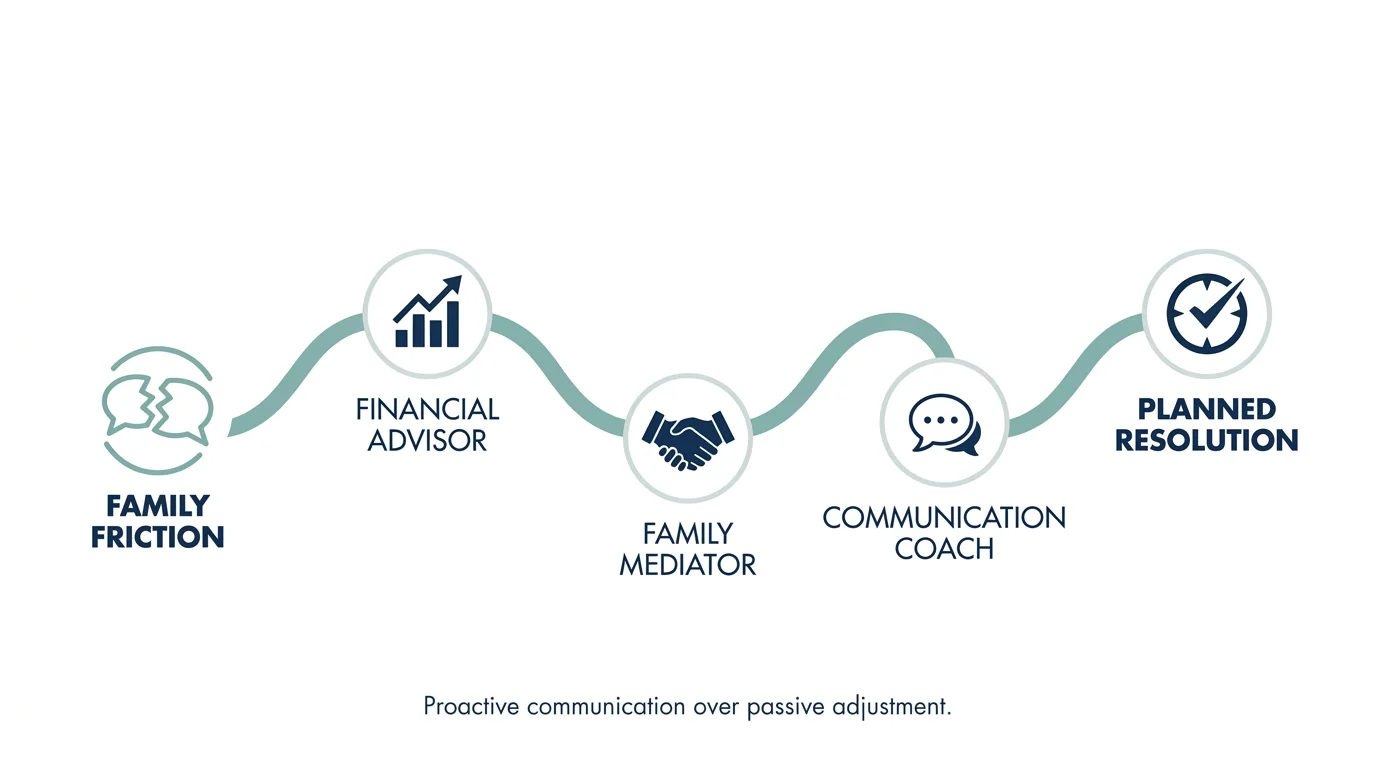

Retirement instantly rewires your family dynamics, shifting everything from your Tuesday morning routines with your spouse to your financial boundaries with adult children. You spent decades operating under one set of rules, and leaving the workforce requires drafting an entirely new social contract with those you love. This transition forces you to confront unspoken expectations about grandparenting duties, caregiving, housing, and estate planning. Navigating these profound changes successfully requires proactive communication rather than passive adjustment. By understanding the eight specific ways retirement alters your closest relationships, you can protect your hard-earned financial security, sidestep common emotional pitfalls, and establish healthy boundaries that bring your family closer together during your next chapter.

1. Redefining Spousal Proximity and Daily Roles

When you and your spouse were both working, your relationship thrived in the margins—evenings, weekends, and scheduled vacations. Retirement suddenly throws you together for 16 waking hours a day. This abrupt shift from passing ships to constant companions often creates friction over seemingly minor issues like grocery shopping routines, television volumes, or what time the dog gets walked.

You must renegotiate your division of labor. The spouse who historically managed the household might resent the newly retired partner interfering in established routines. Conversely, the newly retired partner might feel lost and unintentionally micromanage household affairs to regain a sense of purpose and control. Treat this transition as an opportunity to build a shared “Retirement Policy Statement.” Outline your shared goals, but more importantly, schedule independent time. Maintain separate hobbies, run errands individually, and respect each other’s need for solitude. Healthy marriages rely on physical and emotional breathing room, even when your calendars are entirely free.

2. Shifting Financial Dynamics With Adult Children

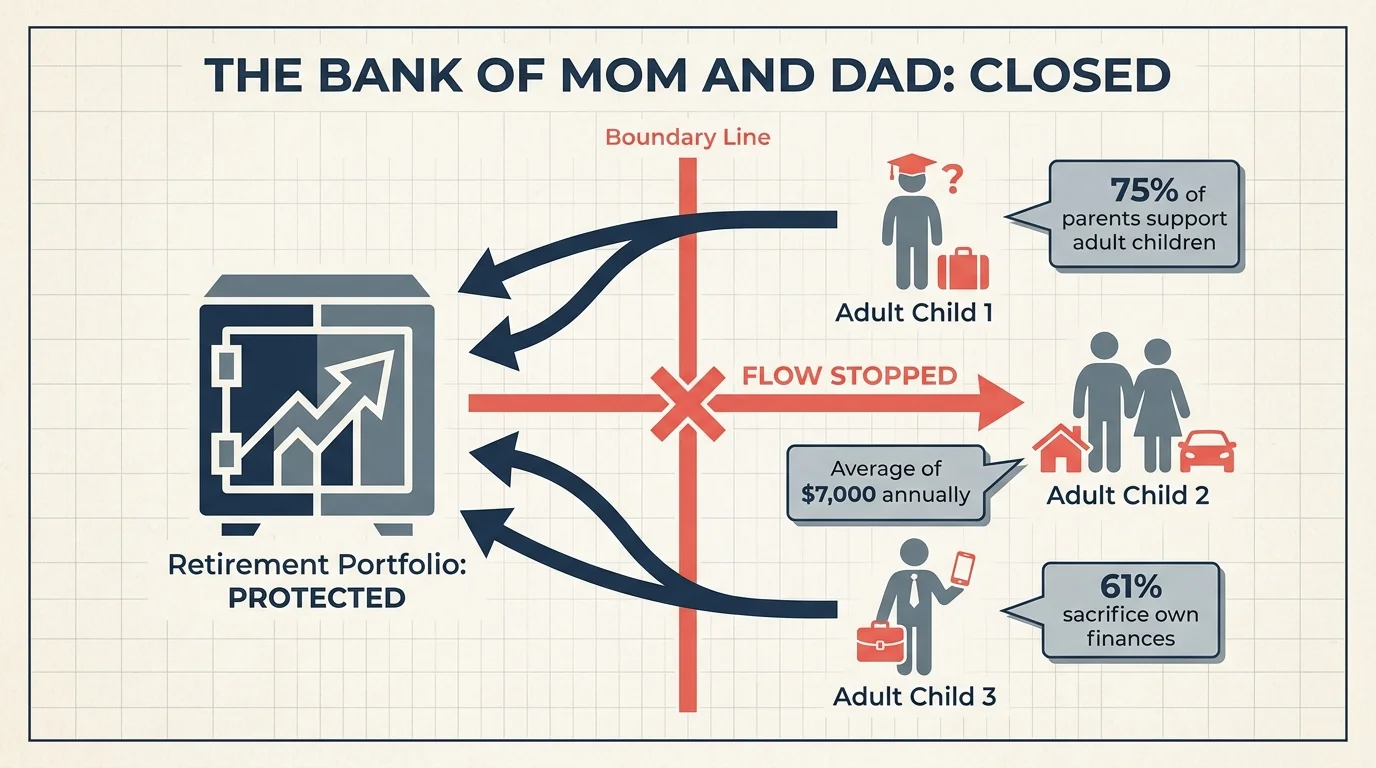

Leaving the workforce forces a hard pivot from asset accumulation to asset preservation. However, your adult children may still view you as their financial safety net. Continuing to act as the “Bank of Mom and Dad” severely jeopardizes your portfolio’s longevity and alters the fundamental respect in your relationship.

Recent data underscores this challenge: 75% of parents financially support at least one adult child, providing an average of $7,000 annually. Startlingly, 61% of parents sacrifice their own finances to help their adult children. You must establish firm financial boundaries immediately. You cannot secure a loan for your retirement, but your children have decades to earn income and finance their own goals.

“You cannot give your children what you do not have. Prioritizing your own retirement security is the greatest financial gift you can give your family.” — Suze Orman, Personal Finance Expert

Communicate your new fixed-income reality clearly and firmly. Transitioning your adult children to total financial independence is a required step for your own financial survival.

3. The Grandparenting Expectation Gap

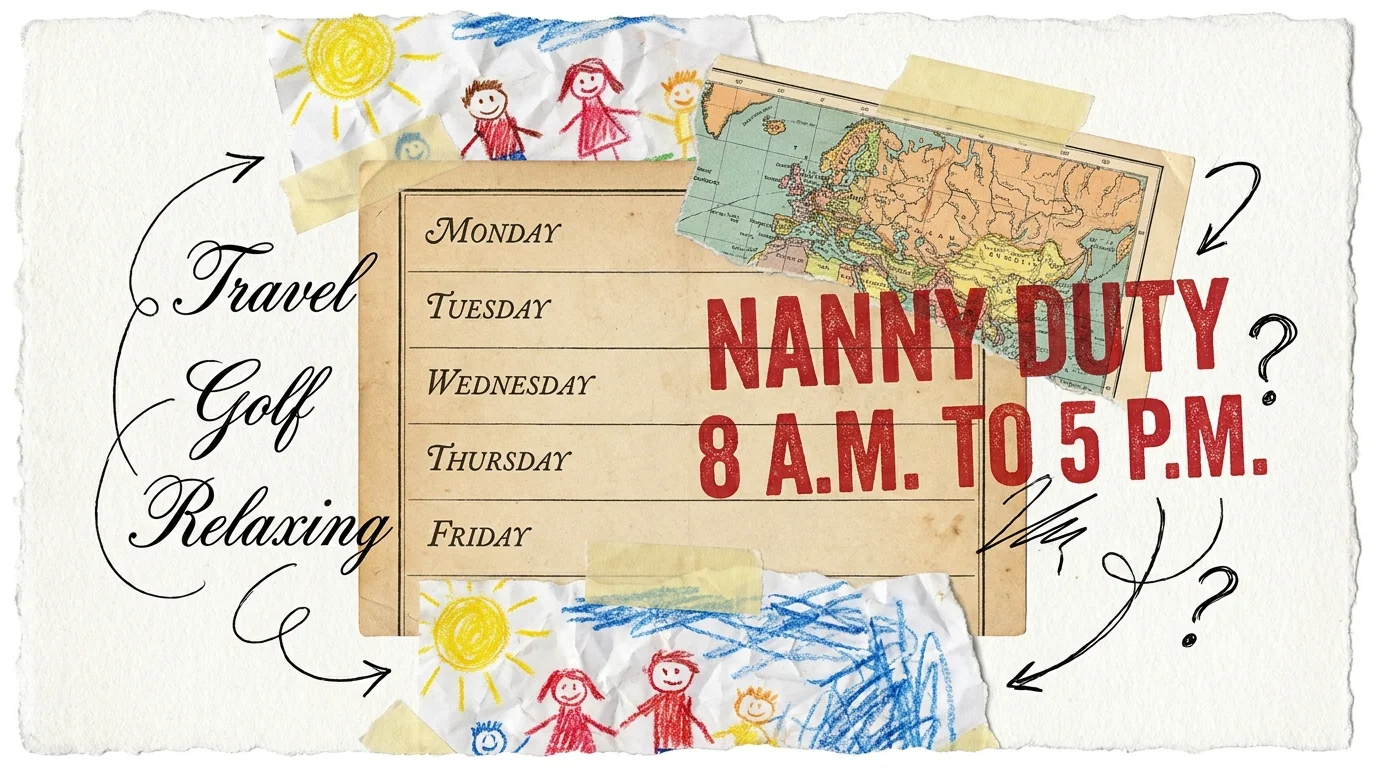

Your adult children might view your retirement as the perfect solution to their rising childcare costs. While spending more time with your grandchildren sounds delightful on paper, serving as a full-time, unpaid nanny quickly leads to physical burnout and emotional resentment.

The expectation gap occurs when your vision of retirement—traveling, volunteering, and relaxing—collides with your children’s assumption that you are available every weekday from 8 a.m. to 5 p.m. Before your retirement date arrives, initiate a candid conversation about your availability. Set specific, structured parameters around when and how often you will watch the grandchildren. Offering to host sleepovers on alternate weekends or handling Tuesday school pickups provides meaningful help without monopolizing your hard-earned freedom. Establishing these boundaries early prevents the guilt trips that inevitably follow when you have to say “no” later.

4. Sibling Relationships and the Caregiving Divide

Retirement rarely happens in a vacuum; it often coincides with your own parents reaching an age where they require increased physical and administrative assistance. If your siblings are still working full-time, they may default to the assumption that your retirement gives you limitless free time to manage your aging parents’ medical appointments, financial affairs, and daily care.

This dynamic strains sibling relationships rapidly. Caregiving carries significant physical, emotional, and financial costs that can derail your early retirement years. You must proactively define caregiving roles with your brothers and sisters. If you handle the day-to-day physical care and transportation, perhaps your working siblings can contribute more financially to hiring a home health aide or taking over the complex administrative tasks of dealing with Medicare and eldercare billing. Demand an equitable distribution of responsibility so that resentment does not permanently fracture your sibling bonds.

5. The Threat of “Gray Divorce”

The romanticized vision of walking hand-in-hand down the beach in retirement masks a sobering reality: divorce rates among older Americans remain stubbornly high. Recent demographic data shows that nearly 40% of divorcing persons in the U.S. are aged 50 and older.

Splitting your household in your sixties or seventies devastates your retirement plan. You lose the economies of scale that come with shared housing, you must aggressively divide your retirement assets, and your claiming strategies become significantly more complicated. Protecting your marriage requires deliberate effort and ongoing investment. Recognize that the person you married thirty years ago has evolved, and so have you. Invest in marriage counseling if communication breaks down, find shared passions that excite both of you, and actively work to transition from busy co-parents and focused co-workers into genuine companions again.

6. The Rise of Multigenerational Living

Economic pressures, soaring housing costs, and caregiving needs are driving a massive resurgence in multigenerational households. In 2024, multigenerational homes accounted for 17% of all home purchases, representing an all-time high for this demographic. Today, roughly 18% of the U.S. population lives in a household with multiple adult generations under one roof.

Moving in with your adult children—or having them move back in with you—changes the family power dynamic instantly. You move from the role of the undisputed head of household to a co-habitant, which requires a heavy dose of humility and compromise. Success in this living arrangement demands rigid boundaries. You need clear agreements on financial contributions, privacy expectations, discipline rules for the grandchildren, and shared chores. Draft a formal written agreement before moving the first box to ensure everyone understands the operational rules of the house.

7. Navigating Social Independence and Friendships

Your broader social network undergoes a massive stress test when you retire. You instantly lose daily contact with workplace colleagues, and your friendships with people who are still working face serious scheduling friction. Your working friends cannot meet for a Tuesday morning golf game, and they may harbor subtle jealousy regarding your new lifestyle.

This shift places immense pressure on your immediate family to fill your socialization void. Do not rely solely on your spouse or your adult children for your emotional fulfillment and daily entertainment. Build a new, independent social circle of fellow retirees. Join local clubs, volunteer at community organizations, or participate in group fitness classes to ensure your social calendar remains full without overburdening your family members. Maintaining your own social independence makes you a more interesting spouse and a less demanding parent.

8. The Legacy and Estate Planning Conversation

Retirement forces you to confront your mortality, making it the ideal time to finalize your estate plan. Many retirees avoid talking to their children about inheritances, wills, and end-of-life care because the topics feel morbid. This silence breeds severe anxiety and sets the stage for bitter family disputes after you are gone.

“Leave the children enough so that they can do anything, but not enough that they can do nothing.” — Warren Buffett, Investor and Philanthropist

Hold a formal family meeting to outline your wishes. Explain where your important documents are located, introduce your children to your financial advisor, and clarify the reasoning behind your estate decisions. If you are leaving unequal inheritances, explain why now while you still can. Transparency prevents surprises and ensures your family focuses on grieving and supporting one another rather than fighting over assets in probate court.

Pitfalls to Watch For: Common Relationship Traps

Navigating these relational shifts requires vigilance. Avoid these common traps that can quickly fracture family bonds during your transition:

- Making unilateral financial decisions: Taking a massive withdrawal from your savings to pay off an adult child’s debt without consulting your spouse breeds deep, lasting resentment. Every major financial decision must be a joint agreement.

- Overpromising your time: Saying “yes” to every volunteer request, community board, and family babysitting duty leaves you exhausted and defeats the primary purpose of retiring. Protect your calendar fiercely.

- Hiding health issues: Concealing physical limitations or early cognitive decline from your family prevents them from providing necessary support and planning for your future care needs.

- Delaying estate planning: Dying intestate or leaving outdated beneficiary designations on your retirement accounts guarantees legal headaches and infighting for your heirs. Keep your paperwork immaculate and up to date.

Getting Expert Help for Family Transitions

You do not have to navigate these complex family dynamics in isolation. Different professionals can assist you depending on the specific challenge your family faces:

- Certified Financial Planners (CFP®): Use a fiduciary planner to act as the “bad guy” when setting financial boundaries with adult children. You can simply deflect the pressure by saying, “My advisor says my financial plan cannot afford this distribution right now.”

- Elder Care Attorneys: Consult a specialized lawyer to draft your durable powers of attorney, healthcare directives, and living trusts. They ensure your assets are protected from unnecessary taxation and your healthcare wishes are legally binding.

- Family Therapists: Seek out a licensed counselor if you and your spouse are struggling to adapt to constant proximity, or if caregiving responsibilities are tearing your sibling relationships apart. A neutral third party can facilitate conversations that are too emotionally charged to handle alone.

Frequently Asked Questions

Does my Social Security COLA keep up with my family’s financial needs?

Historically, the Cost-of-Living Adjustment (COLA) struggles to keep pace with retirees’ actual experienced inflation, particularly regarding healthcare. For example, the Social Security COLA for 2026 was 2.8%, but the standard Medicare Part B premium simultaneously rose to $202.90. Because these baseline costs consume so much of your income increase, you must budget conservatively rather than relying on COLA to cover rising family expenses or to fund financial support for your adult children.

How do I talk to my adult children about cutting off financial support?

Schedule a dedicated time to talk—do not bring it up in the heat of an argument or when they ask for money. Be highly transparent about your transition to a fixed income and present a phased timeline for reducing support. Say, “I want to ensure I never become a financial burden to you later in life, which means I need to prioritize my retirement savings and step back from covering these expenses starting next month.”

Should I pay my family members for caregiving?

If an adult child or sibling provides substantial daily care that prevents them from working or heavily impacts their income, formalizing a personal care agreement is often a wise decision. This compensates them fairly for their labor, prevents resentment among other siblings who are not providing daily help, and can help you strategically and legally spend down assets if you plan to apply for Medicaid long-term care benefits in the future.

Retirement is a profound life transition that tests the resilience of your entire family network. By anticipating these eight relational shifts, you can proactively build the boundaries and communication habits necessary for a peaceful, fulfilling retirement. Treat your family relationships with the same careful planning, routine maintenance, and attention to detail that you give your investment portfolio.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.