Many retirees carefully plan their income strategy for decades, only to watch their monthly cash flow slowly erode from overlooked expenses. A budget leak doesn’t announce itself with a loud warning; it hides in the small, automatic payments and unoptimized financial habits that drain your accounts over time. Whether you are paying unnecessary surcharges on Medicare premiums, ignoring the latest senior tax deductions, or leaving excess cash in low-yield savings accounts, these hidden costs quietly shrink your spending power. Reclaiming your financial independence requires finding these silent leaks and patching them quickly. By identifying the six most common ways money disappears each month, you can keep more of your retirement income exactly where it belongs—in your pocket.

1. You Pay Medicare Surcharges You Could Avoid

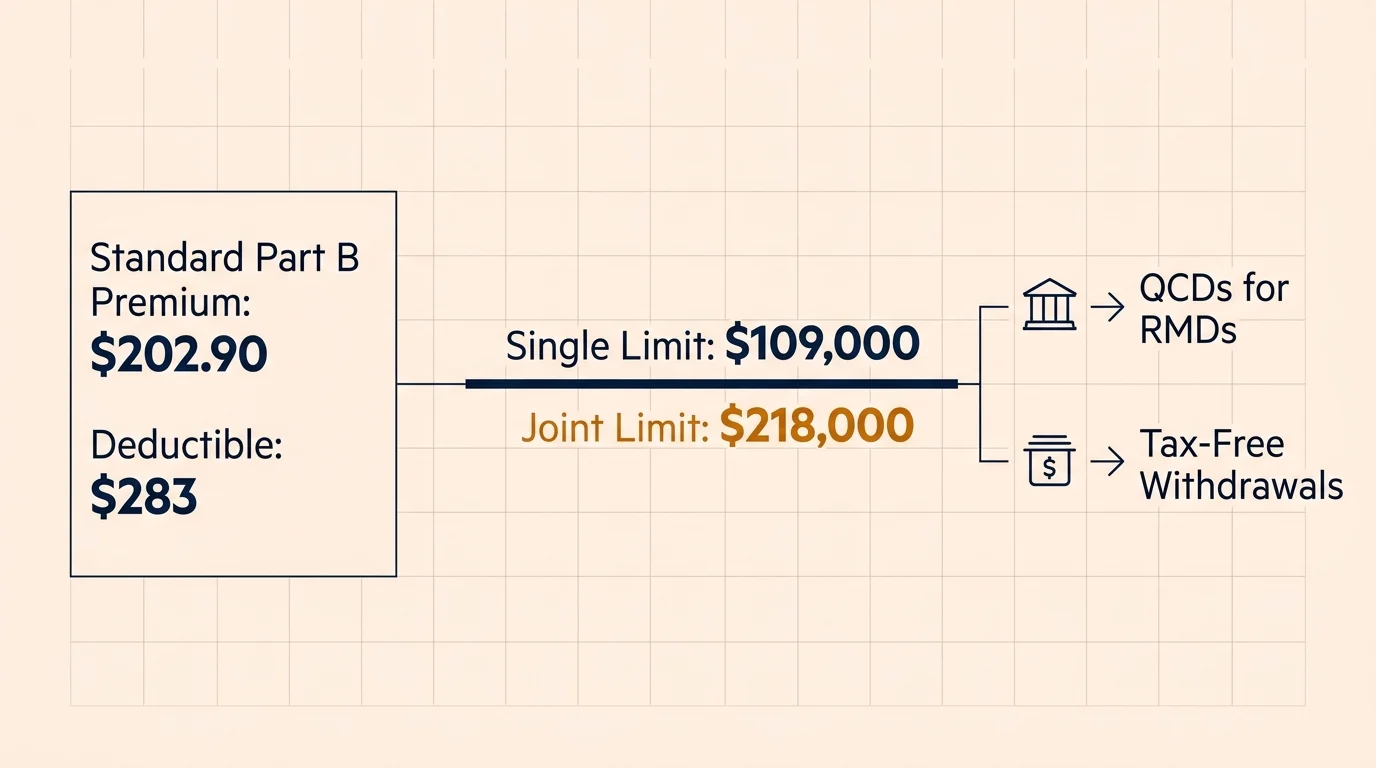

Do not assume Medicare is a fixed, unchangeable cost. In 2026, the standard Part B premium is $202.90, and the annual deductible is $283. However, many retirees unknowingly trigger the Income-Related Monthly Adjustment Amount (IRMAA), an extra surcharge tacked onto Part B and Part D premiums. If your modified adjusted gross income from two years prior exceeds $109,000 as a single filer or $218,000 as a joint filer, you pay this penalty. A massive budget leak occurs when retirees take large, poorly timed withdrawals from traditional IRAs, artificially inflating their income and triggering IRMAA.

You can patch this leak through strategic tax planning. Use Qualified Charitable Distributions (QCDs) to satisfy Required Minimum Distributions (RMDs) without adding to your taxable income. Alternatively, rotate your withdrawals between taxable, tax-deferred, and tax-free accounts to stay safely below the IRMAA thresholds.

Another major healthcare leak stems from brand loyalty. Retirees often stick with the same Part D prescription drug plan or Medicare Advantage plan year after year. Insurance carriers frequently change their formularies, copays, and network providers. A medication that cost you $15 last year might jump to $45 this year if your plan shifts its tiers. Review your coverage every single year during the Annual Enrollment Period (October 15 to December 7). Compare your current medications against the newest plans on the official Medicare.gov website. Switching to an optimized plan can save you hundreds, if not thousands, of dollars annually.

2. Your Cash Is Trapped in Low-Yield Savings Accounts

Leaving excess cash in a traditional checking or savings account represents one of the most common and damaging financial leaks. In an era where the Social Security Administration set the 2026 Cost-of-Living Adjustment (COLA) at 2.8%, your money must grow just to maintain its purchasing power.

Currently, the national average interest rate for a traditional savings account hovers around a meager 0.6%. Meanwhile, high-yield savings accounts (HYSAs) offered by online banks routinely pay between 4.0% and 5.8% Annual Percentage Yield (APY). When you settle for the national average, you lose money to inflation every single month. Consider the math on a conservative emergency fund:

| Account Type | Average Annual Yield (APY) | Annual Interest on $50,000 |

|---|---|---|

| Traditional Brick-and-Mortar Savings | 0.60% | $300 |

| High-Yield Online Savings Account | 4.50% | $2,250 |

| 12-Month Certificate of Deposit (CD) | 4.75% | $2,375 |

Moving your emergency funds from a legacy bank to an FDIC-insured high-yield account requires about fifteen minutes of effort. That simple administrative task instantly plugs a leak worth nearly $2,000 a year on a $50,000 balance.

“The miracle of compounding returns is overwhelmed by the tyranny of compounding costs.” — John Bogle, Founder of The Vanguard Group

While Bogle primarily referred to investment fees, the exact same principle applies to opportunity costs. By accepting negligible banking yields, you actively compound your losses against inflation.

3. You Overlook the Latest Senior Tax Deductions

Tax laws change rapidly, and relying on outdated advice causes significant budget leakage. If you blindly claim the same deductions you used a decade ago, you almost certainly overpay the IRS.

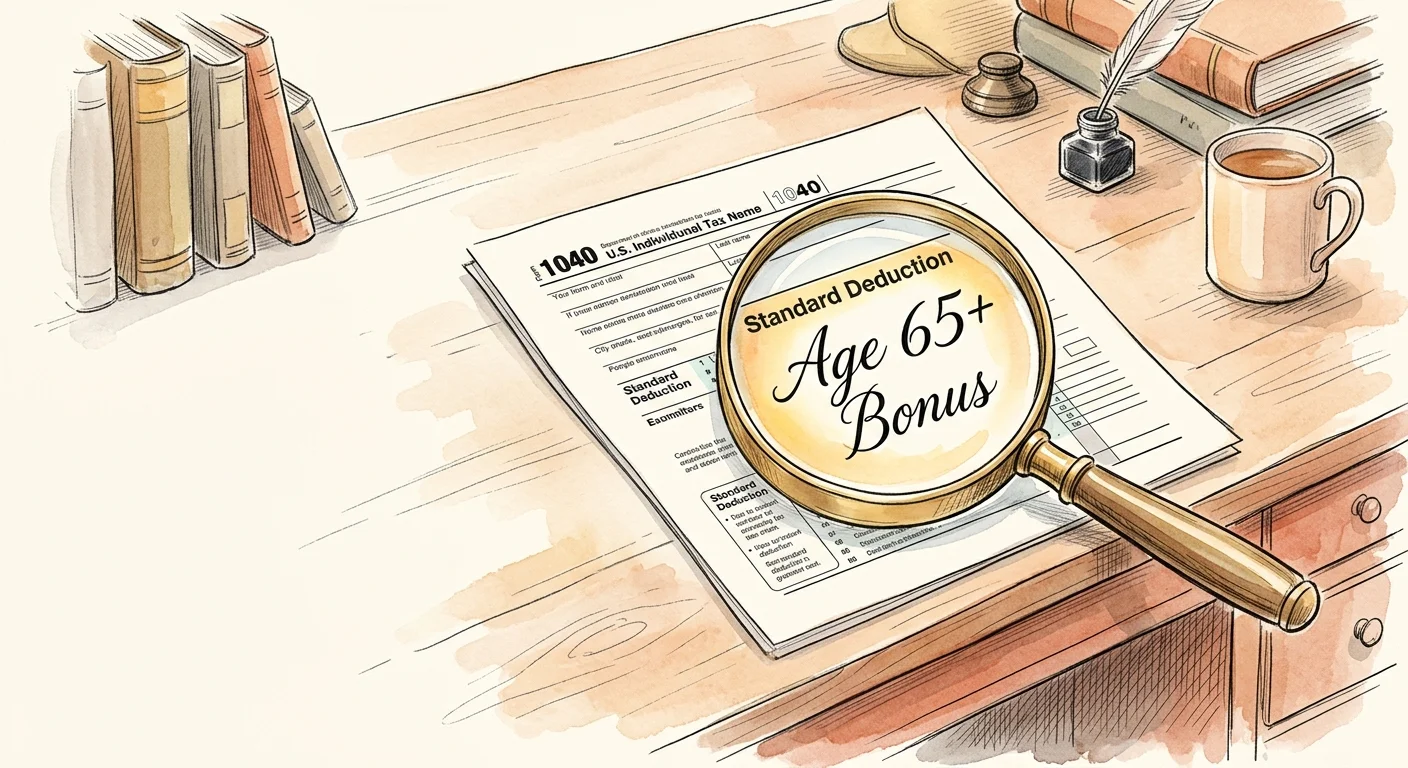

For the 2026 tax year, the IRS implemented dramatic updates to the standard deduction, driven by new federal legislation. Most notably, a recent tax package introduced a temporary $6,000 bonus deduction specifically for taxpayers age 65 and older. When you combine this new bonus with the base standard deduction and the traditional age-based additional deduction, the tax shelter becomes massive.

| Deduction Component | 2026 Amount (Single Filer Over 65) |

|---|---|

| Base Standard Deduction | $16,100 |

| Age 65+ Additional Deduction | $2,050 |

| New Senior Bonus Deduction | $6,000 |

| Total Standard Deduction | $24,150 |

Married couples filing jointly can shelter even more income if both spouses are 65 or older and meet the eligibility requirements. You lose money every month if you over-withhold taxes based on outdated standard deductions. Review your W-4V (for Social Security withholding) or your estimated quarterly tax payments. If your total deductions have increased, you can reduce your withholdings and keep more cash in your monthly budget. Always consult the official Internal Revenue Service website or a certified tax professional to ensure you maximize these new thresholds.

4. Subscriptions and Telecom Bills Are Quietly Draining Your Budget

Convenience often breeds complacency. Subscription services and telecommunication bills rely on auto-pay features to prevent you from scrutinizing the monthly cost.

Let’s start with your smartphone. Recent data indicates the average monthly cell phone bill for a single line is roughly $141. If you pay this rate, you are leaking money. Major networks lease their towers to Mobile Virtual Network Operators (MVNOs). These alternative companies provide the exact same cellular coverage for a fraction of the cost—often $15 to $35 per month. Switching your provider patches a leak of over $1,200 per year.

Beyond your phone bill, evaluate your digital subscriptions. Streaming services regularly hike their prices by $2 or $3 at a time. A $10 monthly subscription quietly becomes a $19 charge. Implement a strategy known as “subscription hopping.” You do not need multiple premium streaming platforms active simultaneously. Subscribe to one service, watch the shows you want, cancel it, and rotate to the next.

Conduct a quarterly audit of your credit card and bank statements. Look for unused gym memberships, premium app subscriptions, magazine deliveries, and cable packages filled with channels you never watch. Cancel anything that does not bring you direct, tangible value.

5. You Serve as the Default “Bank of Mom and Dad”

One of the most emotionally complex budget leaks involves financially supporting adult children. Retirees frequently cover cell phone bills, car insurance, streaming accounts, or even rent for their grown kids. While generosity is a virtue, jeopardizing your own financial security creates a massive problem for both you and your children down the road.

“You can get a loan for college, but you cannot get a loan for retirement.” — Suze Orman, Personal Finance Expert

If you drain your nest egg to subsidize your children’s lifestyle, you risk running out of money and becoming a financial burden to them later in life. To plug this leak, you must set firm boundaries. Track exactly how much money flows out of your accounts to family members each month. If the number shocks you, initiate an honest conversation.

Transition expenses back to your children gradually. Give them a three-month warning that you will remove them from your auto insurance policy or family phone plan. Provide them with guidance on budgeting rather than handing over cash. Your ultimate goal is to foster their financial independence while protecting your own retirement income.

6. Your Insurance Policies Are Running on Autopilot

Insurance companies penalize loyalty. If you renew your auto and homeowners insurance policies automatically every year without checking the market, you suffer from price optimization. Insurers use algorithms to identify customers who are unlikely to shop around, slowly raising their premiums year after year.

Home and auto insurance rates have surged significantly over the last few years due to inflation, vehicle repair costs, and extreme weather events. You counter these increases by comparison shopping. Commit to securing three new insurance quotes every two years. Work with an independent insurance broker who can check multiple carriers simultaneously to find you the best rate for your specific needs.

You can also plug insurance leaks by modifying your coverage. If you drive an older vehicle worth less than $4,000, reconsider carrying comprehensive and collision coverage. The premiums you pay may outweigh the potential payout. Additionally, look into raising your deductibles. Increasing an auto insurance deductible from $500 to $1,000 can drastically lower your monthly premium. Since you have properly patched your savings leak and hold emergency funds in a high-yield account, you can comfortably cover the higher deductible if an accident occurs.

Avoiding Common Errors

When hunting for budget leaks, retirees often make a few predictable missteps. Avoid these common errors to ensure your cost-cutting efforts actually improve your financial standing.

- Fixating on pennies while losing dollars: Do not agonize over a $3 cup of coffee while ignoring a $2,000 tax inefficiency. Prioritize large, recurring leaks—like insurance premiums, high-interest debt, and low-yield savings—before worrying about minor discretionary spending.

- Falling for “free” trials: Many seniors sign up for trial services, fully intending to cancel before the billing cycle begins. Companies count on you forgetting. If you must use a free trial, set a calendar alarm on your phone for two days before the renewal date.

- Ignoring your credit report: Identity theft and fraudulent accounts create devastating invisible leaks. Pull your free annual credit report via resources recommended by the Consumer Financial Protection Bureau (CFPB) to ensure no unauthorized accounts are draining your resources or damaging your score.

- Cutting necessary healthcare: Trimming the fat from your budget never means skipping medications, avoiding doctor visits, or dropping necessary supplemental health coverage. Health is wealth; ignoring medical needs ultimately leads to catastrophic financial emergencies.

When DIY Isn’t Enough

Finding and fixing everyday budget leaks is entirely manageable on your own. However, larger structural leaks require a professional touch. You should consider hiring a fee-only fiduciary financial advisor or a Certified Public Accountant (CPA) when you encounter the following scenarios:

- You approach IRMAA thresholds: If your income fluctuates due to capital gains, property sales, or large IRA withdrawals, a professional can construct a withdrawal strategy that keeps your Medicare premiums in check.

- You need advanced tax planning: The new 2026 tax regulations carry specific phase-outs and income limits. A CPA ensures you maximize these deductions without triggering audits.

- You manage significant inheritance or asset transfers: If you plan to gift money to heirs or transfer real estate, improper structuring triggers massive tax liabilities. Professionals help you utilize annual exclusion gifts and trusts to protect your wealth.

- Your portfolio needs rebalancing: If your investments drift far from your target asset allocation, you expose yourself to unnecessary risk. An advisor can help you rebalance efficiently while minimizing capital gains taxes.

Reclaiming your monthly cash flow is not about depriving yourself; it is about efficiency. By optimizing your healthcare costs, securing higher yields on your cash, leveraging new tax deductions, and cutting unnecessary subscriptions, you give yourself a raise. Take one hour this weekend to audit your bank statements and apply these strategies. The money you save today provides the peace of mind you deserve tomorrow. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: July 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.