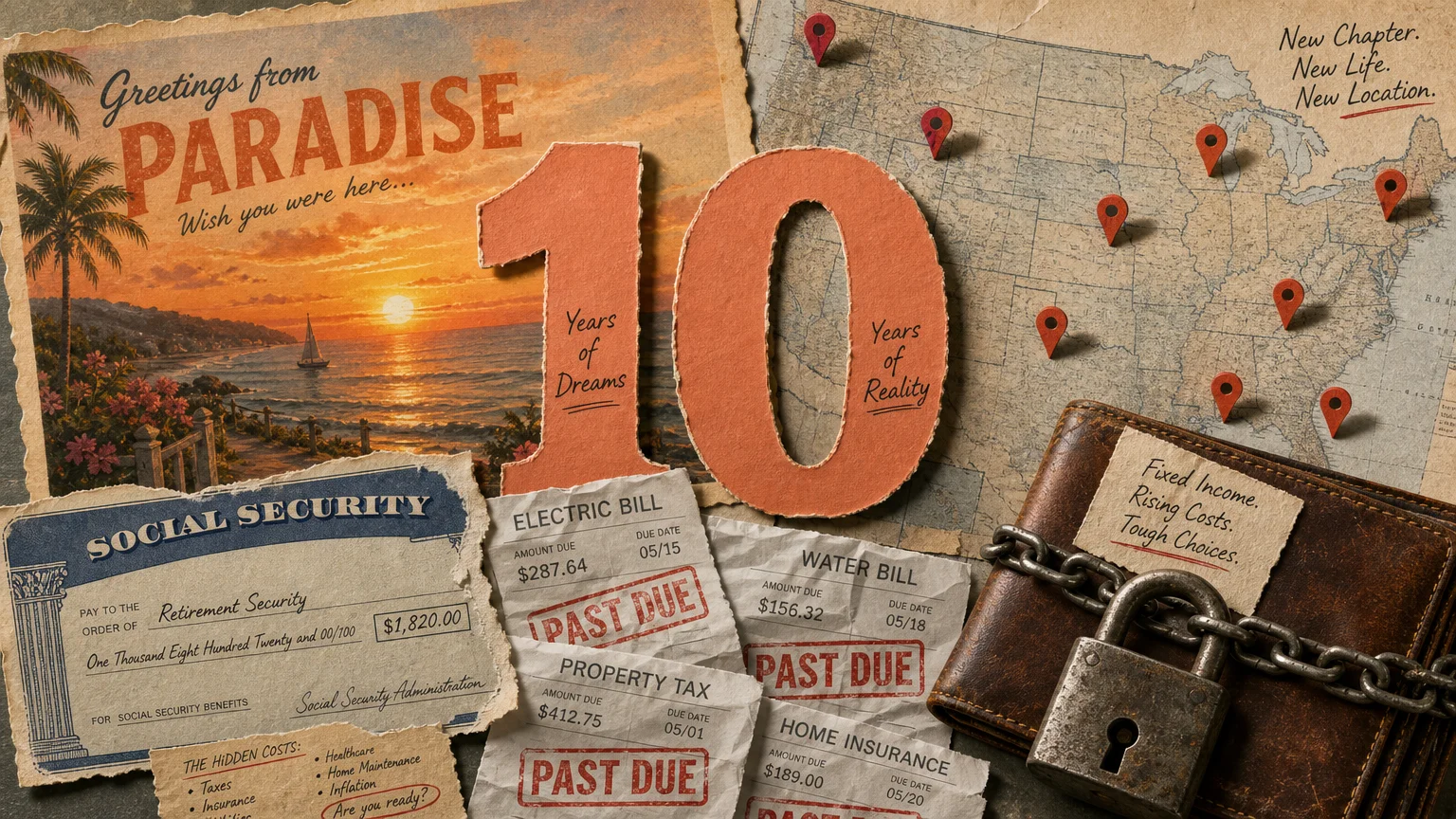

Arizona remains one of the most popular retirement destinations in the United States, offering a compelling mix of tax advantages, top-tier healthcare, and endless sunshine. You might be dreaming of days spent on the golf course or hiking desert trails, but the reality of living in the Grand Canyon State goes beyond the travel brochures. Retiring in Arizona requires navigating complex water shortages, surprising health risks, and rising insurance premiums. Before you pack your bags and commit to a desert lifestyle, you need a complete picture of the financial and physical realities. This guide breaks down the true advantages and hidden challenges of an Arizona retirement so you can decide if it is the right move for your future.

Pro #1: A Highly Favorable Tax Environment for Retirees

When you transition from earning a paycheck to living off your savings, protecting your income from state taxes becomes a top priority. Arizona has positioned itself as one of the most tax-friendly states for older adults, starting with its treatment of government benefits. According to the Social Security Administration and the state’s revenue department, Arizona does not tax Social Security benefits. Every dollar you receive from the federal program stays in your bank account, which provides a massive relief for retirees relying on those monthly deposits to cover basic living expenses.

Beyond Social Security, Arizona transitioned to a flat individual income tax rate of 2.5 percent, which remains fully implemented for the 2025 and 2026 tax years. Prior to this change, high-income retirees taking large distributions from their traditional IRAs or 401(k)s could face progressive brackets that penalized heavy withdrawals. Today, whether you withdraw $40,000 or $140,000 from your retirement accounts, you pay the exact same low percentage. This flat rate makes strategic tax planning—such as executing large Roth IRA conversions—much more predictable and affordable.

Property taxes in Arizona are equally appealing. The state boasts an average effective property tax rate of roughly 0.43 to 0.48 percent of a home’s assessed value, ranking among the lowest in the nation. If you purchase a $500,000 home in the Phoenix metropolitan area, you can generally expect your annual property tax bill to hover around $2,100 to $2,400. Compared to the crushing property tax burdens in states like Illinois, Texas, or New Jersey, the savings you experience in Arizona can easily fund your annual travel budget or cover your Medicare premiums.

Pro #2: Robust, Master-Planned Senior Communities

Arizona effectively invented the modern active adult community when Sun City opened its doors in 1960. Since then, the state has perfected the concept of the master-planned senior lifestyle. Communities like Sun City West, Green Valley, and the numerous Robson Resort Communities are practically self-sustaining municipalities designed entirely around the physical and social needs of older adults.

Living in one of these communities means having immediate access to recreation centers, multiple golf courses, pickleball courts, woodworking shops, and hundreds of special interest clubs. The infrastructure is famously golf-cart friendly; you can drive your cart to the grocery store, the pharmacy, and your doctor’s office without ever merging onto a major highway. This level of accessibility becomes incredibly valuable if you eventually decide to stop driving a full-sized vehicle.

However, you must account for the financial structure of these neighborhoods. Most 55-plus communities require mandatory Homeowners Association (HOA) dues, and many enforce a hefty capital improvement fee when you purchase the home. This one-time buy-in fee can cost several thousand dollars and goes toward maintaining the community’s extensive amenities. While the lifestyle is unparalleled, you should review the HOA’s reserve study before buying to ensure they have adequate funds for future repairs without levying sudden special assessments against residents.

Pro #3: Access to Premier Healthcare Facilities

As you age, proximity to world-class healthcare transitions from a luxury to an absolute necessity. Arizona delivers on this front, serving as a regional hub for medical excellence. The Mayo Clinic campus in Phoenix and Scottsdale consistently ranks among the top hospitals in the country, drawing patients globally for complex cancer treatments, cardiology, and neurology.

In addition to the Mayo Clinic, the Banner Health system operates an extensive network of hospitals and specialized clinics throughout the state, ensuring that even residents in the outer suburbs have access to high-quality emergency and routine care. For retirees relying on Medicare, Maricopa County (home to Phoenix) offers one of the most competitive Medicare Advantage markets in the United States. You will find a wide array of plans featuring zero-dollar monthly premiums, robust prescription drug coverage, and additional perks like dental and vision benefits. You can verify the specific plans available in your desired zip code by using the plan finder tool on Medicare.gov.

The abundance of healthcare options provides peace of mind, but you must be proactive about establishing care. Because of the state’s rapidly growing senior population, finding a primary care physician accepting new Medicare patients can take time. It is highly recommended that you begin your search for local doctors months before your actual move date.

Pro #4: An Active, Outdoor Winter Lifestyle

If you have spent decades shoveling driveways and enduring freezing wind chills, Arizona’s winter climate will feel like an absolute revelation. From November through April, the weather is spectacularly pleasant, with high temperatures consistently resting in the upper 60s and 70s. The state averages over 300 days of sunshine annually, creating an environment that actively encourages physical fitness and outdoor socialization.

This prolonged stretch of perfect weather allows retirees to maintain highly active lifestyles, which is a key component of long-term health and mobility. You can spend your January mornings hiking the trails of the Superstition Mountains, biking along the Scottsdale Greenbelt, or playing tennis outdoors. The psychological benefit of waking up to bright blue skies nearly every day cannot be overstated; many retirees report a significant boost in their mood and energy levels simply by escaping the gloomy, overcast winters of the Midwest or Pacific Northwest.

Con #1: The Hidden Threat of Valley Fever

While the sunshine is a major draw, the desert environment harbors a unique and increasingly prevalent health risk known as Valley Fever (coccidioidomycosis). This respiratory infection is caused by a microscopic fungus that lives in the desert soil. When the dirt is disturbed by construction, farming, or the state’s famous monsoon dust storms (haboobs), the fungal spores become airborne. If inhaled, they can settle in the lungs and cause severe illness.

Recent data underscores the severity of this issue. According to the Arizona Department of Health Services, there were over 14,700 reported cases of Valley Fever in 2024, representing a massive 34 percent increase over the recent five-year average. Older adults and individuals with weakened immune systems are at a higher risk of developing severe complications, which can include chronic pneumonia or the fungus spreading to the bones and brain.

The symptoms closely mimic the flu or COVID-19—fatigue, a persistent cough, fever, and chest pain. Because Valley Fever is relatively unknown outside the Southwest, out-of-state visitors and new residents often face misdiagnosis. If you move to Arizona and develop a lingering respiratory issue, you must specifically ask your physician to order a blood test for Valley Fever, as standard antibiotics will not cure a fungal infection.

Con #2: Water Shortages and Rising Utility Costs

The long-term sustainability of the desert lifestyle is heavily dependent on water, and the region is facing unprecedented challenges. The Colorado River, which supplies a significant portion of the water for the Central Arizona Project (CAP), has been locked in a decades-long drought exacerbated by climate change. As a result, the federal government has declared ongoing Tier 1 shortage conditions extending through 2025 and 2026, which forces mandatory reductions in the amount of water Arizona can draw from the river.

While municipal water supplies for residential homes are prioritized and currently secure, the financial and aesthetic impacts of these shortages are already trickling down to homeowners. To conserve resources, many cities are aggressively restricting the planting of new grass, and HOAs are spending millions to remove lush golf course roughs and communal lawns, replacing them with desert landscaping (xeriscaping). If you dream of a retirement home with a sprawling, green backyard, you will find those properties increasingly rare and expensive to water.

Furthermore, the cost of water and electricity continues to climb. During the blistering summer months, keeping your home at a safe, comfortable temperature requires running your air conditioning around the clock. It is not uncommon for a moderately sized home to generate monthly electricity bills exceeding $350 to $450 from June through September. You must build these inflated seasonal utility costs into your fixed-income budget.

Con #3: Surging Homeowners Insurance Premiums

Arizona was once considered a haven from the massive property insurance spikes seen in hurricane-prone Florida or wildfire-ravaged California. Unfortunately, that reality has shifted dramatically. Driven by inflation in construction materials, labor shortages, and an increase in local climate risks, homeowners insurance rates in Arizona have surged significantly.

Recent industry reports indicate that Arizona home insurance rates have jumped roughly 70 percent over the past six years, marking one of the highest cumulative increases in the nation. The state’s unique weather patterns—including intense monsoon microbursts, damaging hail, and an expanding wildfire season in the northern and eastern regions—have forced insurers to aggressively adjust their pricing models.

When planning your housing budget, do not rely on outdated cost estimates. A policy that might have cost $900 annually a few years ago could easily approach $1,600 or more today depending on your home’s age and roof condition. To protect yourself, you should work with an independent insurance broker to shop your policy annually, and heavily consider raising your deductible to keep your monthly premiums manageable.

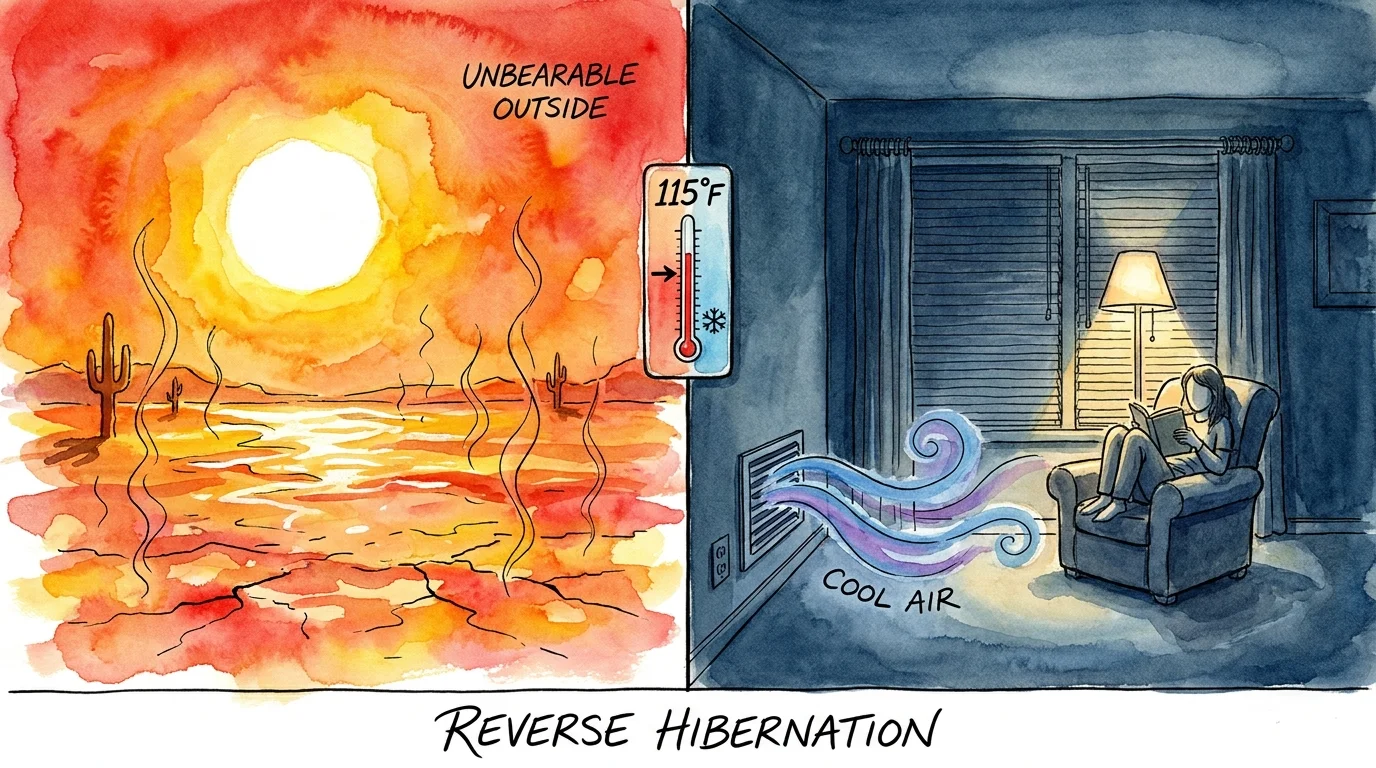

Con #4: The Extreme Summer Heat and Reverse Hibernation

Everyone knows the desert is hot, but experiencing an Arizona summer is a completely different reality than visiting for a long weekend. From late May through September, daytime temperatures routinely exceed 105 degrees, and during intense heat waves, the thermometer can breach 115 degrees. More punishing than the daily highs are the nighttime lows; in July and August, the temperature may not drop below 90 degrees, offering no relief to the environment or the power grid.

This extreme heat forces retirees into a lifestyle pattern known as “reverse hibernation.” Just as residents of Minnesota stay indoors all winter to avoid the snow, Arizona residents spend their summers sheltering in the air conditioning. If you want to walk your dog, play golf, or go for a run, you must complete these activities before 8:00 AM, after which the sun becomes dangerous.

This intense heat takes a toll on both your body and your property. Car batteries often die after just two years, exterior paint fades rapidly, and your home’s HVAC system experiences massive strain. Before purchasing a home, you must hire an inspector to scrutinize the age and condition of the air conditioning unit. Replacing a failed AC system can easily cost between $10,000 and $15,000—a devastating unexpected expense for a retiree on a fixed income.

Con #5: The “Snowbird” Squeeze on Local Infrastructure

Arizona’s perfect winter weather brings a massive seasonal influx of part-time residents, affectionately known as “snowbirds.” From November through April, the populations of cities like Scottsdale, Mesa, and Tucson swell dramatically as retirees from the Midwest, the Pacific Northwest, and Canada migrate south to escape the cold.

While this migration fuels the local economy, it creates a severe squeeze on the region’s infrastructure. Traffic on major arteries like the Loop 101 and I-10 becomes highly congested, and your daily commute can easily double. Wait times at popular restaurants grow frustratingly long, and securing a prime morning tee time at the local golf course becomes a fiercely competitive endeavor.

Most importantly, the sudden population spike places immense pressure on the healthcare system. Routine doctor appointments, specialist visits, and non-emergency surgeries must be booked months in advance during the winter season. If you are a full-time resident, you must learn to schedule your annual checkups and elective procedures during the quieter summer months to avoid the winter rush.

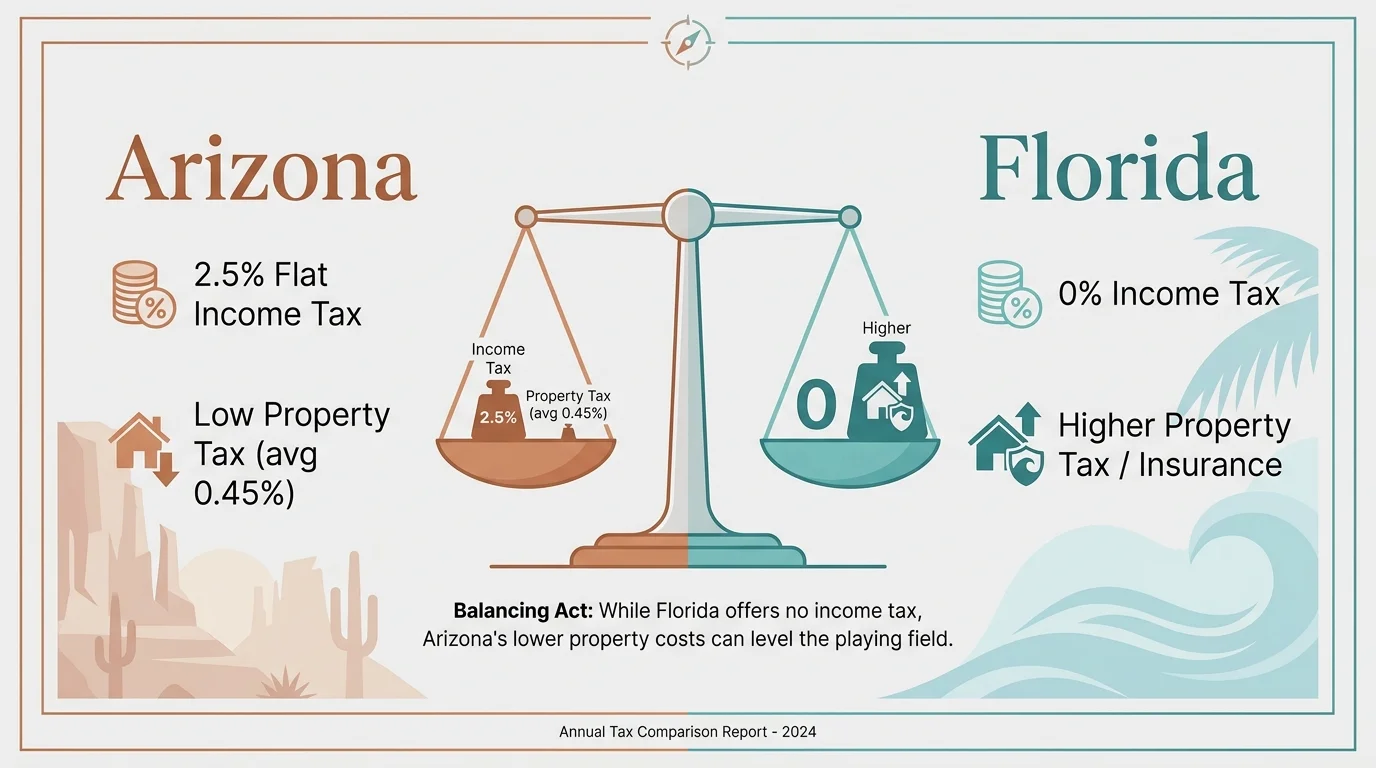

Comparing the Tax Burden: Arizona vs. Florida

Retirees frequently debate between moving to the desert Southwest or the Sunshine State. While both offer favorable climates for older adults, their tax structures differ significantly. Here is a high-level look at how the financial environments compare for retirees:

| Tax Category | Arizona | Florida |

|---|---|---|

| State Income Tax | 2.5% flat rate for all brackets | 0% (No state income tax) |

| Social Security Tax | 0% (Fully exempt) | 0% (Fully exempt) |

| Average Property Tax Rate | ~0.43% to 0.48% | ~0.80% to 0.91% |

| Estate / Inheritance Tax | None | None |

| Sales Tax (Combined Avg) | ~8.5% (Varies by county/city) | ~7.0% (Varies by county/city) |

While Florida boasts zero state income tax, Arizona offsets its modest 2.5 percent income tax with significantly lower property taxes. Your personal financial profile—specifically your ratio of investment income to real estate value—will ultimately determine which state offers the better mathematical advantage.

“When you retire, your housing costs are often your biggest expense. Choosing a state with favorable property taxes can stretch your nest egg significantly and provide a powerful buffer against inflation.” — Jean Chatzky, Personal Finance Expert

Pitfalls to Watch For When Moving to Arizona

If you have decided the pros outweigh the cons, you must navigate the transition carefully. Avoid these common missteps when establishing your new life in the desert:

- Ignoring the HVAC Age: Never buy an Arizona home without knowing the exact age and maintenance history of the air conditioning units. If the system is over 10 years old, negotiate a replacement credit from the seller or walk away. You do not want to endure a system failure during a 110-degree July afternoon.

- Underestimating HOA Restrictions: Many master-planned communities have strict rules regarding exterior paint colors, street parking, and the type of landscaping allowed in your yard. Read the bylaws thoroughly to ensure the community’s culture matches your lifestyle expectations.

- Failing to Hydrate: The desert climate is exceptionally dry, meaning your sweat evaporates instantly. You can become severely dehydrated without ever feeling sweaty. You must develop a habit of carrying water with you everywhere, even for short errands.

- Overlooking Vehicle Maintenance: The extreme heat destroys rubber and drains batteries. You will need to replace your windshield wipers, tires, and car battery much more frequently than you did in cooler climates.

Getting Expert Help

Relocating across the country in retirement is a major logistical and financial undertaking. To ensure a smooth transition, consider enlisting the following professionals:

- Fiduciary Financial Planner: Before you sell your current home, consult a fee-only fiduciary to run a comprehensive tax projection. They can help you calculate exactly how Arizona’s 2.5 percent flat tax will impact your specific combination of pension, 401(k), and investment income.

- Senior Real Estate Specialist (SRES): Hire a local realtor who holds an SRES designation. They possess specialized knowledge regarding 55-plus communities, HOA fee structures, and single-level floor plans tailored for aging in place.

- Independent Insurance Broker: With property insurance rates rising sharply across the state, an independent broker can shop your policy across dozens of carriers to find the most competitive rate for your specific neighborhood and home type.

Frequently Asked Questions

Does Arizona tax out-of-state pensions?

Yes, Arizona generally taxes out-of-state private pensions and traditional IRA withdrawals at the flat 2.5 percent rate. However, military pensions and certain federal civil service pensions are exempt from state income tax. Always consult with a tax professional regarding your specific pension type.

Is it expensive to run air conditioning in Arizona?

Yes, cooling costs are a significant portion of a retiree’s budget. Depending on the size, age, and energy efficiency of your home, summer electricity bills can easily range from $250 to over $450 per month. Many residents utilize budget-billing programs offered by local utility companies to smooth out these seasonal spikes into predictable monthly payments.

Do I need a water softener in Arizona?

Arizona is notorious for having extremely “hard” water, meaning it contains high levels of calcium and magnesium. While perfectly safe to drink, hard water leaves stubborn mineral scale on shower doors, damages plumbing fixtures over time, and dries out your skin and hair. Most homeowners find installing a whole-house water softener to be a necessary investment.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources such as the Internal Revenue Service (IRS) and state agencies before making financial decisions.