Each year, millions of Americans eagerly await the Social Security cost-of-living adjustment announcement, wondering exactly how much their monthly income will change. For 2026, the official 2.8% increase means you will see a higher gross amount deposited into your bank account. However, that top-line raise does not tell the whole story. Because Medicare Part B premiums and shifting tax brackets directly impact your bottom line, your actual net check might look surprisingly different. Understanding the exact calculations behind your 2026 benefits allows you to adjust your retirement budget and protect your purchasing power. By breaking down the latest earning limits, tax rules, and healthcare deductions, you can navigate these upcoming changes with absolute financial confidence.

How the 2026 COLA Adjusts Your Gross Benefit

The annual cost-of-living adjustment serves as a critical defense against inflation for retirees living on a fixed income. For 2026, the Social Security Administration implemented a 2.8 percent COLA. This adjustment is permanently applied to your base benefit, raising the baseline upon which all future adjustments will be calculated.

The government calculates this figure using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the previous year. If the index shows an increase in the cost of basic consumer goods, your gross benefits rise correspondingly. While a 2.8 percent raise is slightly higher than the 2.5 percent adjustment applied in 2025, you might find it still falls short of your everyday expenses. Healthcare costs, housing, and utilities often increase at a faster pace than the general consumer goods measured by the CPI-W.

Looking ahead, economic pressures continue to shift the landscape. Due to mid-2026 inflation data, early projections indicate that the 2027 COLA could potentially land between 3.8 percent and 4.7 percent. While projections change frequently, tracking these numbers helps you model your future guaranteed income. You can verify your exact 2026 benefit amount by logging into your personal my Social Security account on the SSA website.

The Hidden Bite: Medicare Part B Premiums

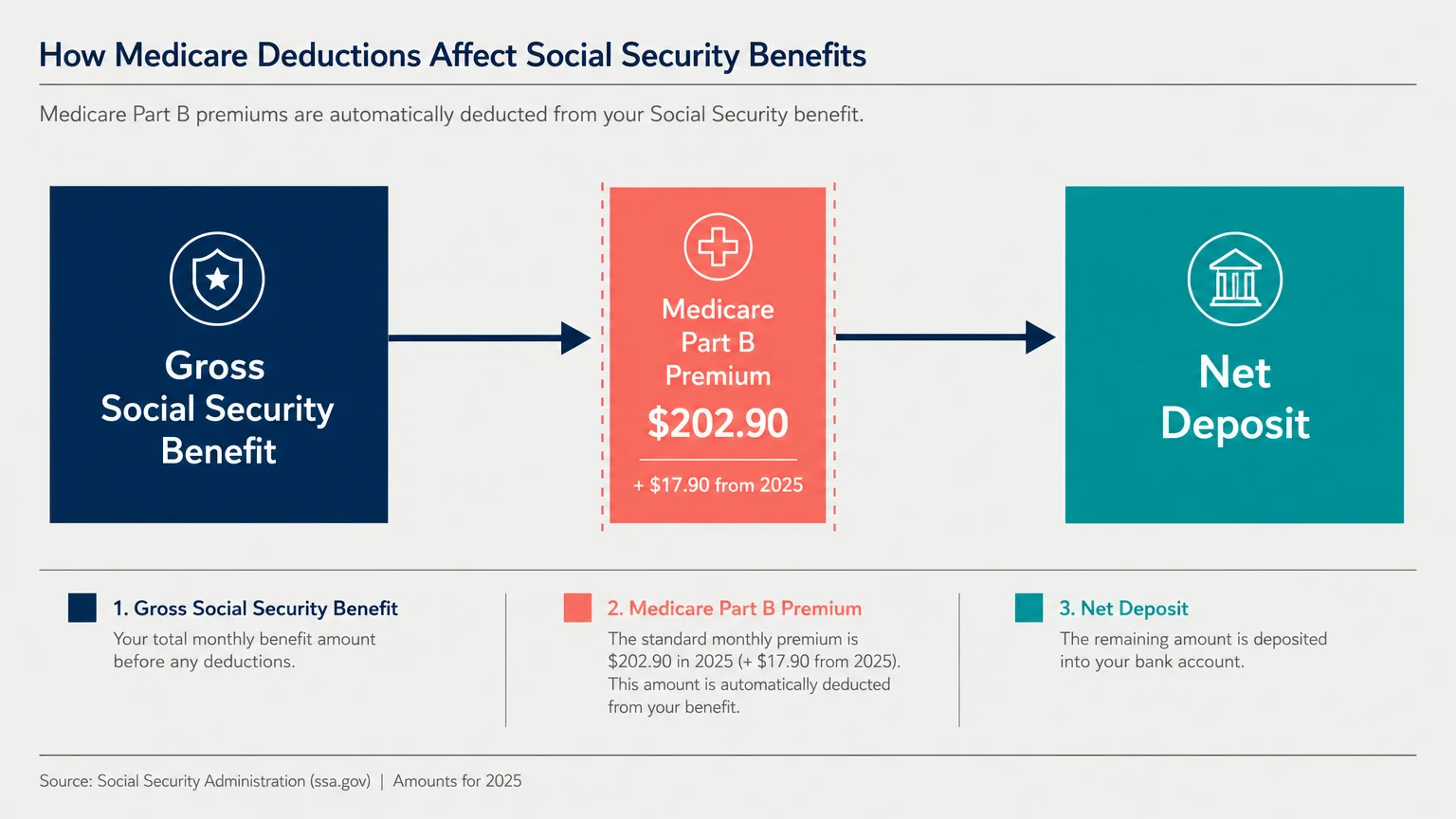

Evaluating your Social Security check in a vacuum ignores the single largest automatic deduction most retirees face: Medicare Part B premiums. Because the federal government deducts your Medicare premiums directly from your Social Security payments before the money ever reaches your checking account, healthcare costs dictate your actual net income.

For 2026, the standard monthly premium for Medicare Part B enrollees is $202.90. This represents a $17.90 jump from the $185.00 base rate applied in 2025. The annual Part B deductible also increased from $257 to $283. If your Social Security COLA added an extra $45 to your gross monthly check, the $17.90 Medicare hike instantly consumed a significant chunk of that raise.

Furthermore, if you generated substantial income prior to retiring, you may fall victim to the Income-Related Monthly Adjustment Amount (IRMAA). Medicare looks at your tax returns from two years prior to determine your surcharge. For 2026, the high-income threshold increased to $109,000 for a single individual and $218,000 for a married couple filing jointly. Crossing these lines triggers premium surcharges that drastically reduce your net Social Security check. Staying informed on current rates via Medicare.gov ensures you are never surprised by an IRMAA deduction.

Working While Collecting: 2026 Earnings Limits

A common reality for modern retirees is the desire or financial necessity to continue working. You are perfectly free to work while collecting Social Security, but if you claim benefits before reaching your Full Retirement Age (FRA)—which is 67 for anyone born in 1960 or later—the government limits how much wage income you can earn before they temporarily withhold your benefits.

For 2026, the specific earnings limits are strictly enforced:

- Under Full Retirement Age: If you are under your full retirement age for the entirety of 2026, the annual earnings limit is $24,480. The Social Security Administration will deduct $1 from your benefits for every $2 you earn above this threshold.

- The Year You Reach Full Retirement Age: In the year you reach your full retirement age, the rules become much more lenient. The limit on your earnings for the months prior to your birthday jumps to $65,160. The penalty also drops; the SSA withholds only $1 for every $3 you earn above the cap.

- After Full Retirement Age: Once you hit your birthday month, the earnings limit disappears completely. You can earn an unlimited amount of income without facing any benefit reductions.

It is crucial to understand that these withheld benefits are not permanently lost. When you finally reach your FRA, the Social Security Administration automatically recalculates your monthly benefit amount to give you credit for the months they withheld payments, resulting in a permanently higher monthly check moving forward.

The Impact of the Rising Social Security Wage Base

While retirees focus heavily on benefit payouts, those still participating in the workforce must monitor the Social Security wage base. You only pay the 6.2 percent Social Security payroll tax on earnings up to a specific limit; income beyond that cap goes untaxed by the SSA.

The maximum taxable earnings limit—often referred to as the wage base—rose to $184,500 for 2026. This is a notable increase from the $176,100 limit in 2025. If you are a high earner still working toward retirement, this means a slightly larger portion of your paycheck will go toward FICA taxes this year. However, consistently hitting this maximum wage base over your 35 highest-earning working years is the exact strategy required to unlock the maximum possible retirement payout.

A worker who waits until age 70 to claim benefits in 2026 can secure a maximum Social Security benefit of $5,181 per month. Most retirees receive far less—the average benefit sits closer to $2,071—but understanding the absolute ceiling helps frame the value of delaying your claim if your savings allow for it.

How Taxes Can Alter Your Net Payment

Even if your gross Social Security check increases significantly, federal taxes can silently consume a large portion of your benefit. To determine whether your Social Security is taxable, the Internal Revenue Service uses a formula called “provisional income” or “combined income.”

You calculate this figure by taking your Adjusted Gross Income (AGI), adding any non-taxable interest (such as municipal bond yields), and finally adding 50 percent of your annual Social Security benefits. Once you have your combined income, the IRS applies the following thresholds:

- Single Filers: A combined income between $25,000 and $34,000 means up to 50 percent of your benefits become taxable. If your combined income exceeds $34,000, up to 85 percent of your benefits are subject to federal income tax.

- Joint Filers: For married couples, a combined income between $32,000 and $44,000 means up to 50 percent of benefits are taxable. Any combined income above $44,000 pushes you into the 85 percent tier.

Crucially, these specific tax thresholds have never been adjusted for inflation since they were enacted decades ago. Consequently, every time you receive a cost-of-living adjustment, your rising income automatically edges you closer to—or further into—these taxable brackets. Effective tax planning through strategies like Roth IRA conversions or utilizing Qualified Charitable Distributions (QCDs) becomes essential to preserving your wealth.

“Taxes will be the single biggest factor that separates people who run out of money from those who don’t.” — Ed Slott, CPA and Retirement Tax Expert

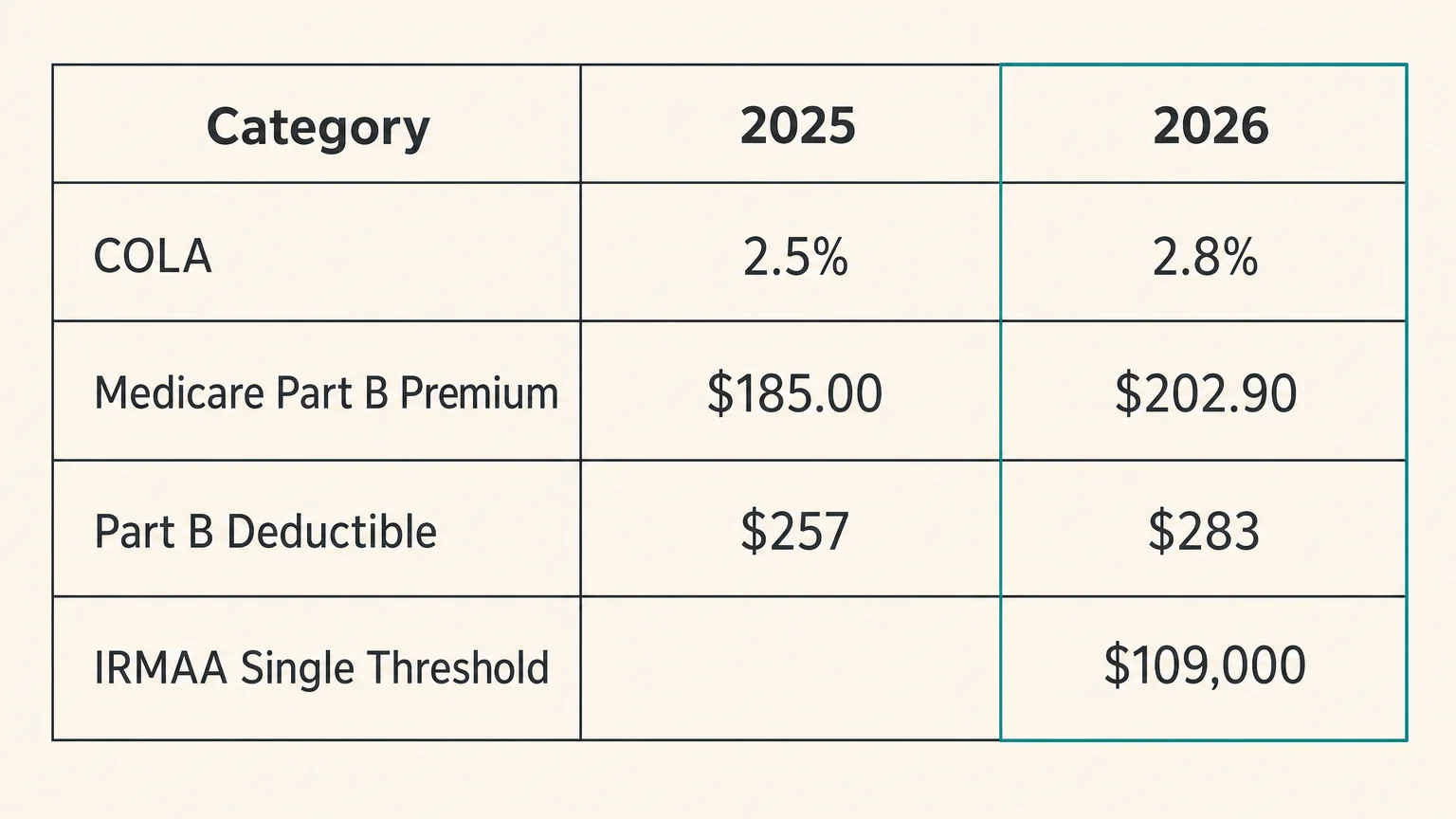

At a Glance: 2025 vs. 2026 Benefit Changes

To help you visualize how your financial landscape has shifted over the past year, review the comparison table below detailing the most critical changes to your retirement variables.

| Retirement Metric | 2025 Value | 2026 Value |

|---|---|---|

| Cost-of-Living Adjustment (COLA) | 2.5% | 2.8% |

| Medicare Part B Premium (Standard) | $185.00 | $202.90 |

| Medicare Part B Deductible | $257.00 | $283.00 |

| Earnings Limit (Under FRA) | $23,400 | $24,480 |

| Earnings Limit (Year of FRA) | $62,160 | $65,160 |

| Max Taxable Wage Base | $176,100 | $184,500 |

What Can Go Wrong: Avoiding Common Benefit Traps

Retirement planning is unforgiving of mistakes. Failing to account for how different government systems interact can cost you thousands of dollars. Be highly cautious regarding these three common scenarios:

1. Triggering an IRMAA Surcharge Accidentally

Many retirees decide to sell their primary residence, liquidate large stock portfolios, or convert Traditional IRA funds to a Roth IRA without considering the downstream effects. Because IRMAA uses a two-year lookback period, a massive income spike in 2024 will suddenly cause your Medicare Part B premiums to skyrocket in 2026. If your income increase was tied to a specific life-changing event (such as a divorce or work stoppage), you can file Form SSA-44 to request a premium reduction.

2. Fearing the Earnings Limit Penalty

Some seniors drastically reduce their working hours to avoid surpassing the $24,480 limit, operating under the false assumption that withheld benefits vanish forever. If you enjoy working or need the income, do not let the earnings test deter you; the money is ultimately credited back to your permanent base benefit once you cross your Full Retirement Age.

3. Assuming the Hold Harmless Rule Will Protect You

The “hold harmless” provision generally prevents your Medicare Part B premium increase from lowering your net Social Security check from one year to the next. However, this rule does not apply to everyone. If you pay Medicare premiums directly because you have not yet claimed Social Security, or if you are subject to high-income IRMAA surcharges, the hold harmless rule provides zero protection against steep premium hikes.

When to Consult a Professional

While educating yourself is a powerful first step, certain retirement scenarios demand the oversight of a Certified Financial Planner or licensed tax professional. Seek specialized advice if you face any of the following circumstances:

- You are executing large Roth conversions. Staggering your conversions over several years can help you minimize immediate tax liabilities and avoid triggering catastrophic Medicare surcharges.

- You are navigating spousal or survivor benefits. The rules governing widow(er) benefits and divorced spouse benefits are incredibly complex. Maximizing these unique payouts requires detailed timeline modeling.

- You plan to work extensively while claiming early. If you anticipate earning a high salary while taking benefits before age 67, a professional can calculate exactly how much of your check will be withheld and whether delaying your claim makes more mathematical sense.

Frequently Asked Questions

Will my net Social Security check decrease next year?

For the vast majority of retirees, your net check will not decrease. The Social Security COLA typically outpaces the dollar amount of Medicare Part B increases. Additionally, the hold harmless provision prevents standard premium increases from reducing your net monthly payment below the previous year’s amount. However, high-income earners triggering new IRMAA tiers could see a smaller net check.

How do I view my official 2026 benefit amount?

The fastest and most secure method is to log into your personal my Social Security account at SSA.gov. The administration updates these portals with official COLA notices in late November or early December of the preceding year.

Does part-time work or side-hustle income count toward the earnings limit?

Yes. Any W-2 wages or net self-employment income counts directly toward the $24,480 earnings limit. However, passive income sources—such as pensions, annuities, investment dividends, and capital gains—do not count toward the Social Security earnings test.

What is the maximum benefit for 2026?

The absolute maximum Social Security benefit for an individual claiming at age 70 in 2026 is $5,181 per month. Achieving this rare payout requires earning at or above the maximum taxable wage base for 35 complete years.

By taking a proactive approach to your finances, you can stop guessing and start planning. Review your projected expenses, monitor your tax brackets carefully, and utilize official government portals to confirm your numbers. Navigating the changes to Social Security and Medicare requires diligence, but maintaining a clear view of your net income will secure the comfortable retirement you have earned.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.