Deciding where to spend your retirement years is one of the most consequential financial choices you will face. While staying in your current home might feel comfortable, subtle warning signs often indicate that your living situation no longer serves your best interests. Many retirees discover that relocating unlocks hidden home equity, reduces annual tax burdens, and provides better access to necessary healthcare services. Identifying the friction points in your daily life can help you transition to a location that genuinely supports your goals. Evaluating your physical environment, local tax laws, and proximity to your support network reveals whether it is time to pack up and find a new place to thrive.

1. Your Housing Costs Constrict Your Fixed Income

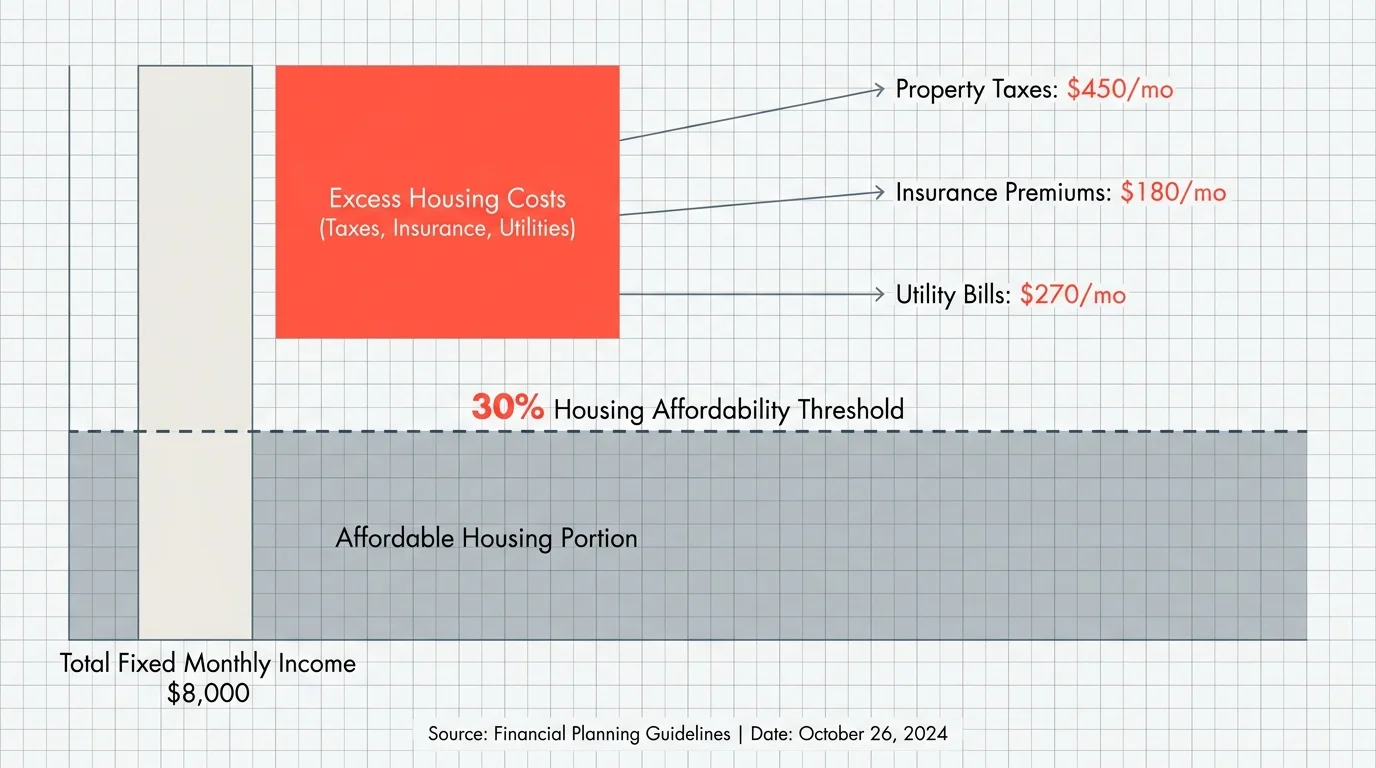

Living on a fixed income requires a delicate, highly managed balance between cash flowing in and expenses flowing out. If property taxes, homeowners insurance premiums, and utility bills consume an increasingly massive percentage of your monthly retirement distributions, your current geographic location is working actively against your financial security. Many retirees rely on safe withdrawal rates from their investment portfolios; however, soaring local tax assessments and inflation quickly derail even the most carefully calculated withdrawal strategies.

Relocating to an area with lower property taxes and more affordable utilities instantly creates vital breathing room in your monthly budget. Instead of selling off precious portfolio assets during market downturns simply to pay an inflated property tax bill, you preserve your nest egg for actual enjoyment. Run the numbers on your current housing expenses. If housing-related costs exceed 30 percent of your fixed monthly income, moving to a lower-cost region offers an immediate and permanent financial upgrade.

2. Your Home Equity Presents a Massive Arbitrage Opportunity

Your home likely represents a substantial, highly concentrated portion of your net worth. Over the past few decades, property values in certain coastal and major metropolitan areas skyrocketed to unprecedented heights. The national median home price sits at approximately $422,300 as of mid-2026. If you reside in a high-cost market, your home might command double or even triple that national average. This dynamic creates a powerful financial maneuver known as geographic housing arbitrage.

Selling a highly appreciated property allows you to purchase a comfortable, modern home in a lower-cost state entirely in cash. Executing this strategy eliminates mortgage debt permanently and unlocks hundreds of thousands of dollars in previously trapped equity. You can then reinvest this freed-up capital into income-producing assets, bulk up your emergency reserves, or use it to fund the travel and lifestyle experiences you dreamed about during your working years.

3. Your State Actively Penalizes Your Retirement Income

Taxes do not stop simply because you stop working. The specific state you choose for your retirement heavily dictates how much of your wealth actually remains in your pocket. States handle the taxation of pensions, 401(k) withdrawals, and Social Security benefits very differently, and these legislative choices compound over a twenty or thirty-year retirement.

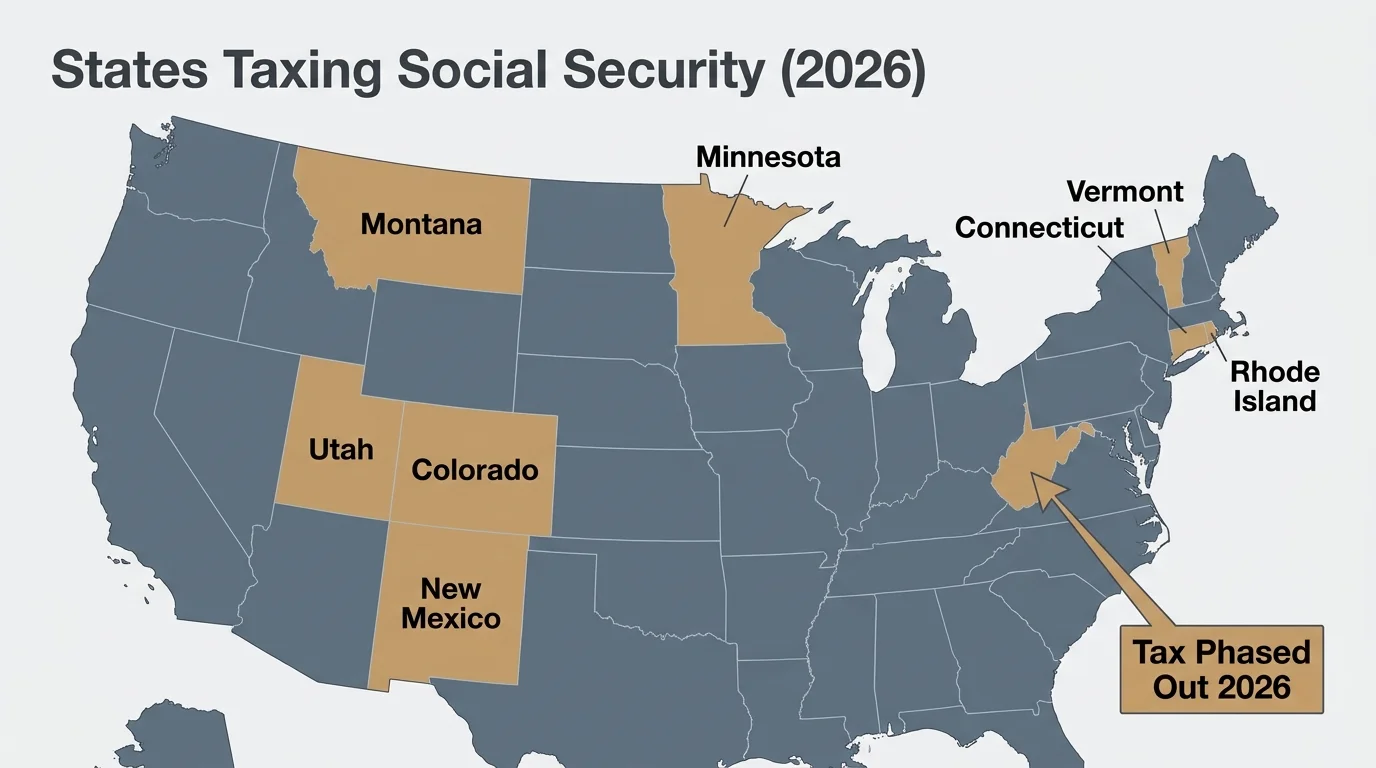

For the 2026 tax year, eight states still impose income taxes on Social Security benefits: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont. Conversely, West Virginia officially phased out its Social Security tax entirely for 2026. Furthermore, several states—such as Florida, Texas, and Nevada—lack a state income tax altogether. If your current state aggressively taxes your hard-earned retirement distributions, establishing legal residency in a tax-friendly jurisdiction mathematically extends the life of your portfolio. Always consult the Internal Revenue Service (IRS) and your state’s department of revenue to accurately project your comprehensive tax liabilities across different state borders.

4. The Local Healthcare Network Falls Short of Your Needs

Access to high-quality healthcare inevitably becomes a dominant priority as we age. Even with federal insurance programs, your geographic location heavily influences your out-of-pocket medical costs and the caliber of specialized care you receive. In 2026, the standard Medicare Part B premium rose to $202.90 per month, alongside an annual deductible of $283. While these foundational federal premiums remain standard regardless of where you live, your specific county strictly dictates the availability, pricing, and network scope of Medicare Advantage and Medigap supplemental plans.

If you must regularly travel long distances to reach essential specialists, or if your local hospital systems consistently receive poor safety ratings, relocating closer to elite medical hubs becomes a medical necessity rather than a luxury. Better proximity to world-class healthcare networks ensures faster treatment times, offers more robust specialized care options, and heavily reduces the physical toll of traveling for necessary medical appointments. You should proactively review plan availability in potential new locations using Medicare.gov to ensure continuous, strong coverage.

5. Your Physical Home Fights Against Aging in Place

Take a highly objective walk through your home and assess its daily functionality. Steep staircases, narrow hallways, sunken living rooms, and second-story primary bedrooms create significant, sometimes dangerous friction for aging in place. While you might navigate these physical obstacles perfectly fine today, human mobility can change abruptly due to unexpected health events.

Retrofitting an older, multi-level home with main-floor primary suites, widened doorways, walk-in showers, and wheelchair-accessible entryways requires immense capital, invasive construction, and extreme patience. Often, selling your current property and purchasing a newer single-story home with universal design principles already built-in proves far more economical and far less stressful. Recognizing the physical limitations of your current house early allows you to move deliberately on your own terms, rather than scrambling to relocate during an active medical crisis.

6. Geographic Isolation Weakens Your Support Network

Retirement affords you the invaluable time to deeply invest in your personal relationships. Yet, if your adult children, grandchildren, or closest lifelong friends live several time zones away, maintaining those vital connections becomes physically and financially exhausting. Soaring flight costs, unpredictable airport delays, and general travel fatigue severely limit how often you actually see your loved ones.

Relocating closer to your core support network yields profound emotional and logistical dividends. Beyond the pure joy of attending weekend soccer games or hosting casual Sunday family dinners, living near loved ones provides a highly critical safety net. Having family nearby to assist with unexpected medical recoveries, household management, or daily transportation tasks drastically reduces your eventual reliance on expensive paid caregiving services. Current data shows retirees increasingly favor relocating to states like Florida, Texas, and the Carolinas, often following broad family migration patterns to optimize both affordability and deep personal connection.

7. Constant Home Maintenance Drains Your Time and Joy

Traditional homeownership comes attached to an endless, demanding checklist of chores. Cleaning gutters, mowing sprawling lawns, shoveling heavy winter snow, and repairing aging HVAC systems require intense physical labor and constant vendor management. You worked your entire adult life to reach the freedom of retirement—spending your hard-earned time managing relentless property maintenance represents a terrible return on your energy.

If looking at your weekend house-project to-do list causes genuine dread, it is time to downsize or transition to a vastly different living arrangement. Moving to a low-maintenance townhome, condominium, or a 55-plus active adult community legally shifts the heavy exterior maintenance burden to a homeowners association. You instantly reclaim your daily schedule, allowing you to focus completely on hobbies, travel, volunteering, and relaxation.

8. The Climate Actively Restricts Your Daily Lifestyle

Local weather profoundly impacts your daily quality of life and physical well-being. If harsh, freezing winters force you to remain indoors for four to five months out of the year, or if extreme summer humidity prevents you from safely enjoying outdoor activities, your environment is actively limiting your retirement joy. Furthermore, dealing with icy driveways and snow-covered stairs introduces severe, unnecessary physical fall risks.

Relocating to a climate that perfectly aligns with your preferred lifestyle enables healthy, year-round activity. Whether you prefer the dry, predictable heat of the Southwest for year-round tennis and golf, or the mild, temperate coastal regions for daily morning beach walks, matching your geographic location to your favorite hobbies keeps you physically active, socially engaged, and mentally sharp.

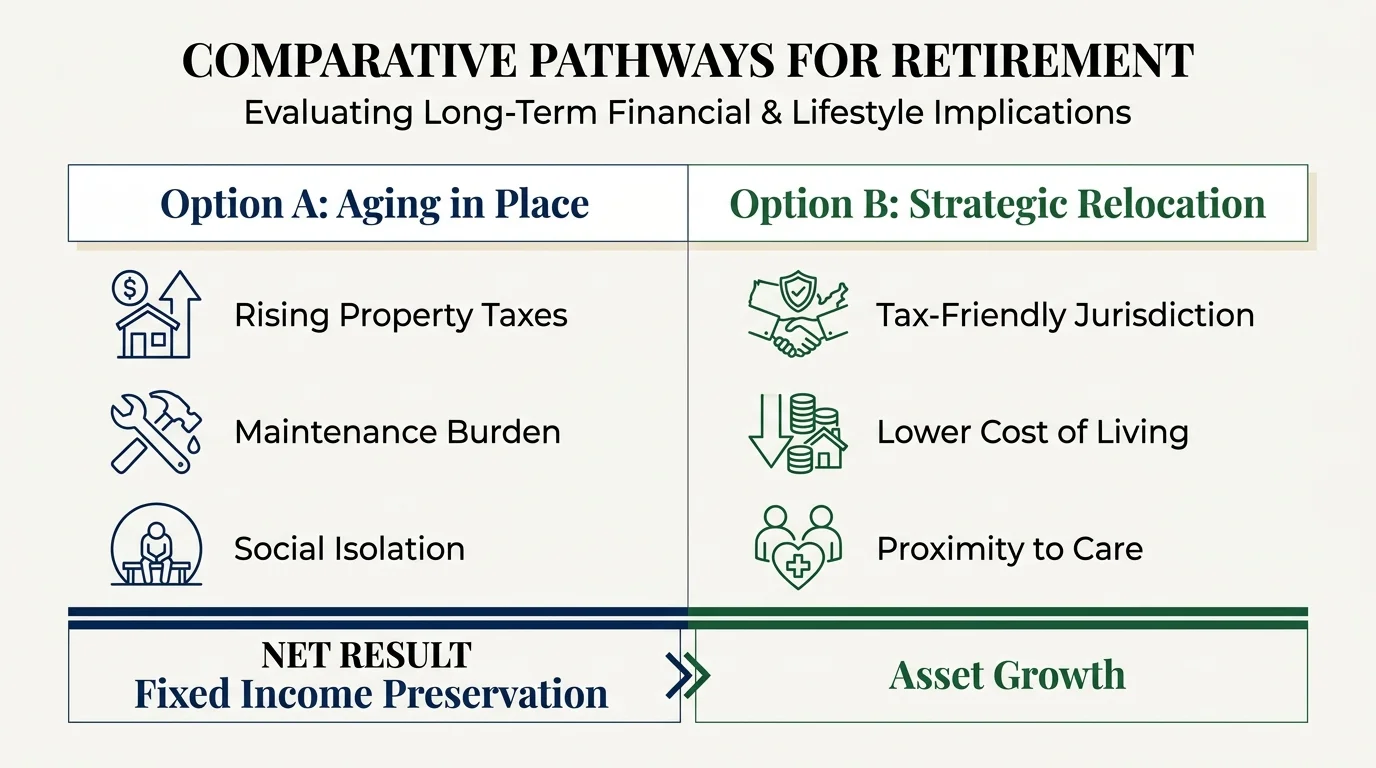

Comparing Your Options: Staying Put vs. Relocating

To provide a clear, objective perspective on how a potential move impacts your lifestyle and finances, consider this breakdown of the factors involved in staying in place versus pulling up stakes:

| Decision Factor | Staying in Your Current Home | Relocating to a Retirement-Friendly State |

|---|---|---|

| State & Local Taxes | You remain entirely subject to existing property tax hikes and potential state taxation on your Social Security and pension income. | You gain the opportunity to deliberately select a state with no income tax and secure highly favorable property tax exemptions for seniors. |

| Home Equity Usage | Your capital remains permanently locked inside the property walls unless you utilize costly financial products like a reverse mortgage or a HELOC. | You can seamlessly cash out your peak home equity, buy a cheaper home entirely in cash, and invest the remaining difference for steady income. |

| Healthcare Access | You are strictly limited to the current network of local doctors and the regional Medicare Advantage plan options available in your existing county. | You possess the ability to deliberately move near top-tier, nationally ranked hospital systems and secure access to better-rated supplemental coverage networks. |

| Property Maintenance | You bear the full physical and financial burden of maintaining an aging property, replacing roofs, and managing extensive seasonal yard work. | You secure the chance to purchase a modern, low-maintenance home or join an HOA that professionally handles all exterior upkeep on your behalf. |

Avoiding Common Relocation Errors

Even when all financial and emotional signs heavily point toward moving, poor execution can quickly sour your retirement dreams. The absolute most frequent misstep retirees make involves moving to a beloved vacation destination without ever experiencing its off-season realities. A charming coastal town that feels magical during a vibrant two-week summer trip might shut down completely in the dead of winter, leaving you socially isolated and severely lacking access to basic community amenities.

Another prevalent error is failing to research the new location’s exact healthcare infrastructure prior to closing on a home. A picturesque mountain cabin looks idyllic in real estate photos, but if the nearest Level 1 trauma center sits three hours away down a winding road, you are unnecessarily exposing yourself to massive medical risk. Furthermore, do not blindly assume that a state boasting no income tax is automatically cheaper across the board. You must carefully factor in local sales taxes, annual vehicle registration fees, and homeowners insurance premiums—especially in coastal areas highly prone to extreme weather events. Always calculate the full, comprehensive cost of living before you ever hire the moving truck.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

When DIY Isn’t Enough

Managing a major cross-country relocation involves significantly more than simply packing cardboard boxes; it frequently triggers highly complex financial and legal hurdles. Seeking professional guidance proves absolutely essential in several specific scenarios.

- Establishing a Legal Domicile: Moving to a tax-free state to escape high taxes requires strictly proving your new residency. If you maintain property or strong ties in your former high-tax state, aggressive state revenue departments may legally challenge your move and demand back taxes. A certified public accountant (CPA) will guide you through correctly severing ties and establishing an ironclad legal domicile.

- Updating Estate Plans: Estate and probate laws vary wildly by state. What served as a perfectly valid living trust or durable power of attorney in your old state might face heavy legal friction or rejection in your new one. An elder law attorney must review and formally update your essential documents to ensure your healthcare directives and financial wishes remain legally protected under your new local statutes.

- Managing Large Liquidity Events: If you successfully sell a highly appreciated primary residence and suddenly hold hundreds of thousands of dollars in cash, parking it in a standard checking account wastes its massive compounding potential. A qualified fiduciary financial planner helps you reinvest these funds efficiently, deploying careful strategies to mitigate capital gains exposure and generate a steady, reliable stream of retirement income.

Frequently Asked Questions

-

Does changing states affect my monthly Social Security payments?

Your gross federal Social Security benefit remains exactly the same regardless of where you live within the United States. However, your net take-home amount may change based on whether your new state actively taxes those benefits. You must update your address directly through SSA.gov to ensure vital correspondence and annual tax forms reach you seamlessly. -

Will my Medicare coverage automatically follow me if I move across the country?

Original Medicare (Parts A and B) applies seamlessly nationwide across any provider or facility that accepts Medicare. However, if you utilize a Medicare Advantage (Part C) plan or a standalone Part D prescription drug plan, you generally must enroll in a brand-new plan specific to your new zip code. Moving permanently triggers a recognized Special Enrollment Period, granting you the crucial opportunity to switch plans safely without incurring a coverage gap or financial penalty. -

How long do I actually need to live in a new state to officially claim residency?

The “183-day rule” serves as a common baseline, meaning you must physically spend more than half the calendar year inside the new state. Yet, state tax auditors look closely at multiple factors far beyond mere physical presence. They will investigate where you register your vehicles, where you are registered to vote, where you hold your primary banking relationships, and where your primary physicians are located. Documenting your transition comprehensively and legally protects you during a potential residency audit.

Relocating during your retirement years requires courage, flexibility, and meticulous financial planning, but the long-term rewards—significantly lower living costs, superior access to healthcare, and deeper family connections—often completely transform your daily life. Listen carefully to the subtle frustrations you experience in your current environment; they are usually guiding you toward a more intentional and deeply fulfilling chapter. Take the necessary time to run the hard math, visit prospective communities during different and difficult weather seasons, and actively build a living situation that works just as hard for you as you did for your retirement.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.