Your grocery bill consumes a massive portion of your retirement budget, but relocating to the right town can instantly stretch your fixed income. While inflation and supply chain issues keep food prices high nationally, specific regional hubs—often located near agricultural centers or major distribution networks—offer significantly lower grocery costs. The Council for Community and Economic Research continually tracks these localized price differences, revealing that retirees in certain markets pay up to twenty percent less at the checkout counter. If you want to stop overpaying for basic staples, moving to an affordable community provides a permanent solution. Here are seven retirement towns where residents consistently spend less on their weekly groceries.

1. McAllen, Texas

Located at the southern tip of Texas in the fertile Rio Grande Valley, McAllen serves as a massive agricultural conduit for the United States. Because the region produces a staggering volume of citrus, melons, and winter vegetables, local supermarkets bypass the steep transportation costs that plague coastal cities. Recent data from the Council for Community and Economic Research (C2ER) ranks McAllen as having the third-lowest grocery costs in the entire country.

Beyond the checkout counter, McAllen offers a powerful financial environment for seniors. Texas famously levies no state income tax. When the Social Security Administration implemented the 2.8 percent Cost-of-Living Adjustment (COLA) for 2026, McAllen residents kept every penny of that increase at the state level. The warm climate also drastically reduces winter heating bills, leaving more room in your budget to enjoy an active senior lifestyle.

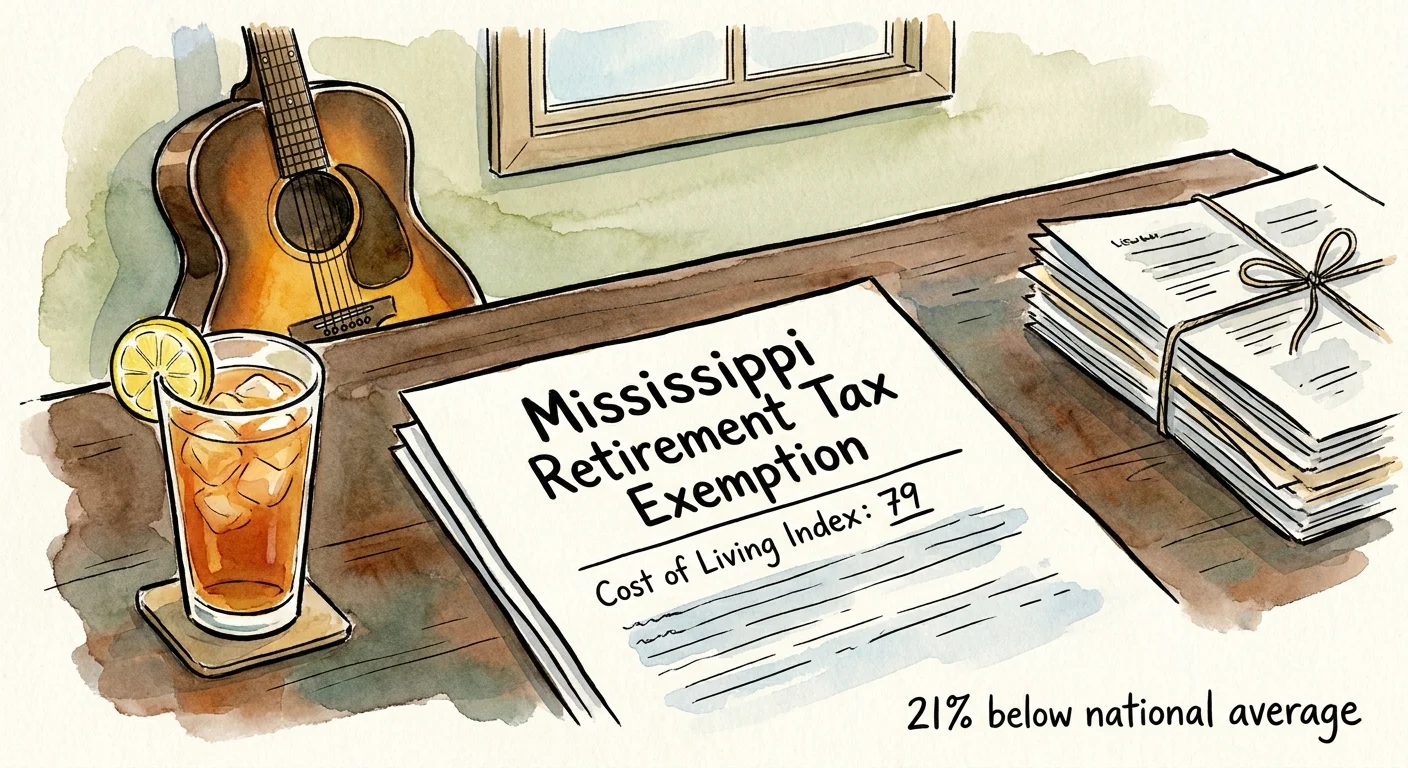

2. Tupelo, Mississippi

Widely recognized as the birthplace of Elvis Presley, Tupelo has quietly transformed into one of the most financially advantageous retirement destinations in America. The city frequently tops affordability metrics, boasting an overall cost of living index of 79—meaning it costs roughly 21 percent less to live here than the national average. Mississippi consistently ranks among the states with the lowest absolute grocery prices, heavily insulating retiree budgets from food inflation.

Tupelo operates as a regional commercial hub, ensuring healthy competition among grocery chains and local markets. Furthermore, Mississippi offers some of the most generous tax policies for seniors in the nation. The state completely exempts qualified retirement income from taxation, including Social Security benefits, public and private pensions, and IRA withdrawals. This combination of cheap food and zero retirement taxes creates exceptional cash flow for your later years.

3. Kalamazoo, Michigan

Moving north, Kalamazoo consistently ranks more than twenty percent below the national average for living costs. Surrounded by robust Midwestern farmland, the local food supply chain is incredibly short. Supermarkets and independent grocers in the area enjoy direct access to affordable dairy, corn, apples, and seasonal produce, directly reducing the prices you see on the shelves.

Kalamazoo maintains a strong network of local farmers’ markets, allowing retirees to purchase fresh, healthy food directly from growers. Michigan has also improved its tax landscape for older adults by phasing in significant exemptions for pension income. With excellent local healthcare facilities and affordable housing options, Kalamazoo proves that you do not need to move to the deep south to protect your retirement savings.

4. Salina, Kansas

Nestled in the agricultural heartland, Salina benefits immediately from its proximity to massive farming and ranching operations. Kansas stands as a top national producer of wheat, beef, and dairy. When your food travels mere miles rather than crossing multiple time zones, prices plummet. Salina holds a highly competitive cost of living index, making it an ideal destination for seniors living on a strict fixed income.

Residents enjoy substantial savings on high-ticket grocery items like meat and pantry staples. Salina also offers a peaceful, senior-friendly lifestyle with low property taxes and a tight-knit community feel. The city provides enough commercial infrastructure to ensure you have multiple shopping choices without the traffic and premium pricing of a major metropolitan area.

5. Richmond, Indiana

Positioned strategically near the Ohio border, Richmond operates as a vital distribution hub for the Midwest. Major grocery chains and logistics companies maintain distribution centers in this corridor. Because retailers spend less money transporting goods to local stores, they pass those logistical savings directly to consumers.

Richmond offers a cost of living index of 81, leaving plenty of breathing room in a standard retirement budget. Indiana taxes income at a low flat rate and completely exempts Social Security benefits. With a charming historic downtown, affordable real estate, and remarkably low food costs, Richmond offers practical stability for retirees who want their dollar to go further.

6. Harlingen, Texas

Just a short drive from McAllen, Harlingen provides a quieter alternative while maintaining the exact same agricultural and geographical advantages. The city’s cost of living index sits at an impressive 80. Retirees who prefer a slightly slower pace flock here for the warm winters and rock-bottom prices on fresh food.

Harlingen is heavily populated by “Winter Texans”—retirees from the Midwest and Canada who relocate seasonally. This creates a built-in community for newcomers. You get access to the same inexpensive produce from the Rio Grande Valley, the same zero-percent state income tax environment, and a highly competitive local grocery market eager to cater to budget-conscious seniors.

7. Decatur, Illinois

Known globally as the Soybean Capital of the World, Decatur is deeply entrenched in the American food production industry. With a cost of living index of 79, it ties with Tupelo as one of the most affordable urban areas in the United States. Because Decatur is a massive processing center for grains and agricultural products, local grocery prices remain exceptionally low.

While Illinois does have higher property taxes than some southern states, it counterbalances this by completely exempting Social Security benefits and most pension income from state taxation. Retirees in Decatur spend significantly less on basic staples, allowing them to redirect their funds toward travel, hobbies, or spoiling their grandchildren.

Why Location Dictates Your Grocery Bill

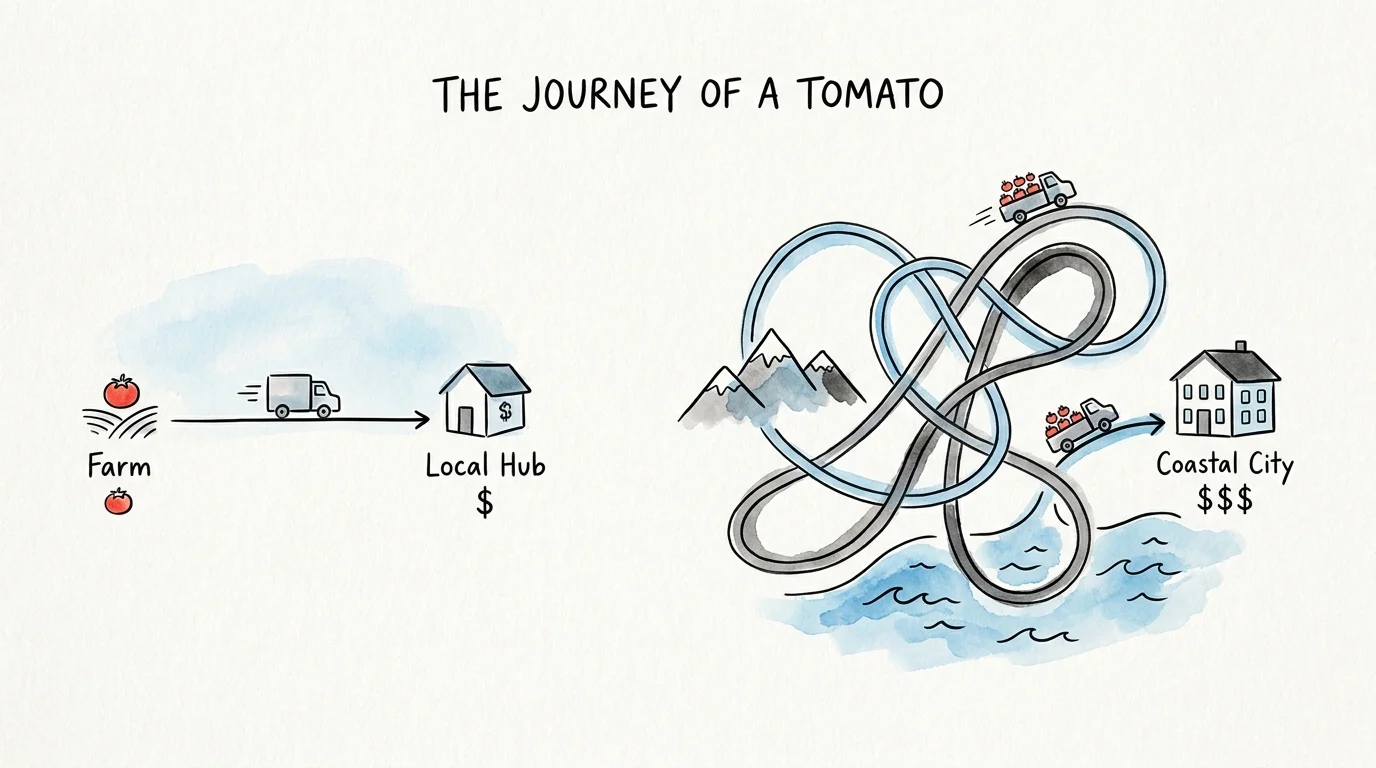

Food prices do not rise uniformly across the country. Your zip code plays a massive role in determining how much you pay for a carton of eggs or a pound of beef. Several structural factors drive these localized price differences:

- Supply Chain Proximity: Towns located near agricultural centers or massive distribution hubs cut out the middleman. The less fuel required to transport a tomato, the cheaper that tomato will be.

- Commercial Real Estate Costs: Supermarkets pass their overhead costs onto you. In expensive coastal cities, grocers pay exorbitant rent and property taxes, forcing them to mark up food. In affordable towns like Decatur or Salina, commercial rent is low, keeping grocery prices in check.

- State and Local Regulations: Energy costs, labor laws, and fuel taxes directly impact how much it costs to keep the lights on and the refrigerators running at the local supermarket.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor and Philanthropist

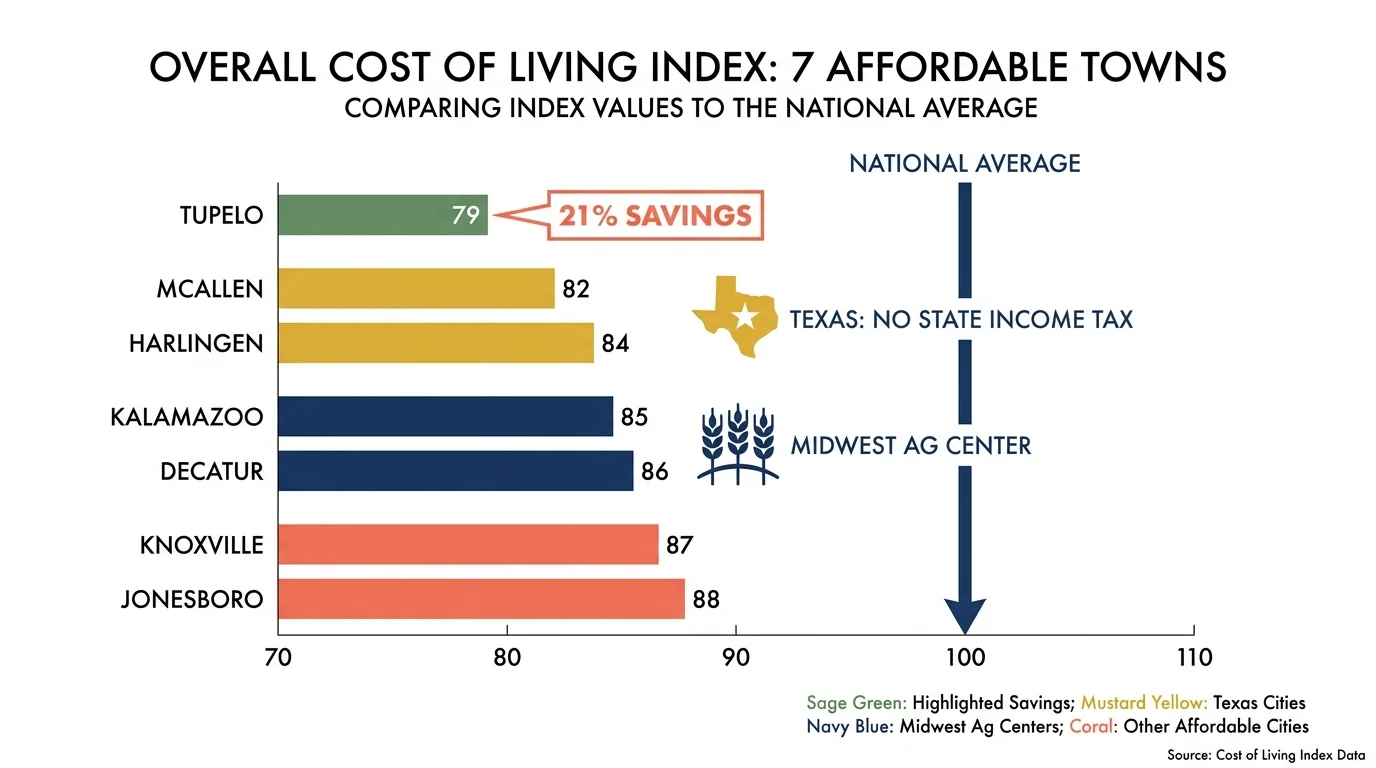

At a Glance: Comparing Affordable Retirement Hubs

Use this quick reference guide to see how these affordable towns stack up regarding living costs and state taxation on your federal benefits.

| Retirement Town | Cost of Living Index (100 = Avg) | Primary Grocery Advantage | State Tax on Social Security |

|---|---|---|---|

| Tupelo, MS | 79 | Regional distribution hub | Exempt |

| Decatur, IL | 79 | Massive agricultural processing | Exempt |

| McAllen, TX | 80 | Rio Grande Valley produce | Exempt (No State Income Tax) |

| Harlingen, TX | 80 | Year-round fresh agriculture | Exempt (No State Income Tax) |

| Richmond, IN | 81 | Midwest logistics corridor | Exempt |

| Salina, KS | 82 | Heartland grain and meat | Exempt |

| Kalamazoo, MI | Consistently below 85 | Direct-to-consumer farming | Exempt |

Avoiding Common Errors

Focusing solely on food prices while ignoring healthcare networks is a disastrous retirement mistake. You cannot eat cheap groceries if a local hospital cannot treat your medical conditions. When evaluating a new town, you must research the healthcare infrastructure.

The standard Medicare Part B premium requires $202.90 per month in 2026. If you relocate to a rural agricultural town with cheap groceries but no in-network specialists for your specific Medicare Advantage plan, your out-of-pocket medical expenses will quickly obliterate your food savings. Additionally, while the Inflation Reduction Act caps Medicare Part D out-of-pocket drug costs at $2,100 for 2026, your prescriptions still require a local pharmacy that accepts your exact plan. Always verify that a prospective retirement town has robust medical facilities and in-network providers before you sign a lease or buy a home.

When DIY Isn’t Enough

Relocating across state lines to stretch your fixed income requires complex tax forecasting. You should hire a licensed financial planner or tax professional when:

- You hold significant tax-deferred assets: If you plan to take large distributions from a 401(k) or Traditional IRA, you need to calculate the exact state income tax impact. A town with cheap groceries might have punishing income tax brackets for IRA withdrawals.

- You rely on specific healthcare waivers: If you use state-specific Medicaid waivers for long-term care or in-home assistance, those benefits do not transfer across state lines. You must apply under the new state’s rules, which requires professional legal navigation.

- You are selling a highly appreciated home: If you plan to sell a primary residence in an expensive coastal city to buy a cheap home in the Midwest, you need an Internal Revenue Service specialist to help you navigate capital gains exemptions and properly shield your profits.

Frequently Asked Questions

Will moving to a cheaper town reduce my Social Security benefits?

No. The Social Security Administration does not adjust your monthly retirement benefit based on your current state or city of residence. You will continue to receive the same federal payment regardless of where you live in the United States. Moving from an expensive city to an affordable one simply increases your purchasing power.

Do cheap groceries mean lower quality food?

Not at all. In towns located near agricultural hubs like McAllen or Salina, the food is often fresher than what you find in coastal cities. The lower price reflects reduced transportation and storage costs, not inferior quality. You are paying for the food itself, rather than the diesel fuel required to truck it across the country.

Should I factor Medicare premiums into my relocation budget?

Yes. While the standard Medicare Part B premium ($202.90 in 2026) is federal and remains the same regardless of where you live, your Medicare Advantage or Medicare Supplement (Medigap) premiums vary wildly by zip code. A town might have cheap groceries but highly expensive Medigap premiums. You must price out your specific health coverage using the tools available at AARP or Medicare.gov for your target zip code.

Take Control of Your Retirement Budget

Trimming your expenses does not have to mean sacrificing your quality of life. By strategically relocating to a town that structurally supports a lower cost of living, you can stretch your Social Security benefits and retirement savings significantly further. Research the towns listed above, take a scouting trip to visit local supermarkets, and evaluate the healthcare networks. With the right planning, you can comfortably enjoy your retirement years without stressing over the checkout total.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.