When you look at the average Social Security check of $2,082 per month in 2026, you quickly realize that retirement requires more than relying on a single government income stream. While the 2.8 percent cost-of-living adjustment boosted benefits this year, everyday expenses, rising Medicare premiums, and housing costs consistently outpace these modest increases. Understanding exactly how far this money stretches is the first step toward building a resilient financial strategy. Whether you are already collecting benefits or mapping out your timeline, you must know what this baseline income handles—and exactly where you need to fill the gaps with your own savings to maintain your desired lifestyle.

The Reality of the Average Social Security Check in 2026

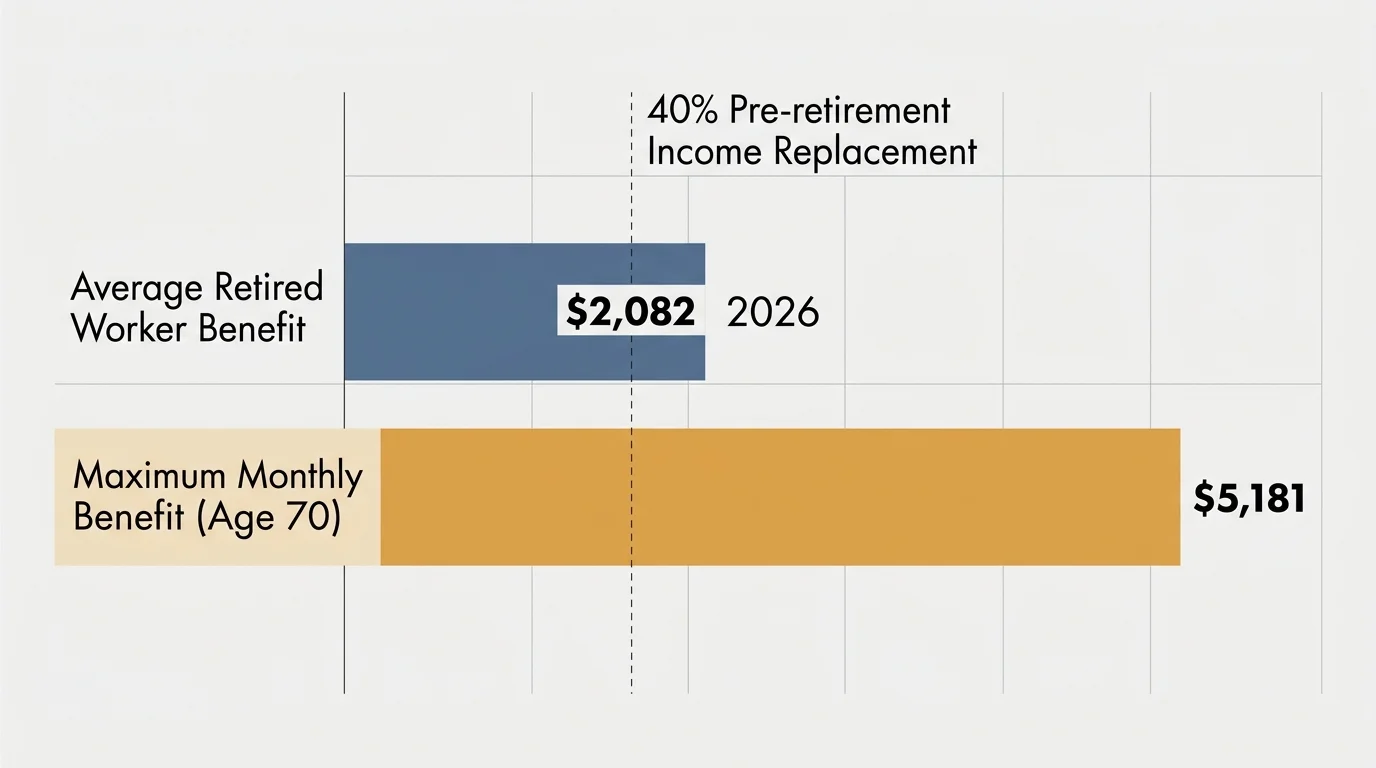

If you retired this year, your monthly income from the Social Security Administration looks vastly different than it did for retirees just a decade ago. As of mid-2026, the average retired worker receives approximately $2,082 a month. However, focusing solely on the average can easily create a false sense of security. The absolute maximum monthly benefit a worker can receive in 2026—assuming they earned the maximum taxable amount for 35 years and delayed claiming until age 70—is $5,181. Conversely, those who claimed early with lower lifetime earnings receive significantly less.

The system was designed to replace roughly 40 percent of an average worker’s pre-retirement income. For lower earners, it replaces a slightly higher percentage; for high earners, it replaces much less. The recent 2.8 percent cost-of-living adjustment (COLA) implemented in January 2026 offered a slight buffer against inflation, but many retirees find that the specific basket of goods they purchase—healthcare, prescription medications, and utilities—rises at a much steeper rate than the broad Consumer Price Index (CPI-W) used to calculate the COLA.

What the Average Check Actually Covers

Living on roughly $25,000 a year from Social Security requires meticulous financial discipline. If you rely heavily on this income, you must optimize every dollar. For retirees who enter their golden years completely debt-free, the average check provides a functional baseline for essential living expenses.

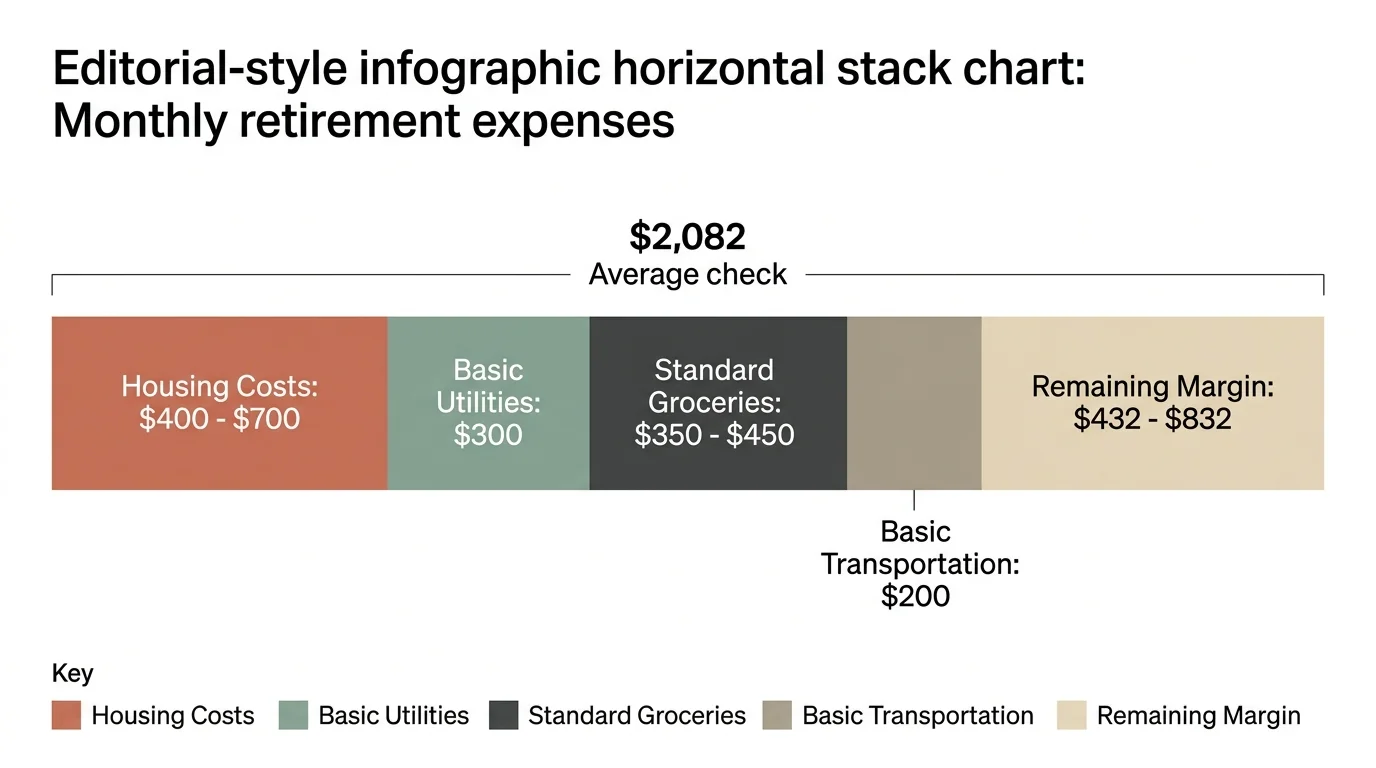

Here is what an average check can reliably cover in most parts of the country:

- Paid-Off Housing Costs: Even without a mortgage, homeownership carries persistent costs. Property taxes, homeowners insurance, HOA fees, and basic maintenance average $400 to $700 per month depending on your state. Your check can cover this, provided no catastrophic repairs arise.

- Basic Utilities: Electricity, water, garbage collection, and internet services run roughly $300 a month in the average American household.

- Standard Groceries: The cost of food remains high. A modest grocery budget for a single retiree optimizing meals at home sits between $350 and $450 per month.

- Basic Transportation: If you own a reliable, paid-off vehicle, budgeting $200 a month for gas, standard insurance, and routine oil changes is feasible.

If your housing is fully paid for, these essential expenses consume roughly $1,300 to $1,650 of your $2,082 check. That leaves a narrow margin for everything else—a margin that vanishes quickly when you factor in healthcare.

The Healthcare Bite: Medicare Premiums and Out-of-Pocket Costs

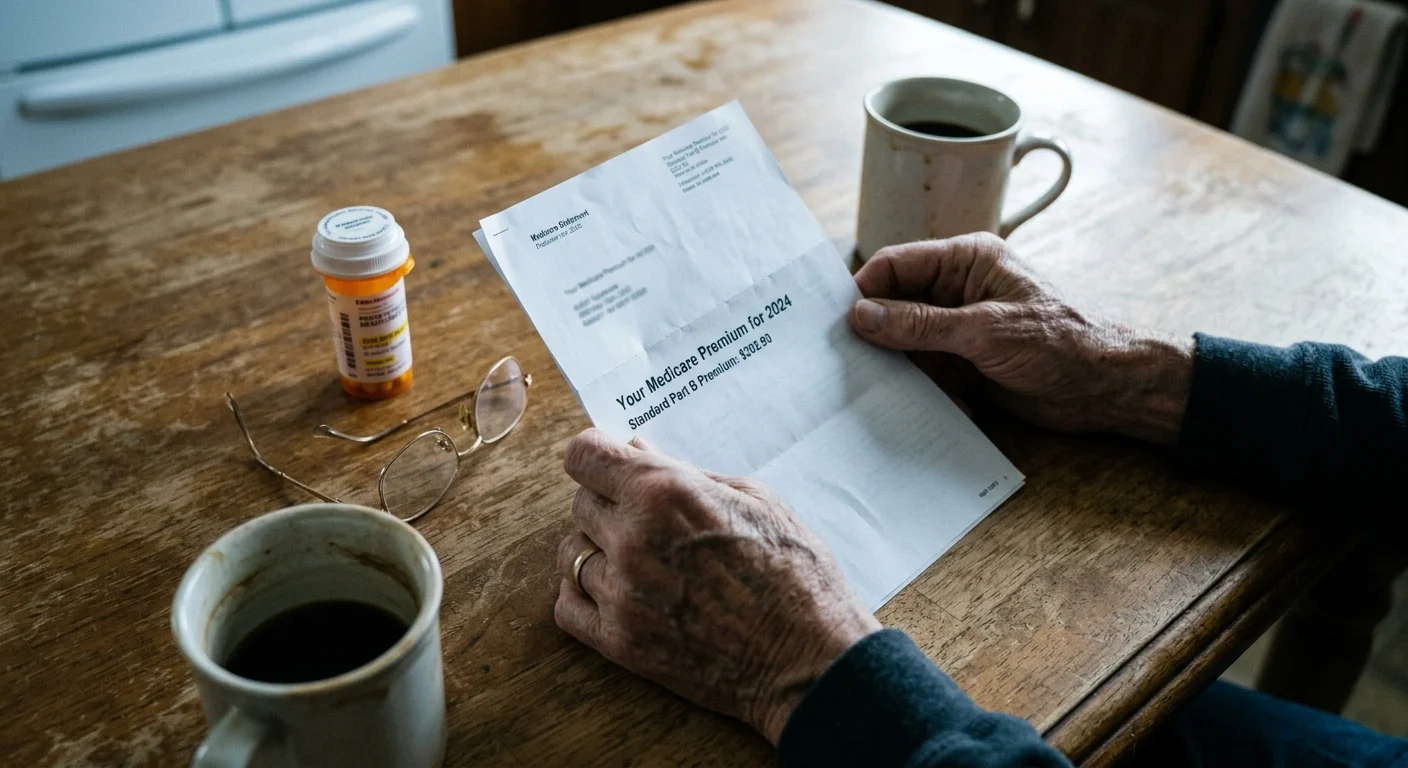

Healthcare is the most significant and consistent drain on retirement income, and it starts before the money even hits your checking account. When you turn 65 and enroll in Medicare, your Part B premium is automatically deducted from your Social Security benefit.

In 2026, the standard Medicare Part B premium is $202.90 per month. Immediately, the average $2,082 check drops to a net payout of $1,879.10. But Part B only covers 80 percent of outpatient medical costs; you are responsible for the remaining 20 percent, with no out-of-pocket maximum. To protect against ruinous medical debt, most retirees purchase supplemental coverage.

When you account for a Medicare Supplement (Medigap) policy, a standalone Part D prescription drug plan, and out-of-pocket costs for dental, vision, and hearing—which Original Medicare does not cover—a healthy retiree can expect to spend $400 to $600 a month on total healthcare expenses. If you are a higher earner, you must also navigate the Income-Related Monthly Adjustment Amount (IRMAA), a surcharge that can push your Medicare Part B and Part D premiums significantly higher. You can verify current premium tiers directly through Medicare.gov.

What Your Social Security Check Won’t Cover

The limitations of the average benefit become glaringly apparent when you face major life events, taxation, and long-term care needs. Social Security is simply not scaled to absorb the heavy financial shocks common in the later stages of life.

One of the most profound expenses seniors face is long-term care. Whether it involves hiring an in-home aide or transitioning to a dedicated community, the costs far exceed government benefits. According to 2026 data, the national median cost of independent living is $3,200 per month, while assisted living averages $5,419. The average Social Security check cannot even cover a fraction of advanced care needs.

| Living Expense Category | Average Monthly Cost (2026) | Percentage of Average SS Check ($2,082) |

|---|---|---|

| Medicare Part B Premium | $202.90 | 9.7% |

| Independent Senior Living | $3,200.00 | 153% |

| Assisted Living Facility | $5,419.00 | 260% |

| Memory Care Facility | $6,690.00 | 321% |

Furthermore, many retirees are shocked to discover they owe income taxes on their Social Security benefits. The taxation thresholds, known as provisional income limits, were established in the 1980s and have never been indexed for inflation. If your combined income (adjusted gross income plus non-taxable interest plus half of your Social Security benefits) exceeds $25,000 as a single filer or $32,000 as a married couple filing jointly, up to 50 percent of your benefits become taxable. If your combined income surpasses $34,000 (single) or $44,000 (joint), up to 85 percent of your benefits are subject to federal income tax. You can review the exact worksheets at the Internal Revenue Service (IRS) website.

How Claiming Age Changes Your Monthly Picture

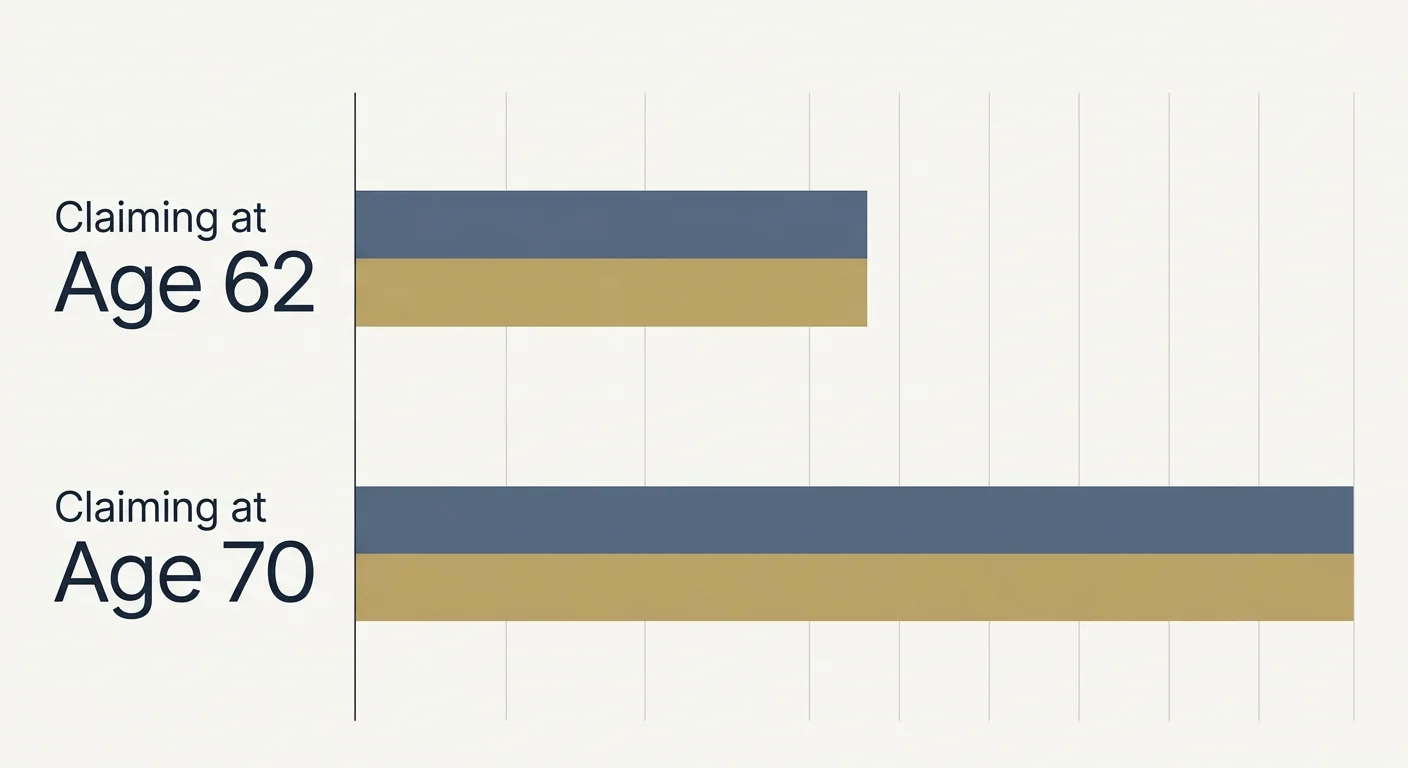

The $2,082 average reflects a blend of millions of retirees who claimed at various ages. Your specific claiming strategy remains the most powerful lever you have to increase your guaranteed lifetime income.

You can claim benefits as early as age 62, but doing so results in a permanent reduction of up to 30 percent compared to your Full Retirement Age (FRA) amount. For anyone born in 1960 or later, FRA is 67. If you wait beyond your FRA, the Social Security Administration credits you with an 8 percent increase for every year you delay, up until age 70. A $2,000 benefit at age 67 transforms into a $2,480 benefit at age 70—a permanent 24 percent boost that also maximizes the dollar value of every future COLA.

“The most important retirement decision you make is not what you invest in, but when you claim Social Security. Deferring until age 70 is the best guaranteed return you can get in any market environment.” — Jean Chatzky, Financial Expert and Author

Delaying is not just about your own income; it is fundamentally about protecting your spouse. When one spouse passes away, the surviving spouse is entitled to the larger of the two benefit checks, but the smaller check disappears entirely. A maximized age-70 benefit ensures the surviving spouse has the highest possible baseline income when the household experiences the “widow’s penalty” of reduced total income.

Common Mistakes to Avoid

Failing to understand the nuances of Social Security can lead to permanent financial consequences. Ensure you avoid these critical missteps:

- Assuming benefits are completely tax-free: As mentioned, up to 85 percent of your benefit can be subject to federal taxation. Additionally, certain states also tax Social Security income. Always calculate your net benefit, not just your gross.

- Forgetting to coordinate spousal benefits: Married couples often claim in a vacuum rather than coordinating their dates. Having the higher earner delay until 70 while the lower earner claims early can often optimize cumulative lifetime benefits.

- Earning too much while claiming early: If you claim Social Security before your Full Retirement Age and continue to work, you are subject to the earnings test. In 2026, if you earn over the specified annual limit, the SSA will withhold $1 in benefits for every $2 you earn above the threshold.

- Ignoring the official record: Check your earnings record annually via the Social Security Administration portal. If an employer failed to report a year of your earnings accurately, your primary insurance amount will be permanently calculated at a lower rate unless you correct the error.

Professional vs. Self-Guided

Bridging the gap between a $2,082 monthly check and your actual living expenses requires a strategic drawdown of your personal assets. Deciding whether to manage this yourself or hire a professional depends on your specific financial architecture.

Self-Guided Strategies: You can likely manage your own retirement income plan if your situation is straightforward. This applies if your primary assets are held in a single traditional IRA or 401(k), your home is completely paid off, and you have no complex tax considerations. Simple adherence to a conservative withdrawal rate and utilizing standard Medicare options may be sufficient.

Professional Guidance Required (Tax Optimization): If your wealth is spread across pre-tax 401(k)s, taxable brokerage accounts, and Roth IRAs, a financial planner can help you execute strategic Roth conversions. Drawing down the right accounts in the right order can keep your provisional income low enough to reduce taxes on your Social Security benefits and prevent you from triggering Medicare IRMAA surcharges.

Professional Guidance Required (Complex Family Dynamics): If you are navigating a divorce and want to claim benefits on an ex-spouse’s record, or if you are coordinating benefits for a disabled dependent, professional advice is vital. The rules surrounding survivor benefits, ex-spousal claims, and government pension offsets are unforgiving; one wrong filing can permanently lock you into a lower payment.

Actionable Steps to Bridge the Income Gap

Because the average Social Security check cannot single-handedly support a comfortable retirement, you must actively architect your supplementary income. Start by calculating your baseline expenses—housing, food, healthcare, and insurance. Compare that number to your projected Social Security benefit.

The difference between those two numbers is your mandatory income gap. To fill it, look to your investment portfolio. Historically, financial planners leaned on the 4 percent rule—withdrawing 4 percent of a portfolio’s value in the first year of retirement and adjusting for inflation thereafter. In today’s economic climate, many experts advise a slightly more conservative withdrawal rate, closer to 3.5 percent, to account for market volatility and longer life expectancies.

If your portfolio cannot sustain the necessary withdrawals to bridge the gap, you have three primary levers: reduce your fixed expenses by downsizing or relocating to a tax-friendly state, delay your retirement to allow your investments to grow while increasing your Social Security benefit, or create a bridge income stream through part-time consulting or a scaled-back job during your early retirement years.

Strategic Next Steps

The average Social Security check serves as the foundation of your retirement house, but it was never designed to be the roof and walls. Take the time today to pull your current statement from the SSA, estimate your Medicare premiums, and project your actual living expenses.

Building a comfortable retirement means acknowledging the limitations of government benefits and actively planning for the shortfall. By understanding the math now, you give yourself the runway to make precise adjustments, ensuring your money lasts exactly as long as you do.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: July 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.