According to the Employee Benefit Research Institute (EBRI), while average household spending drops modestly at the beginning of retirement, a large percentage of new retirees actually experience a massive, unexpected spending spike [1.16]. You spend decades meticulously stashing money into 401(k)s and IRAs, calculating target numbers, and dreaming of the day you hand in your keys. Yet, the first 365 days of retired life bring a barrage of financial and emotional surprises that standard retirement calculators simply cannot predict.

The transition from full-time earner to full-time retiree shifts your entire paradigm. Your daily schedule, tax situation, healthcare expenses, and even your personal identity go through a profound transformation. Navigating this shift requires more than just a healthy portfolio; it demands a strategic roadmap tailored to the realities of modern retirement.

1. The Initial “Honeymoon Phase” Fades Faster Than Expected

When you first leave the workforce, the sudden absence of morning commutes, endless meetings, and overflowing inboxes feels euphoric. Psychologists often refer to these first few months as the retirement honeymoon phase. You sleep in, tackle long-delayed home projects, and take a celebratory trip to mark the occasion.

However, around the six-month mark—sometimes referred to as the “100-Day Wall”—the novelty of perpetual weekends wears off. Without the built-in purpose and social interaction of a career, many retirees face a jarring sense of aimlessness and decision fatigue. This sudden void forces you to actively construct a new daily rhythm. Building a successful retirement means replacing the structure your employer used to provide with self-directed goals. Whether you join a local board, volunteer your expertise, consult part-time, or deeply engage in a complex hobby, you need a reason to get out of bed that goes beyond watching television or browsing the internet.

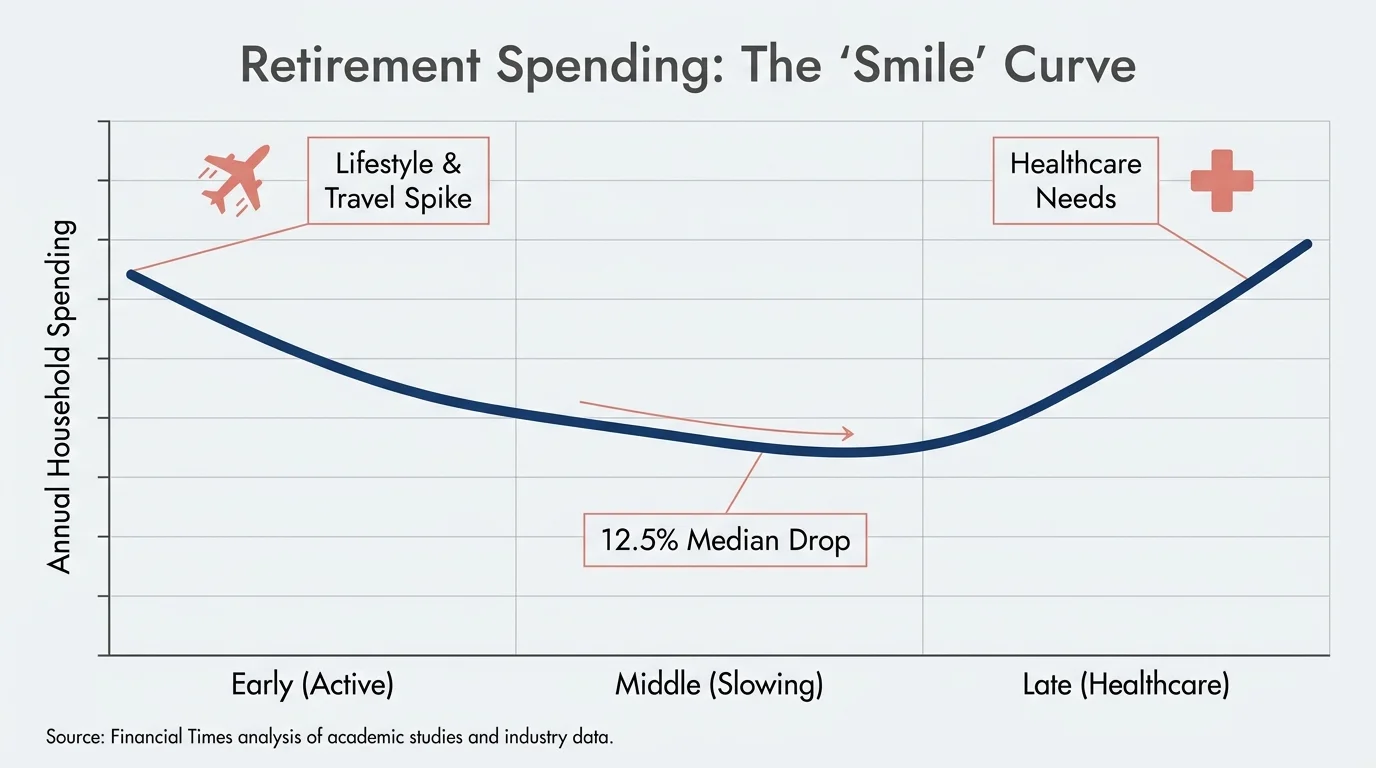

2. Your Spending Patterns Will Flip Upside Down

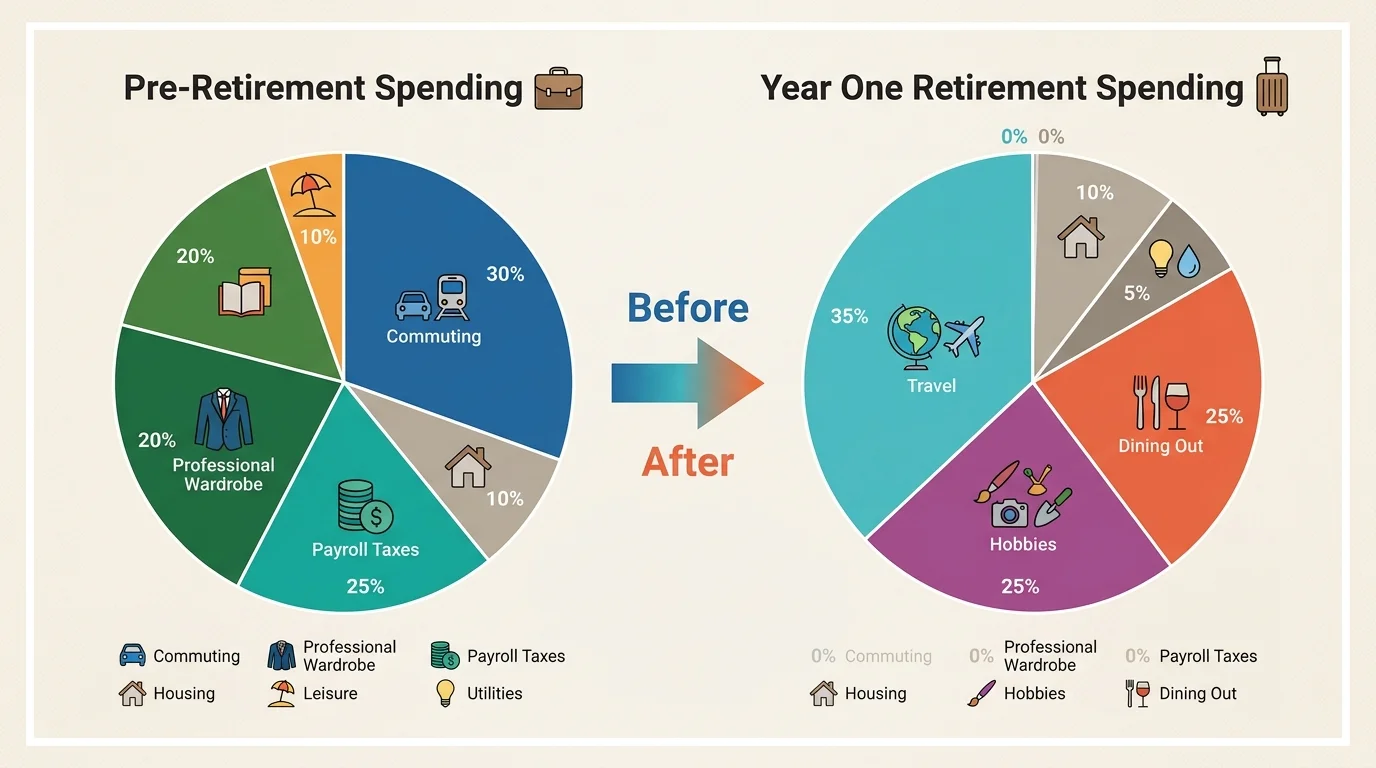

Financial planners often use a rule of thumb stating you will need 70 to 80 percent of your pre-retirement income to maintain your lifestyle. The reality of the first year is much more volatile. Research from EBRI indicates that median household spending drops by about 5.5 percent during the first two years of retirement, and by 12.5 percent by the third or fourth year. However, the categories where you spend your money will completely flip.

Commuting costs, professional wardrobe expenses, and payroll taxes vanish. In their place, your entertainment, travel, and lifestyle budgets often explode. Financial institutions like J.P. Morgan Asset Management refer to this phenomenon as the “spending smile”—spending is highest in the early, active years of retirement, dips during the middle years as you slow down, and spikes again at the end of life due to healthcare needs. Because every day is essentially a Saturday, the opportunities to spend money multiply. You go out for lunch more often, plan mid-week golf outings, and book spontaneous flights.

To avoid draining your portfolio prematurely, track your cash flow meticulously during these first twelve months. Establish a new monthly “paycheck” transferred from your investment accounts to your checking account, and stick to that budget rather than pulling funds on demand whenever an impulse arises.

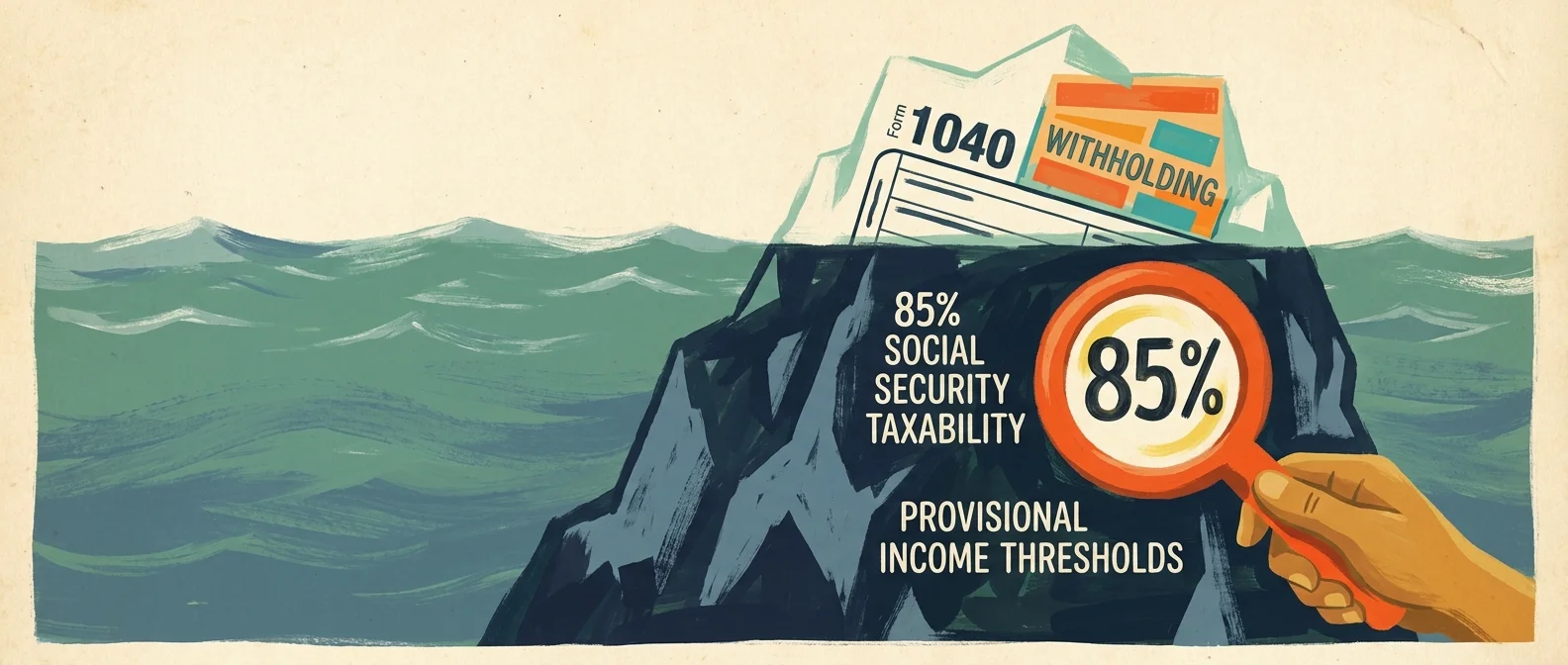

3. Taxes Become Your Biggest Unseen Expense

During your working years, your employer automatically withheld income taxes, making tax compliance relatively frictionless. In retirement, you become your own withholding agent, and the rules change drastically. Depending on your other income sources, up to 85 percent of your Social Security benefits can be subject to federal income tax if your provisional income exceeds certain thresholds.

Furthermore, the tax landscape shifts constantly. For the 2026 tax year, the Internal Revenue Service set the standard deduction at $32,200 for married couples filing jointly and $16,100 for single taxpayers. Retirees age 65 and older also qualify for an additional standard deduction amount. If you pull heavily from tax-deferred accounts like traditional IRAs or 401(k)s to fund a first-year kitchen remodel or an RV purchase, you could accidentally bump yourself into a higher marginal tax bracket.

Managing your withdrawals across taxable brokerage accounts, tax-deferred IRAs, and tax-free Roth accounts—a strategy known as tax-bracket management—can save you thousands. The first year of retirement is often an ideal time to consult a tax professional about strategic Roth conversions before Required Minimum Distributions (RMDs) force money out of your accounts later in life.

4. Medicare Costs Hide in Plain Sight

Many pre-retirees assume Medicare provides free, comprehensive healthcare. The first year of retirement quickly shatters this illusion. While Medicare Part A (hospital insurance) is generally premium-free if you paid Medicare taxes while working, Part B (medical insurance) and Part D (prescription drugs) carry distinct monthly costs.

For 2026, the standard Medicare Part B premium jumped to $202.90 per month, with an annual deductible of $283. However, if you had a strong earning year right before you retired, you face a hidden surcharge known as the Income-Related Monthly Adjustment Amount (IRMAA). The Social Security Administration bases your 2026 IRMAA on your Modified Adjusted Gross Income (MAGI) from 2024. If your 2024 MAGI exceeded $109,000 as a single filer or $218,000 as a married couple filing jointly, your Part B and Part D premiums will increase significantly. For high earners, IRMAA brackets can push monthly Part B premiums well over $400 or even $600 per person.

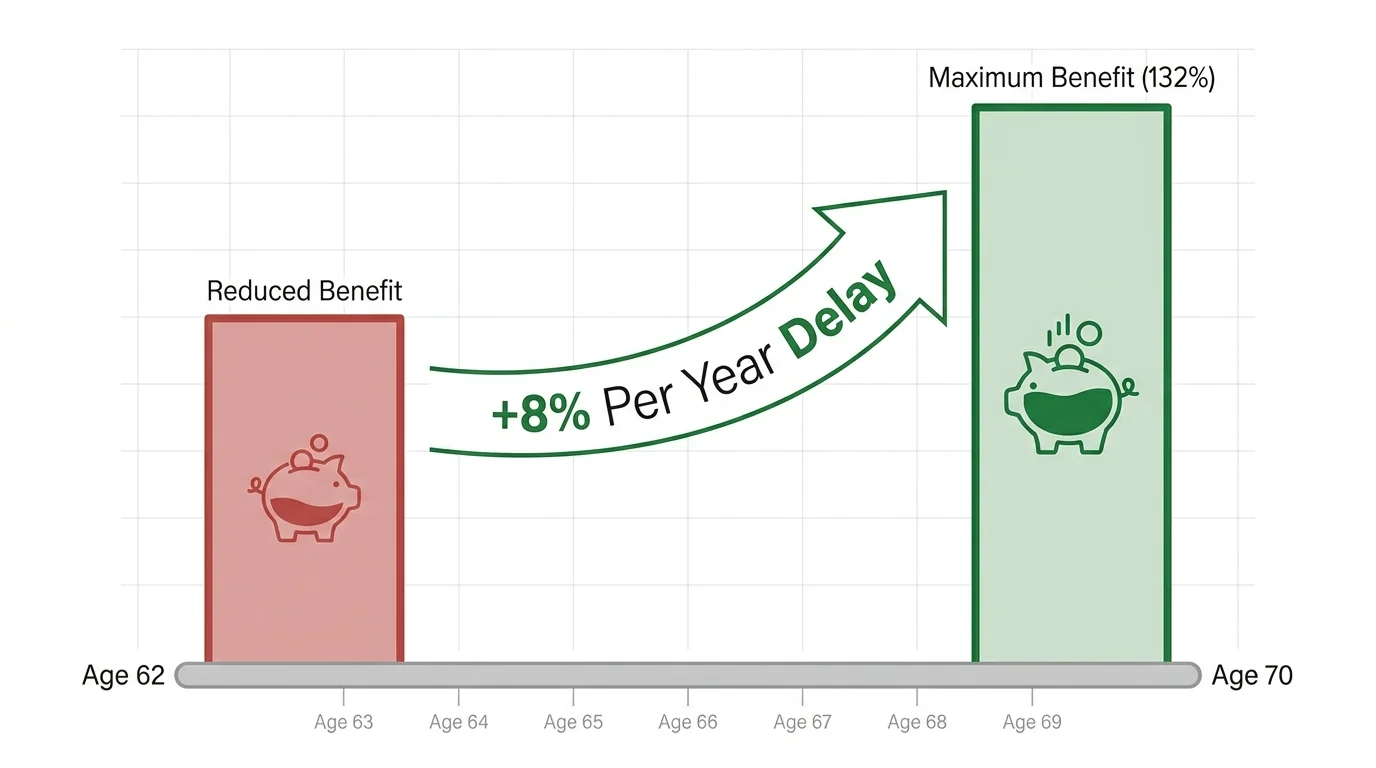

5. Social Security Timing Requires Mathematical Precision

Choosing when to claim Social Security ranks among the most critical financial decisions of your first year. While you can claim as early as age 62, doing so permanently reduces your monthly payout. Conversely, waiting until age 70 maximizes your guaranteed income, earning you delayed retirement credits.

The impact of inflation makes this decision even more vital. To help benefits keep pace with the economy, the government provides an annual Cost of Living Adjustment (COLA). For 2026, the Social Security Administration announced a 2.8 percent COLA, pushing the typical monthly retirement payment up to $2,071. Because COLAs apply as a percentage of your base benefit, securing a higher base amount by delaying your claim yields mathematically larger annual raises for the rest of your life. Evaluate your break-even point, family longevity, and immediate cash needs before filing your application.

6. You Have to Redefine Your Identity Without a Job Title

For decades, your professional title served as a shorthand for who you are and where you fit into the world. When you attend a social gathering during your first year of retirement and someone asks, “What do you do?”, hesitation often kicks in. You may find yourself answering with what you used to do.

Grieving the loss of your professional identity is a normal, healthy part of the transition. You are no longer the senior vice president, the lead floor manager, or the head nurse. You must proactively build an identity rooted in your character, your relationships, and your community contributions rather than your economic output. Give yourself grace during this psychological shift, and consciously practice a new “retirement elevator pitch” that focuses on your current passions—such as mentoring, traveling, or community advocacy—rather than your past employment.

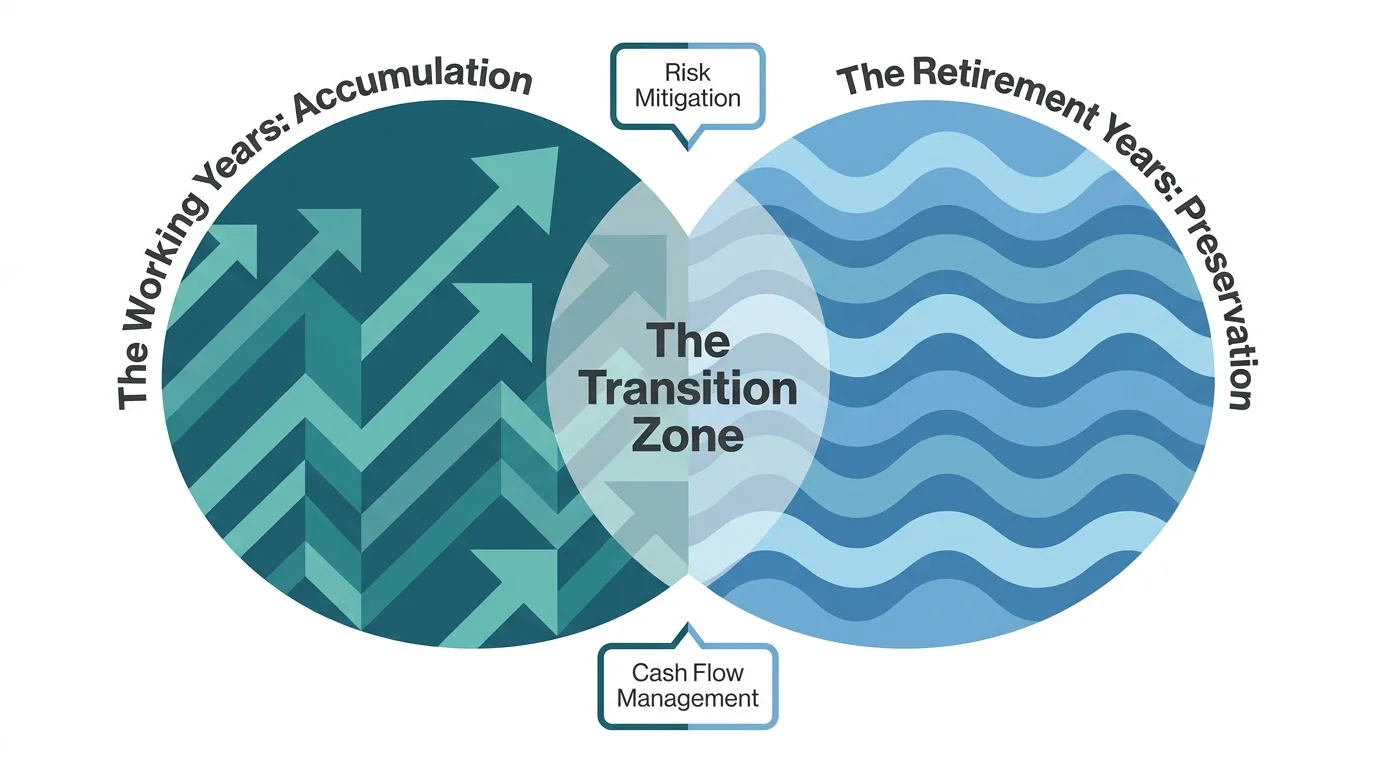

7. Your Investment Strategy Shifts from Accumulation to Preservation

During your working years, market volatility presented a buying opportunity. When stocks dropped, your bi-weekly 401(k) contributions simply bought more shares at a discount. In your first year of retirement, a market downturn becomes an immediate threat to your livelihood. This vulnerability is known as sequence of returns risk. If you withdraw living expenses from a shrinking portfolio early in retirement, you permanently reduce the capital available to generate future growth when the market eventually recovers.

This reality necessitates a fundamental shift in your investment approach. You must pivot from pure growth to a balanced strategy that prioritizes income generation and capital preservation.

“The first rule of an investment is don’t lose. And the second rule of an investment is don’t forget the first rule.” — Warren Buffett, Chairman of Berkshire Hathaway

To protect yourself, consider adopting a “bucket strategy.” Ensure you hold enough cash, short-term bonds, or certificates of deposit to cover one to three years of living expenses. This buffer allows you to leave your equity investments untouched during temporary market corrections, giving your stocks the time they need to rebound.

8. Marital and Social Dynamics Require Intentional Realignment

If you are married, the first year of retirement drastically alters your relationship dynamic. Going from seeing your spouse a few hours an evening to sharing the house 24 hours a day requires boundary setting. The sudden overlap in domestic space can lead to friction over household chores, daily schedules, and spending habits.

You will quickly discover that “we are retired” does not mean “we must do everything together.” Maintaining separate hobbies, individual friendships, and personal quiet time prevents resentment and preserves the health of your marriage. Open communication about expectations for this new phase is critical to avoiding the rising trend of “gray divorce.”

Socially, the built-in network of your workplace disappears. You no longer have breakroom chats or regular team lunches. You must put deliberate effort into making and keeping friends. Join community groups, attend local classes at a community college, and actively reach out to neighbors to build a new support system.

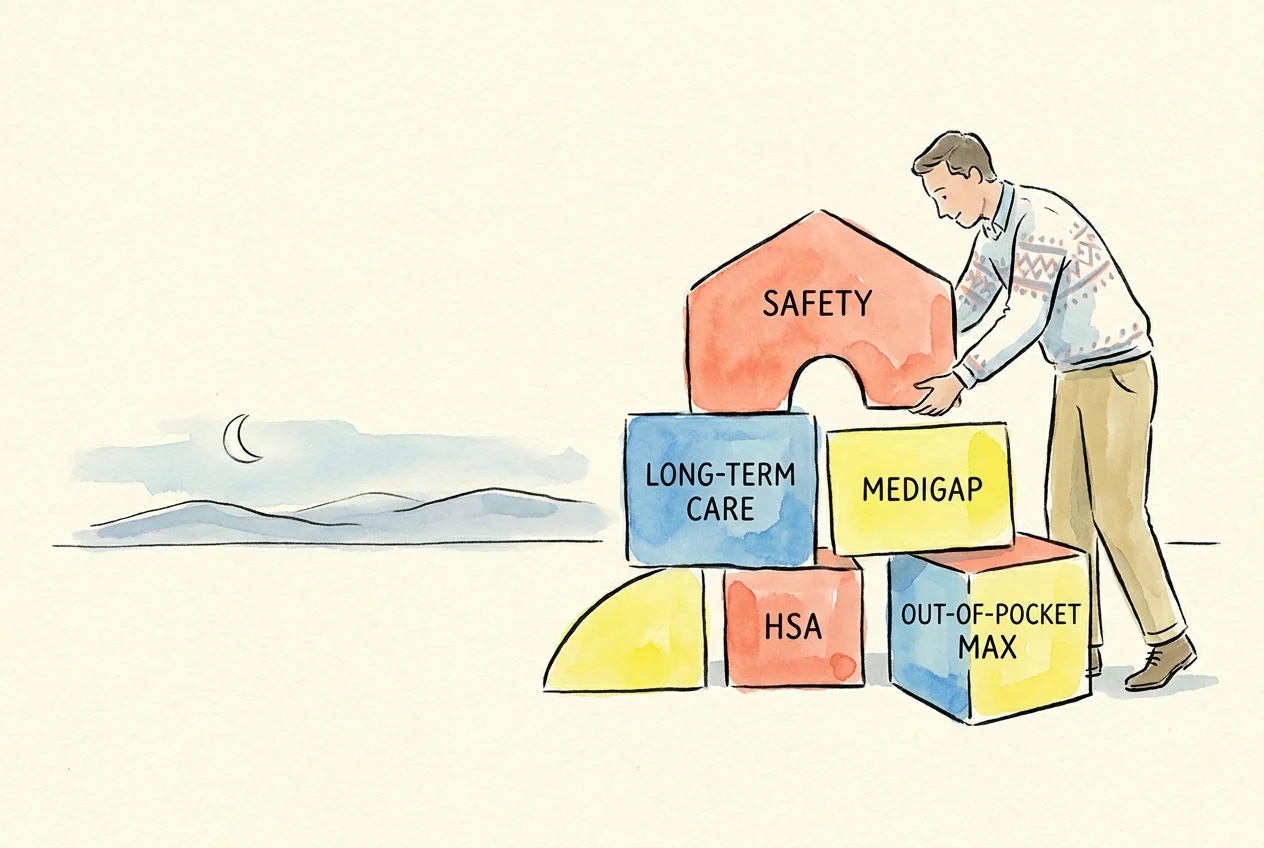

9. Healthcare Pre-Planning Becomes Non-Negotiable

Beyond basic Medicare premiums, out-of-pocket medical costs catch many new retirees off guard. Routine dental work, vision care, and hearing aids generally fall outside of standard Original Medicare coverage. You will need to evaluate Medicare Advantage (Part C) plans or Medicare Supplement (Medigap) policies—such as Plan G or Plan N—to bridge these coverage gaps.

Furthermore, the first year of retirement is the exact time to confront long-term care planning. Fidelity estimates that a typical 65-year-old couple will need approximately $300,000 to cover out-of-pocket healthcare costs throughout retirement, and that figure does not even include long-term care facilities. Medicare does not cover custodial care (help with activities of daily living like bathing and dressing). Whether you look into traditional long-term care insurance, hybrid life insurance policies, or self-funding strategies, putting a plan in writing now protects your family from making distressed financial decisions later.

10. The Need for Routine is Hardwired into Your Brain

Humans thrive on predictability and circadian rhythms. You spent 40 years waking up, eating lunch, and winding down at roughly the same time every day. Removing that structure completely can lead to poor sleep hygiene, skipped meals, and lethargy.

Establish a flexible but consistent retirement routine. Dedicate your mornings to physical health—walking, swimming, or stretching. Block out afternoons for mental engagement, whether that means reading, managing your portfolio, or volunteering. Reserve your evenings for relaxation and family time. Setting a schedule does not mean stifling your freedom; it means giving your days a framework so you can fully enjoy your free time without feeling adrift.

Pre-Retirement vs. First Year of Retirement

Understanding how fundamentally your financial mechanics change can help you prepare for the shock. Here is a look at how your daily financial life shifts the moment you retire:

| Financial Area | Pre-Retirement Reality | First Year of Retirement Reality |

|---|---|---|

| Primary Income | Predictable bi-weekly employer paycheck | Self-generated from portfolio withdrawals, Social Security, and pensions |

| Tax Strategy | Maximizing deductions and deferring taxes into retirement accounts | Managing withdrawal brackets, Roth conversions, and avoiding IRMAA surcharges |

| Healthcare | Subsidized employer-sponsored group plan handled by HR | Navigating Medicare Parts A, B, D, and Supplement premiums independently |

| Investment Focus | Aggressive growth and regular dollar-cost averaging through payroll | Capital preservation, dividend income, and mitigating sequence of returns risk |

Avoiding Common Errors

The decisions you make in your first twelve months compound over the rest of your life. Protect your nest egg by sidestepping these frequent blunders:

- Filing for Social Security out of fear: Many new retirees claim benefits at age 62 simply because they fear the system will go bankrupt. Doing so locks in a permanently reduced benefit. Base your claiming strategy on mathematical break-even analysis and personal longevity, not sensational headlines.

- Ignoring the “Tax Torpedo”: Pulling too much money from a traditional IRA for a large purchase can push your income over the threshold where your Social Security benefits become highly taxable. Plan your major withdrawals holistically across multiple tax years.

- Keeping an aggressive accumulation portfolio: If you retire with a portfolio entirely heavily weighted in aggressive growth stocks, you expose yourself to disastrous losses if a bear market hits in year one. Rebalance your portfolio to match your new income needs.

When DIY Isn’t Enough

While you might have successfully managed your own 401(k) allocations during your working years, the decumulation phase of retirement introduces complex legal and tax hurdles. Consider bringing in a professional if you face the following scenarios:

- Navigating IRMAA and Medicare Transitions: If you had a major liquidity event, sold a home, or received a large executive bonus right before retiring, a professional can help you file Form SSA-44 to request a reduction in your Medicare IRMAA surcharges based on a “life-changing event” (such as work stoppage).

- Pension Lump Sum vs. Annuity Decisions: If your former employer offers a defined benefit pension, deciding between a lifetime monthly payout and a single lump sum requires advanced actuarial modeling, inflation analysis, and risk assessment.

- Complex Estate Planning: Ensuring your assets transfer smoothly to your heirs or chosen charities requires more than a simple will. Establishing living trusts, minimizing estate taxes, and updating beneficiary designations demands specialized legal guidance.

Frequently Asked Questions

Will my Social Security benefits keep up with inflation?

The government implements a Cost of Living Adjustment (COLA) designed to protect the purchasing power of your benefits. For 2026, the SSA approved a 2.8 percent increase. While this helps, it may not perfectly match your personal inflation rate, especially regarding the rapidly rising costs of healthcare and housing.

What is the standard Medicare Part B premium for 2026?

The base monthly premium for Medicare Part B in 2026 is $202.90. However, higher-income retirees will pay more due to income-related surcharges (IRMAA).

Do I still get a standard tax deduction in retirement?

Yes. In fact, for the 2026 tax year, the standard deduction is $32,200 for married couples filing jointly and $16,100 for single filers. Additionally, if you are 65 or older, you are eligible for an extra standard deduction amount, which further reduces your taxable income.

Can I work part-time without hurting my Social Security?

If you have reached your Full Retirement Age (FRA), you can earn as much as you want without penalty. If you claim benefits before your FRA and continue working, the Social Security Administration will temporarily withhold a portion of your benefits if your earnings exceed the annual limit.

Your Next Steps

The first year of retirement is less of a finish line and more of a starting block. Treat this transition as an active, engaging project. Take the time to build a detailed withdrawal budget, map out your tax strategy, and intentionally design your new daily routine. Use the vast resources available through official government portals to verify the current rules surrounding your specific benefits. You spent a lifetime earning this freedom; now is the time to optimize it so you can enjoy your golden years with absolute confidence.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: April 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.