Retirement should be about enjoying the wealth you spent decades building, but hidden expenses can quietly drain your savings. Even careful budgeters often overlook subtle money leaks that compound into thousands of lost dollars each year. From unnecessary tax hits and creeping Medicare surcharges to zombie subscriptions and high-interest debt, fixing these inefficiencies is one of the most effective ways to instantly boost your monthly cash flow. By plugging these financial gaps, you protect your nest egg and free up capital for the things that actually matter—like travel, family, and peace of mind. Here are the most common retirement money leaks and exactly how you can stop them.

1. Medicare Surcharges and Penalties

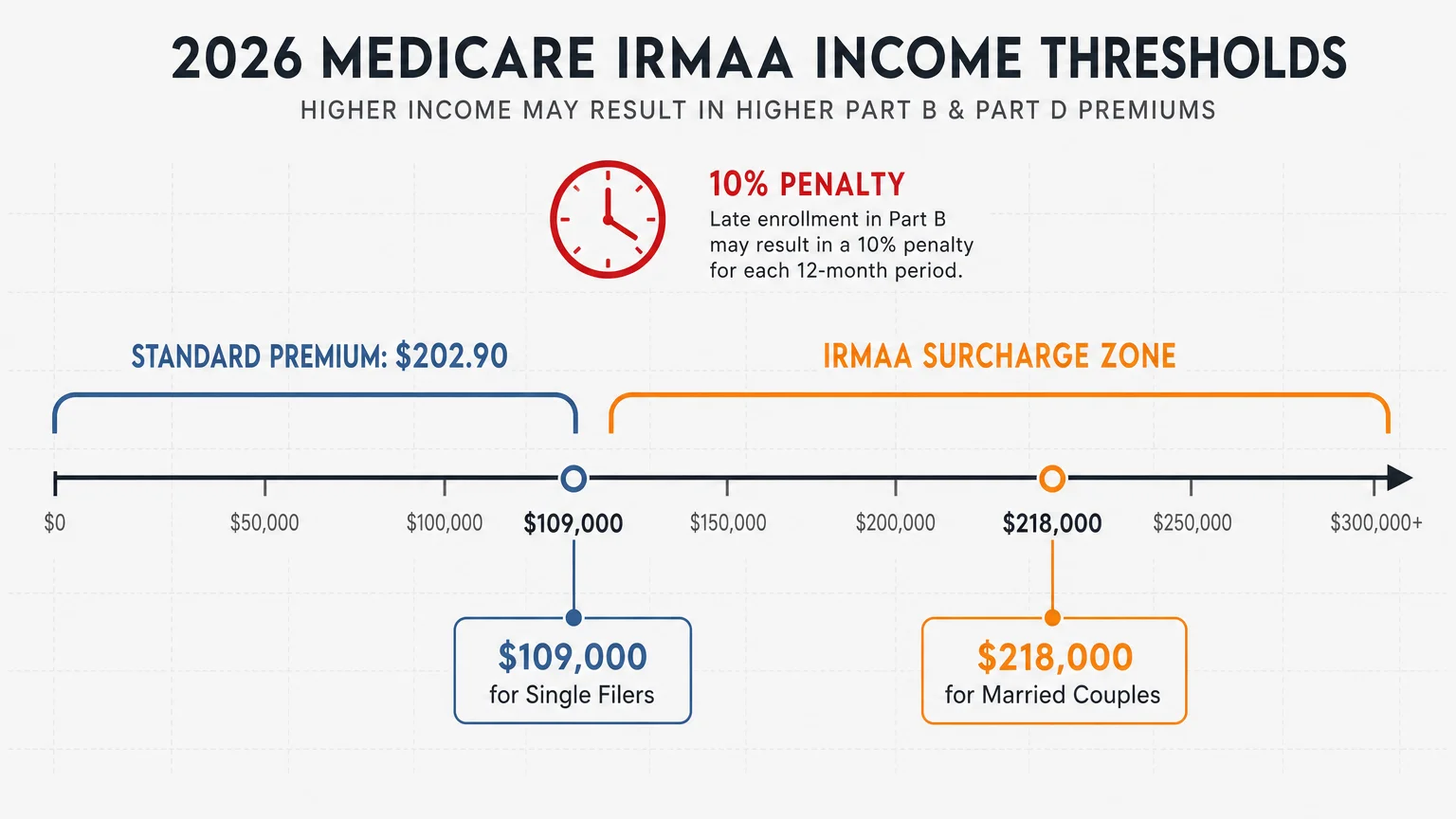

Healthcare is one of the largest expenses you will face in your later years, yet many retirees unknowingly overpay for their coverage. The standard Medicare Part B premium for 2026 is $202.90 per month, but if your income from two years prior crosses certain thresholds, you will be hit with an Income-Related Monthly Adjustment Amount—commonly known as IRMAA. For 2026, IRMAA surcharges begin if your modified adjusted gross income (MAGI) exceeds $109,000 for single filers or $218,000 for married couples filing jointly.

Another major leak involves missing your initial Medicare enrollment window. If you fail to sign up for Part B when you first become eligible at age 65—and you do not have qualifying creditable coverage from an employer—you face a permanent late enrollment penalty. Your monthly premium increases by 10% for every full 12-month period you delayed signing up. This penalty stays with you for life.

To plug this leak, you must be strategic about your income. If you experience a life-changing event such as retirement or the loss of a spouse, you can file form SSA-44 with the Social Security Administration to request a reduction in your IRMAA surcharge. Always monitor your withdrawal strategy so you do not accidentally bump yourself into a higher Medicare premium bracket just to cover a large, one-time purchase.

2. The High-Interest Debt Trap

Entering retirement with revolving credit card debt is like trying to sail a boat with a hole in the hull. Recent data from the Consumer Financial Protection Bureau and the Federal Reserve indicates that average credit card interest rates hover around an astronomical 21% in 2026. When you carry a balance at those rates, a massive portion of your fixed income goes strictly toward enriching the credit card issuer rather than paying down the principal.

If you are pulling money from your retirement accounts just to service high-interest debt, you are creating a secondary problem: you might be paying income taxes on those withdrawals, making the actual cost of your debt even higher. To stop this massive financial drain, prioritize eliminating your high-interest balances immediately.

- Consolidate your debt: Look into a personal loan or a balance transfer credit card offering a 0% introductory APR. A personal loan often carries a significantly lower interest rate than a standard credit card.

- Reassess your spending: Temporarily pause discretionary expenses until the revolving balances are cleared.

- Tap equity carefully: If appropriate for your situation, using a home equity line of credit might offer a lower interest rate, though you must be disciplined enough not to run up the credit cards again.

3. Zombie Subscriptions and Forgotten Memberships

The digital economy thrives on auto-renewing charges that quietly deduct money from your account each month. Studies show the average American spends upwards of $200 per month on subscriptions—many of which they rarely use or have completely forgotten about. These “zombie subscriptions” include streaming services, premium app features, meal delivery memberships, and unused gym passes.

“A budget is telling your money where to go instead of wondering where it went.” — Dave Ramsey, Personal Finance Expert

Because these charges are usually small individually—$10 here, $15 there—they slip past our mental accounting. However, allowing $150 a month to vanish on unused services costs you $1,800 a year. To fix this leak, print out your last three months of credit card and bank statements. Highlight every recurring charge. If you have not used a service in the past 30 days, cancel it. You can always resubscribe later if you genuinely miss it.

4. The “Family Bank” Subsidies

It is natural to want to help your children, but continuously subsidizing the lifestyles of self-sufficient adults is a fast track to draining your retirement portfolio. Many retirees keep their adult children on their family cell phone plans, pay their auto insurance premiums, or share expensive streaming accounts for years after the kids have entered the workforce.

Worse yet, some retirees pull from their 401(k) accounts to help their children buy a house or pay off student loans. While the intention is noble, you cannot secure a loan to fund your retirement, whereas your children have decades to earn income and build wealth. Have an honest conversation with your family about financial boundaries. Set a firm timeline for them to assume their own expenses, allowing you to protect the nest egg that must sustain you for the rest of your life.

5. Tax-Inefficient Withdrawals

How you pull money out of your accounts matters just as much as how much you withdraw. If you pull funds haphazardly, you might unnecessarily inflate your tax bill. With the impending expiration of the Tax Cuts and Jobs Act provisions at the end of 2025, tax brackets and standard deductions are shifting in 2026, making a calculated withdrawal strategy absolutely critical.

Another major tax leak involves ignoring Required Minimum Distributions (RMDs) from traditional IRAs and 401(k)s. If you miss an RMD deadline, the IRS levies an excise tax of 25% on the amount you failed to withdraw. Thanks to the SECURE 2.0 Act, you can reduce this penalty to 10% if you correct the mistake within a specific window, but it remains an entirely avoidable loss.

Understanding the tax status of your accounts is the first step to keeping more of your money. Review the Internal Revenue Service rules to ensure you are withdrawing from the most tax-efficient buckets first.

| Account Type | Tax Treatment on Contributions | Tax Treatment on Withdrawals |

|---|---|---|

| Traditional IRA / 401(k) | Contributions are typically tax-deductible | Taxed as ordinary income; subject to RMDs |

| Roth IRA / Roth 401(k) | Contributions are made with after-tax money | 100% tax-free if rules are met; no RMDs for original owners |

| Brokerage (Taxable) | Contributions are made with after-tax money | Subject to capital gains tax rates, which are often lower than income tax |

6. Outdated Insurance Policies

Insurance needs change dramatically as you age, yet many retirees continue paying for coverage designed for a different phase of life. Consider your life insurance policy. If your mortgage is paid off, your children are financially independent, and your surviving spouse has adequate resources, continuing to pay expensive premiums on a large term or whole life policy might be an unnecessary drain.

Similarly, your auto insurance needs adjustment. When you stop commuting to work every day, your annual mileage drops significantly. Call your auto insurance provider to update your status from “commuter” to “pleasure use.” This simple phone call can reduce your premiums significantly. Furthermore, review your deductibles; if you have robust emergency savings, raising your deductibles can lower your monthly payments.

7. Lazy Cash and Avoidable Bank Fees

Leaving a large cash reserve in a traditional checking or savings account paying 0.01% interest is a silent leak caused by inflation. When inflation runs higher than your interest rate, your money actively loses purchasing power every single day.

“The miracle of compounding returns is overwhelmed by the tyranny of compounding costs.” — John Bogle, Founder of Vanguard Group

While you certainly need liquid emergency funds, you should make sure that cash is working for you. Moving your cash buffer to a high-yield savings account or a ladder of Certificates of Deposit (CDs) can generate hundreds—if not thousands—of dollars in passive income each year. Additionally, comb through your bank statements to hunt down maintenance fees, paper statement fees, and low-balance penalties. Switch to a credit union or an online bank that offers truly free checking for seniors.

8. Missed Property Tax Relief and Senior Discounts

Property taxes are often a retiree’s largest recurring expense, especially once the mortgage is paid off. Unfortunately, many homeowners simply pay the bill without realizing they qualify for substantial relief. Many states and local municipalities offer homestead exemptions, property tax freezes, or specific reductions for homeowners over the age of 65. You usually have to proactively apply for these programs at your local tax assessor’s office.

Beyond property taxes, ignoring everyday senior discounts is a steady leak. From grocery stores and restaurants to public transit and state parks, discounts of 10% to 15% are widely available but rarely advertised. Always ask if a senior discount is available before you pay; over a year, these small savings add up to a sizable amount of retained cash.

Pitfalls to Watch For

As you work to eliminate these money leaks, be careful not to create new problems in the process. Avoid these common mistakes:

- Canceling Life Insurance Prematurely: Before you drop a life insurance policy, confirm with absolute certainty that your spouse would not face a financial shortfall if your pension or Social Security benefits are reduced upon your passing.

- Chasing Yield Without Understanding Risk: Do not move your safe emergency cash into volatile investments just to get a higher return. High-yield savings accounts are FDIC-insured; risky dividend stocks are not. Use resources like Investor.gov to verify the safety of financial products.

- Ignoring Tax Drag on Reallocations: If you decide to sell off investments in a taxable brokerage account to pay off a mortgage or consolidate debt, calculate the capital gains tax you will owe before making the trade.

Getting Expert Help

You do not have to navigate the complexities of retirement cash flow alone. Consider reaching out to a professional in the following scenarios:

- Tax Strategy: A Certified Public Accountant (CPA) can help you sequence your withdrawals efficiently, manage RMDs, and explore Roth conversions before tax brackets potentially shift.

- Medicare Navigation: A licensed, independent Medicare broker can review your prescriptions and health needs to ensure you are enrolled in the most cost-effective Part D or Advantage plan during the Annual Enrollment Period.

- Comprehensive Planning: A fee-only fiduciary financial planner can run long-term projections to show you exactly how much you can safely withdraw each year without outliving your assets.

Taking control of your retirement expenses does not mean sacrificing your quality of life. It simply means directing your money intentionally toward your goals rather than letting it slip through the cracks. Take an afternoon to audit your accounts, make the necessary adjustments, and enjoy the peace of mind that comes with a watertight financial plan.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.