasury Inflation-Protected Securities) | The principal value adjusts upward with inflation and downward with deflation. | Fixed-income portfolio diversification and principal protection. |

| High-Yield Savings Accounts (HYSAs) & CDs | Offer competitive interest rates that respond favorably to the Federal Reserve’s benchmark rate policies. | Emergency funds and short-term liquidity needs. |

4. Slash Your Personal Inflation Rate with Targeted Property Tax Relief

When discussing inflation, most attention goes to the grocery store and the gas pump. However, housing costs remain the largest line item in the average retiree’s budget. Because the Social Security CPI-W formula heavily weights the spending habits of younger, working-age individuals, it often fails to accurately capture the specific inflation seniors experience regarding property taxes and home maintenance.

You can create a personal COLA by aggressively lowering your fixed overhead. Property taxes, in particular, have surged alongside rising home valuations. If you live in a state with rapidly appreciating real estate, your local tax assessment can climb relentlessly, draining your fixed income.

Fortunately, many states and local municipalities offer targeted tax relief for seniors. Depending on your location and income level, you may qualify for a property tax freeze, which locks in your tax bill at its current level regardless of future home valuations. Other jurisdictions offer outright exemptions that slash a percentage off your assessed value.

Contact your county assessor’s office immediately to determine the application deadlines for senior property tax relief. Additionally, leverage resources provided by the National Council on Aging (NCOA) to explore utility assistance programs, such as the Low Income Home Energy Assistance Program (LIHEAP), and free home weatherization services offered by local utility companies. Lowering your monthly output is mathematically identical to increasing your monthly income.

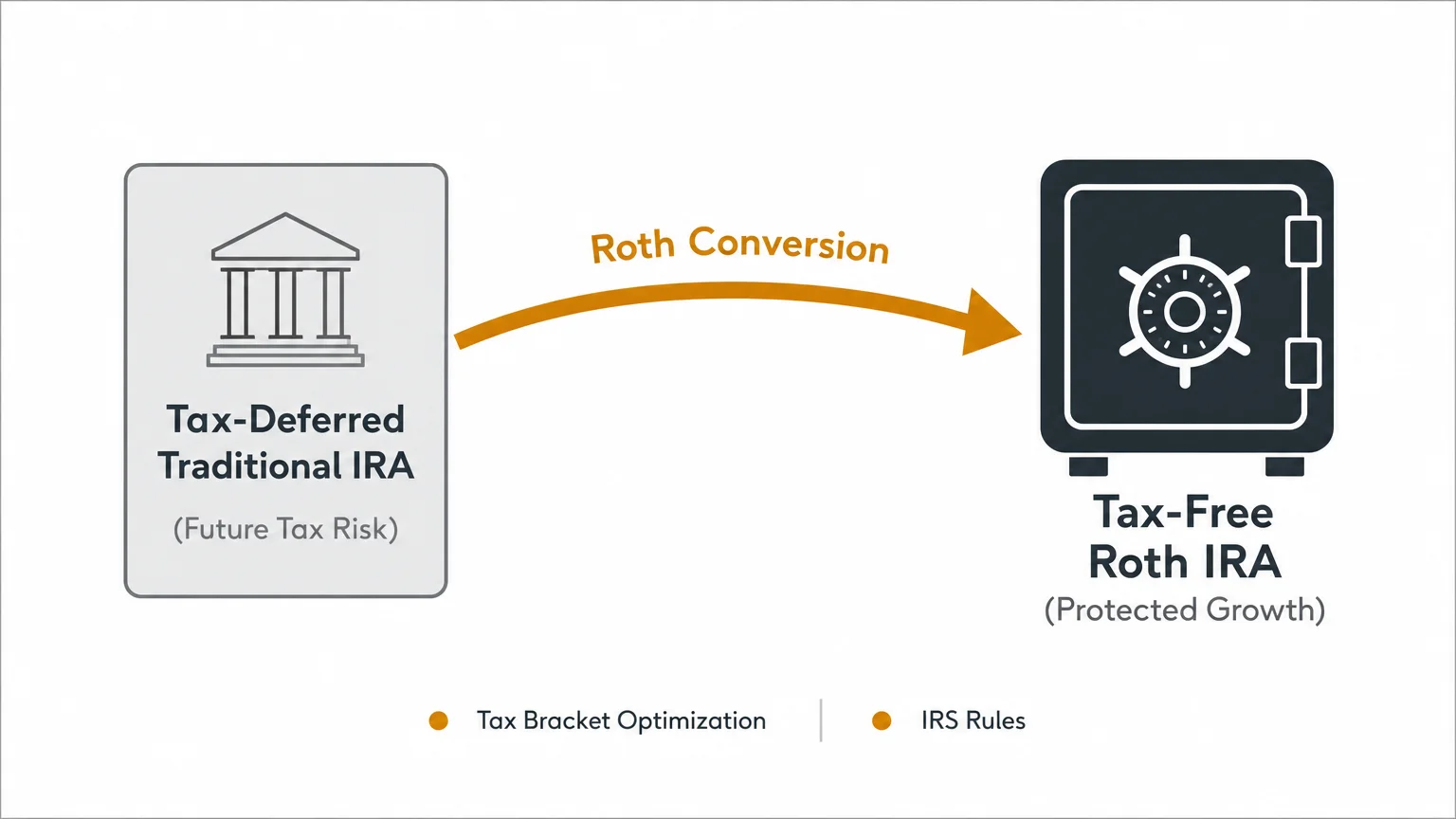

5. Build Tax-Free Reserves with Roth Conversions

Taxes represent a massive, ongoing liability that threatens your purchasing power. Withdrawals from traditional IRAs and 401(k)s are taxed as ordinary income. If tax rates rise in the future to manage the national deficit, your required minimum distributions (RMDs) will trigger larger tax bills, leaving you with less money to spend.

“Taxes will be the single biggest factor that separates people from their retirement dreams.” — Ed Slott, CPA and Retirement Tax Expert

You can defend your income by taking advantage of current Internal Revenue Service contribution limits and strategic Roth conversions. For 2026, the IRS allows individuals aged 50 and older to contribute up to $8,000 to an IRA. Furthermore, executing a Roth conversion involves voluntarily transferring pre-tax money from a traditional IRA into a Roth IRA. While you must pay income taxes on the converted amount in the year you make the transfer, all future growth and withdrawals become completely tax-free.

Roth IRAs do not force you to take RMDs during your lifetime. This allows your money to continue compounding without interference, providing a flexible pool of tax-free capital that you can tap into if a smaller-than-expected COLA fails to meet your needs. By paying taxes proactively when brackets are favorable, you insulate your future spending power from legislative risks.

Professional vs. Self-Guided: Managing Your Inflation Risk

Building an independent COLA involves a sophisticated mix of healthcare choices, tax optimization, and investment strategies. Depending on your financial complexity, you must decide how to manage this process:

- The Self-Guided Retiree: If your income is well below the IRMAA surcharge threshold, and your portfolio relies primarily on Social Security and standard savings, you can manage many of these steps independently. You can optimize your Medicare Part D coverage annually on Medicare.gov and open high-yield savings accounts without professional intervention.

- The Fiduciary Financial Planner: If you are within five years of retirement and debating when to claim Social Security, a fee-only Certified Financial Planner (CFP) is highly recommended. A professional planner can run detailed breakeven analyses that factor in assumed inflation rates, helping you determine exactly how much value you gain from delayed claiming.

- The CPA or Tax Strategist: If you plan to execute multi-year Roth conversions or need to file an SSA-44 for an IRMAA appeal, working with a qualified tax professional is essential. Miscalculating a Roth conversion can unintentionally push you into a higher tax bracket, triggering the exact Medicare premium surcharges you are trying to avoid.

Common Mistakes to Avoid When Building Your COLA

As you take steps to secure your purchasing power, be careful to avoid these frequent retirement planning errors:

- Chasing High Yields Recklessly: In a desperate bid to beat inflation, some retirees shift their safe cash reserves into volatile dividend stocks or high-risk junk bonds. While these assets offer attractive yields, they expose your principal to severe market downturns. Keep your emergency reserves strictly in guaranteed, principal-protected vehicles.

- Misunderstanding the “Hold Harmless” Provision: This federal rule dictates that your Social Security check cannot decline from year to year simply because the standard Medicare Part B premium increased more than your COLA. However, this protection is not universal. It does not apply if you are newly enrolling in Medicare, if you pay an IRMAA surcharge, or if your Part B premiums are billed directly to you rather than deducted from Social Security.

- Filing for Social Security Early Out of Fear: Claiming benefits at age 62 solely because you are afraid of inflation or government solvency locks in a permanently reduced payout. By voluntarily shrinking your base benefit, you guarantee that all future COLAs will generate mathematically smaller dollar amounts for the rest of your life.

Frequently Asked Questions

How is the Social Security COLA calculated?

The Social Security Administration calculates the annual COLA based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). They compare the average CPI-W data from the third quarter (July, August, and September) of the current year to the same period from the previous year. If there is an increase, benefits are adjusted upward by that percentage.

Will the 2027 COLA cover my rising Medicare premiums?

It depends entirely on the final COLA percentage and your specific benefit amount. Because the 2026 standard Part B premium increased to $202.90, retirees with smaller Social Security checks often find that the flat-dollar increase in Medicare premiums consumes the majority of their percentage-based COLA raise.

Can I reverse my Social Security claiming decision if I made a mistake?

Yes, but under strict conditions. If you claimed your benefits within the last 12 months, you can withdraw your application by filing Form SSA-521. However, you must repay all the benefits you and your family received during that time. Once repaid, your record is wiped clean, allowing your benefit to grow again until you reapply later.

Securing your retirement against inflation requires shifting your mindset from passive reliance to active management. By plugging the leaks in your healthcare coverage, optimizing your tax strategies, and treating your safe cash as a working asset, you can build a personalized safety net that far exceeds the government’s standard adjustments. Take action today to review your Medicare plan, audit your property taxes, and consult a professional about Roth conversions to fortify your financial future.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.