You spend decades saving, investing, and planning for the day you can finally stop working. You meticulously calculate your expected Social Security benefits, review your 401(k) balance, and map out a realistic monthly budget. Yet, even the most diligent planners frequently encounter financial blind spots once they actually leave the workforce.

A recent analysis reveals that a 65-year-old retiring in 2025 will need approximately $172,500 to cover healthcare and medical expenses throughout their retirement. For a married couple, that figure doubles to $345,000—and shockingly, this estimate does not even include the costs of long-term care. When you build your retirement roadmap, relying strictly on your current living expenses simply will not work. Your spending habits change, tax rules shift, and government programs like Medicare come with a complex web of premiums and deductibles.

To protect your nest egg and enjoy the comfortable retirement you worked so hard to achieve, you must anticipate the expenses that drain retiree budgets. By recognizing these financial hurdles ahead of time, you can build a more resilient financial plan. Let us explore the most common hidden costs that catch retirees off guard—and how you can prepare for them today.

1. The Surprising Price Tag of Medicare

Many Americans assume that turning 65 means waving goodbye to expensive health insurance premiums. While Medicare provides an incredible safety net, it is far from free. Original Medicare consists of Part A (hospital insurance) and Part B (medical insurance), and while Part A is generally premium-free for most retirees, Part B carries a mandatory monthly cost.

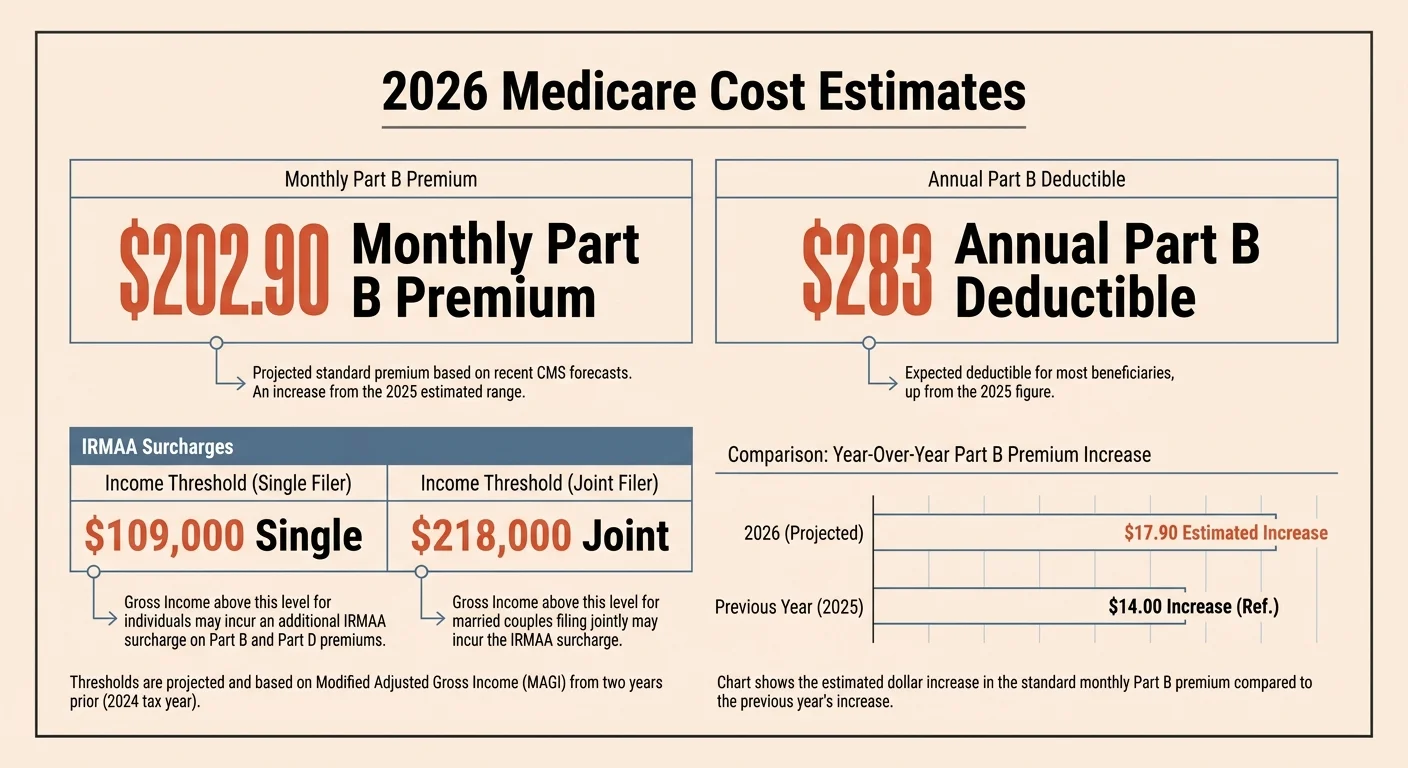

In 2026, the standard Medicare Part B premium is $202.90 per month, reflecting a $17.90 increase from the previous year. You must also cover the Part B annual deductible, which climbed to $283 for 2026. These baseline costs immediately eat into your monthly Social Security check, since the government automatically deducts Part B premiums from your benefits.

However, the real surprise comes if you saved diligently and generate a higher income in retirement. The government imposes an Income-Related Monthly Adjustment Amount (IRMAA) on retirees with higher incomes. For 2026, if you file taxes as a single person and your Modified Adjusted Gross Income (MAGI) exceeds $109,000, or if you file jointly with a MAGI over $218,000, you face significant surcharges on both your Part B and Part D (prescription drug) premiums. Because the government looks at your tax return from two years prior to determine your IRMAA status, a one-time financial windfall—such as selling a property or executing a large Roth conversion—can temporarily trigger these hefty surcharges.

2. Out-of-Pocket Healthcare Creep

Medicare covers a substantial portion of your medical needs, but it deliberately leaves wide gaps in coverage. Original Medicare generally does not pay for routine dental care, vision exams, glasses, or hearing aids. As you age, your reliance on these specific services typically increases, leaving you fully responsible for the bills unless you purchase supplemental coverage.

Retirees generally address these gaps in one of two ways, both of which add to your monthly overhead:

- Medicare Supplement (Medigap) Policies: These plans cover the deductibles, copayments, and coinsurance that Original Medicare leaves behind. However, Medigap requires a separate monthly premium paid to a private insurance company, which increases as you age.

- Medicare Advantage (Part C) Plans: These plans often bundle Part A, Part B, and prescription drug coverage, sometimes throwing in dental and vision perks. While they often boast low or zero-dollar premiums, they require you to navigate restrictive provider networks and pay copayments out of pocket as you use services.

Furthermore, prescription drug costs under Medicare Part D change annually. Formularies shift, and the medications you rely on today might cost significantly more next year. You must aggressively manage your healthcare budget and shop your Part D or Advantage plans during the Annual Enrollment Period every fall.

3. The Threat of Long-Term Care

If there is one expense with the power to devastate a carefully constructed retirement portfolio, it is long-term care. According to recent federal estimates, most Americans over the age of 65 will eventually need some form of daily assistance with bathing, dressing, or eating. Original Medicare does not cover custodial long-term care; it only pays for short-term skilled nursing facility stays following a qualifying hospital admission.

The private pay rates for long-term care have skyrocketed due to inflation and severe labor shortages in the healthcare industry. A recent national survey highlights the staggering 2025-2026 costs of this care:

- In-Home Care: Hiring a home health aide costs a median of $80,080 annually.

- Assisted Living Facilities: The median cost for a private room in an assisted living community now runs roughly $74,400 per year.

- Nursing Homes: A semi-private room in a skilled nursing facility commands a median daily rate of $315, translating to nearly $115,000 annually. A private room pushes the cost to almost $130,000 per year.

Without long-term care insurance, a hybrid life insurance policy, or substantial personal assets earmarked for healthcare, you risk depleting your life savings. Medicaid will step in to cover nursing home costs, but only after you spend down your assets to near-poverty levels.

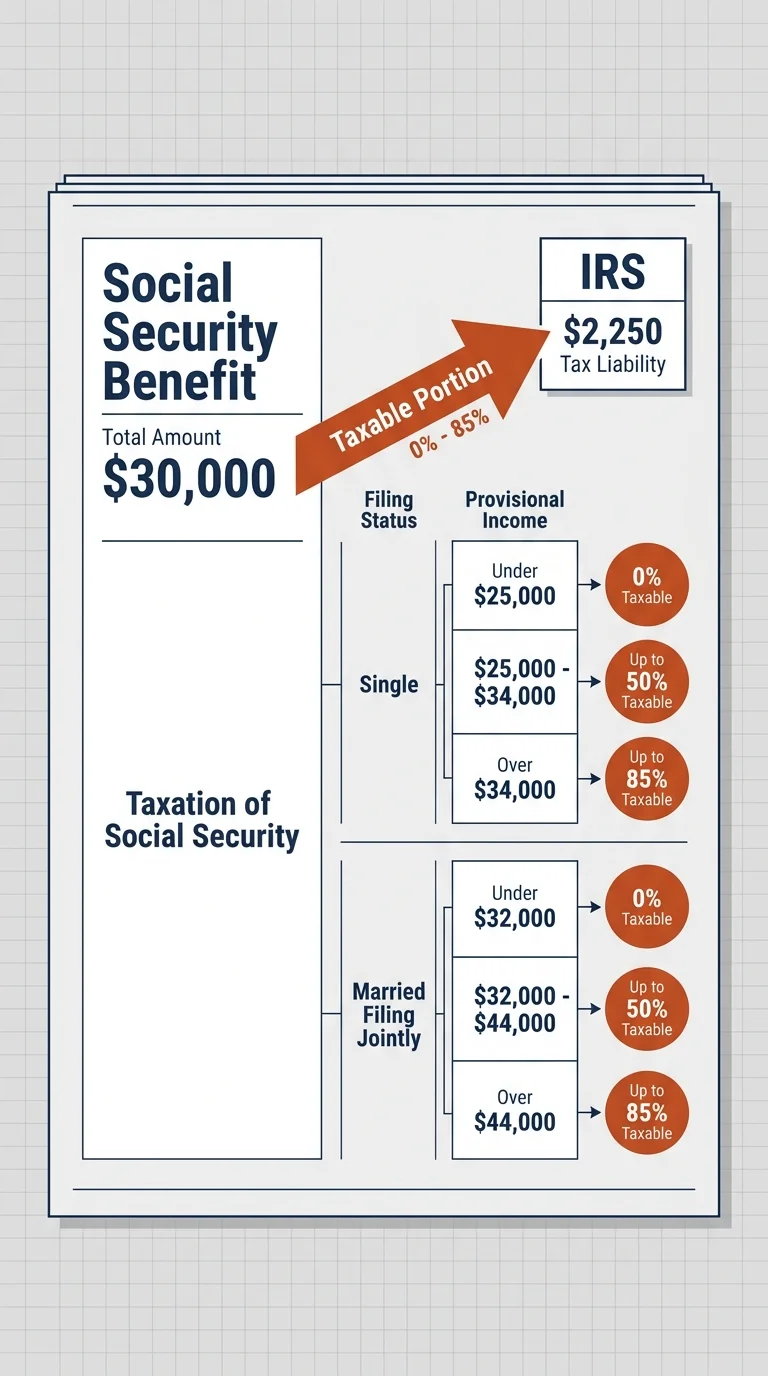

4. The Tax Trap on Social Security Benefits

Many new retirees believe their Social Security checks are tax-free. Unfortunately, depending on your other sources of income, the Internal Revenue Service may tax up to 85% of your benefits.

The IRS uses a specific formula called “Combined Income” to determine the taxability of your benefits. You calculate your Combined Income by adding your Adjusted Gross Income (AGI), any nontaxable interest (such as municipal bond yields), and exactly half of your yearly Social Security benefits. The thresholds for this tax trap have remained completely unchanged since they were established in the 1980s and 1990s, meaning inflation naturally pushes more retirees into taxable territory every single year.

For the 2026 tax year, the rules dictate:

- Single Filers: If your Combined Income falls between $25,000 and $34,000, up to 50% of your benefits may be taxable. If your Combined Income exceeds $34,000, up to 85% of your benefits may face taxation.

- Married Filing Jointly: If your Combined Income lands between $32,000 and $44,000, up to 50% of your benefits may be taxed. Above $44,000, up to 85% of your benefits become taxable.

Withdrawing funds from a traditional IRA or 401(k) directly increases your AGI, which drives up your Combined Income and subjects more of your Social Security to taxation. This creates a painful “tax torpedo” effect that requires careful withdrawal sequencing to avoid.

5. Home Maintenance and “Aging in Place” Renovations

Paying off your mortgage before retirement removes a massive burden from your monthly budget, but it does not make your home free to live in. Property taxes inevitably rise, homeowners insurance premiums surge—especially in areas prone to natural disasters—and the physical structure of your house requires ongoing capital.

Financial professionals generally advise budgeting 1% to 2% of your home’s total value annually for routine maintenance. If your home is worth $400,000, you should expect to spend $4,000 to $8,000 per year fixing leaky roofs, replacing aging HVAC systems, and maintaining your landscaping.

More significantly, if you plan to stay in your current home for the rest of your life, you will likely need to modify the space for accessibility. Aging in place often requires widening doorways to accommodate walkers or wheelchairs, replacing step-in bathtubs with zero-entry showers, installing reinforced grab bars, and potentially adding a chairlift if you live in a multi-story home. These accessibility renovations routinely cost tens of thousands of dollars and represent a major, highly predictable expense that rarely makes it into a retirement spreadsheet.

6. Inflation’s Slow-Motion Erosion

When you calculate your retirement needs, the math looks simple in year one. But retirement is not a single event; it is a phase of life that can easily last 25 to 30 years. Over three decades, the silent thief of inflation relentlessly erodes your purchasing power.

“Inflation is the greatest enemy of the long-term investor.” — John Bogle, Vanguard Founder

Even a modest inflation rate of 3% will cut the purchasing power of your money in half over a 24-year period. If your comfortable retirement lifestyle costs $60,000 a year today, you will need approximately $120,000 a year to buy the exact same goods and services two decades from now. While Social Security provides an annual Cost-of-Living Adjustment (COLA)—which delivered a 2.8% increase for 2026—your personal investment portfolio must shoulder the rest of the burden.

Retirees who pivot completely away from the stock market and hide their cash in low-yield bonds or savings accounts often run out of money. You must maintain enough exposure to growth-oriented assets to outpace inflation, ensuring your portfolio continues generating real returns deep into your golden years.

7. The “Bank of Mom and Dad” Stays Open

We naturally want to give our children a leg up in the world, but supporting adult kids financially has become a severe threat to American retirement security. With high housing costs and inflation squeezing younger generations, parents routinely step in to bridge the gap.

A comprehensive 2025 survey found that exactly half of all American parents with adult children provide them with regular financial support. The average monthly assistance reached $1,474—equating to nearly $18,000 annually. Parents direct this money toward their children’s groceries, cell phone bills, rent, and even vacations.

Alarmingly, working parents who support their grown kids contribute more than twice as much money to their children each month as they do to their own retirement accounts. Nearly half of supporting parents admit they have sacrificed their personal financial security to keep their kids afloat.

“The best thing you can do for your kids is secure your own retirement.” — Suze Orman, Personal Finance Expert

If you drain your nest egg to pay your child’s rent today, you may eventually become a financial burden on them tomorrow when you cannot afford your own medical care. Setting firm financial boundaries with adult children is one of the most critical steps in defending your retirement.

Pitfalls to Watch For

Awareness of these hidden costs is just the first step. To keep your financial plan on track, remain vigilant against these common retirement mistakes:

- Ignoring Required Minimum Distributions (RMDs): Once you reach age 73 (or 75, depending on your birth year), the IRS forces you to pull money out of your tax-deferred accounts. Forgetting to take these distributions results in severe penalties, and the forced income can push you into higher tax brackets and trigger Medicare IRMAA surcharges.

- Failing to Diversify by Tax Type: If 100% of your savings sits in a traditional 401(k), the IRS taxes every single dollar you withdraw. By building up Roth accounts and taxable brokerage accounts before you retire, you grant yourself the flexibility to pull income from tax-free sources during years when your tax rate spikes.

- Overlooking the Senior Standard Deduction: The tax code does offer some relief for retirees. In 2026, the standard deduction for a single filer age 65 or older is $18,150 (combining a base of $16,100 and a $2,050 age-based bonus). A married couple filing jointly where both spouses are 65 or older enjoys a massive $35,500 standard deduction. You must ensure you actually claim the age-related bonuses when you file your return.

Getting Expert Help

Navigating the transition from accumulating wealth to distributing wealth is inherently difficult. You only get one chance to retire right. Consider consulting a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) in the following scenarios:

- Five Years Before Retirement: A professional can run Monte Carlo simulations to stress-test your portfolio against market crashes, inflation spikes, and long-term care events.

- When Claiming Social Security: Coordinating spousal benefits and timing your claim to minimize the “tax torpedo” requires highly specific tax modeling.

- When Exploring Roth Conversions: Moving money from traditional accounts to Roth accounts requires paying taxes upfront, but it reduces your future RMDs. An expert can help you fill up your current tax bracket without tipping over into higher marginal rates or triggering IRMAA.

Frequently Asked Questions

Are Social Security benefits taxed at the state level?

While the federal government taxes benefits based on your Combined Income, state laws vary dramatically. Most states do not tax Social Security at all. However, a handful of states still levy taxes on benefits, though many offer exemptions based on your age and income. Always verify the current tax laws in your specific state before finalizing your retirement budget.

Can I buy long-term care insurance after I turn 65?

Yes, you can purchase a policy after age 65, but the premiums become substantially more expensive the longer you wait. Additionally, insurance companies require medical underwriting; if you already have serious pre-existing health conditions, the carrier may deny your application entirely. Financial planners generally recommend shopping for coverage in your late 50s or early 60s.

How can I avoid the Medicare IRMAA surcharge?

Because IRMAA is based on your MAGI from two years prior, avoiding it requires proactive tax management. Strategies include completing Roth conversions before you file for Medicare, utilizing Qualified Charitable Distributions (QCDs) to satisfy your RMDs without increasing your AGI, and drawing income from tax-free sources like Roth IRAs or Health Savings Accounts (HSAs) to keep your taxable income below the surcharge thresholds.

Retirement should be a season of freedom and fulfillment, not a period defined by financial anxiety. By facing these hidden costs head-on, adjusting your savings targets, and establishing a tax-efficient withdrawal strategy, you empower yourself to navigate your golden years with complete confidence. Take the time today to review your current plan and ensure your budget accounts for the realities of aging, taxes, and inflation.

Disclaimer: This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: April 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.