Retiring to the countryside is no longer just a romantic dream—it has become a strategic financial decision for millions of older Americans. As rising costs squeeze fixed incomes in major cities, seniors are trading urban gridlock and skyrocketing property taxes for open spaces and genuine affordability. In 2026, maximizing your retirement income is essential, and moving away from metropolitan centers offers immediate financial breathing room. From expanded Medicare telehealth access that brings top specialists into your living room to dramatic reductions in daily living expenses, the appeal of small-town living has never been stronger. Here are twelve reasons why trading the city skyline for the rural tree line might be your smartest retirement move.

1. Unbeatable Housing Affordability

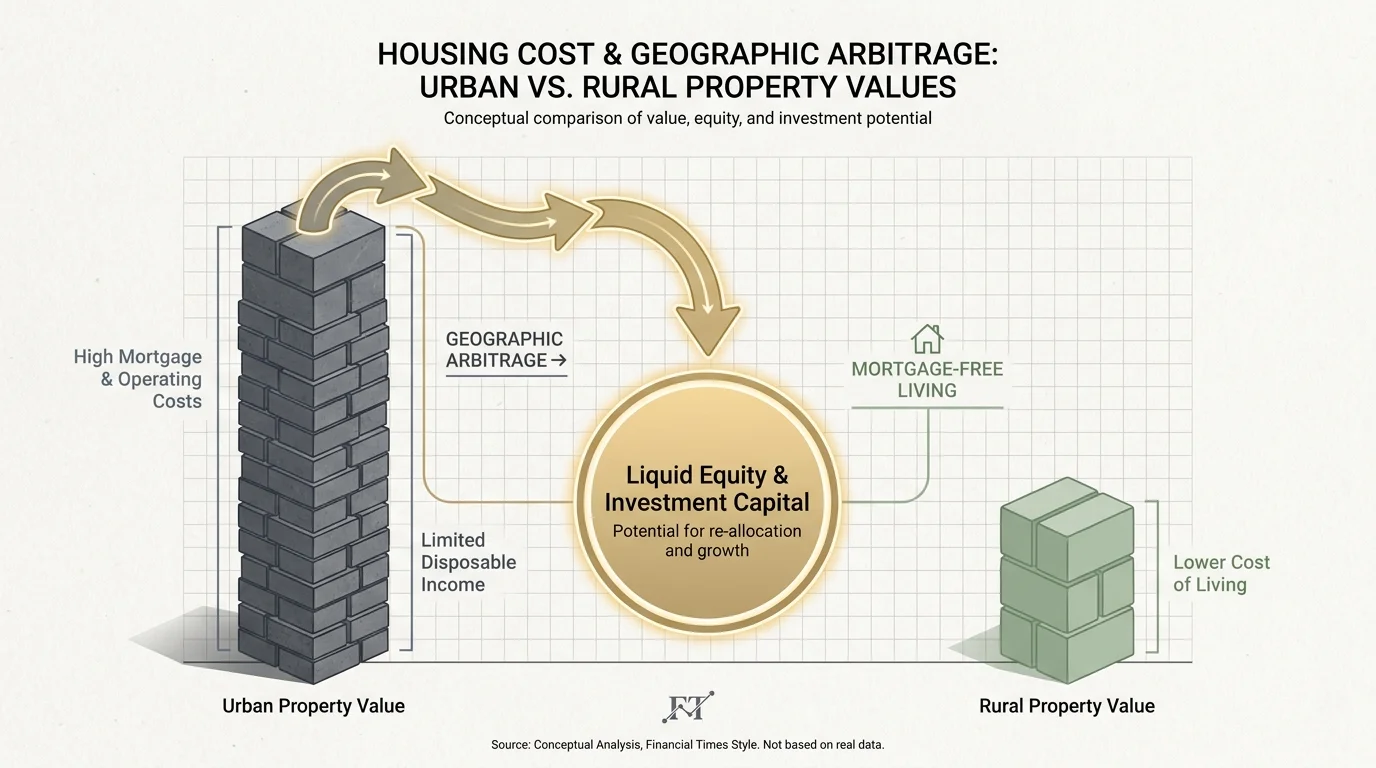

If you live in a major metropolitan area or a densely populated suburb, your home likely serves as your largest single financial asset. Selling a high-value urban property and relocating to a rural county empowers you to practice geographic arbitrage. You can frequently purchase a comfortable, single-story home in the countryside for a fraction of your current property’s market value. By avoiding a new mortgage, you eliminate your largest monthly expense. You can then redirect your leftover equity into your investment accounts to generate additional income. Instead of watching your wealth remain tied up in urban real estate, rural housing prices allow you to buy your new property outright and keep your remaining capital highly liquid.

2. Stretching Your Social Security Income Further

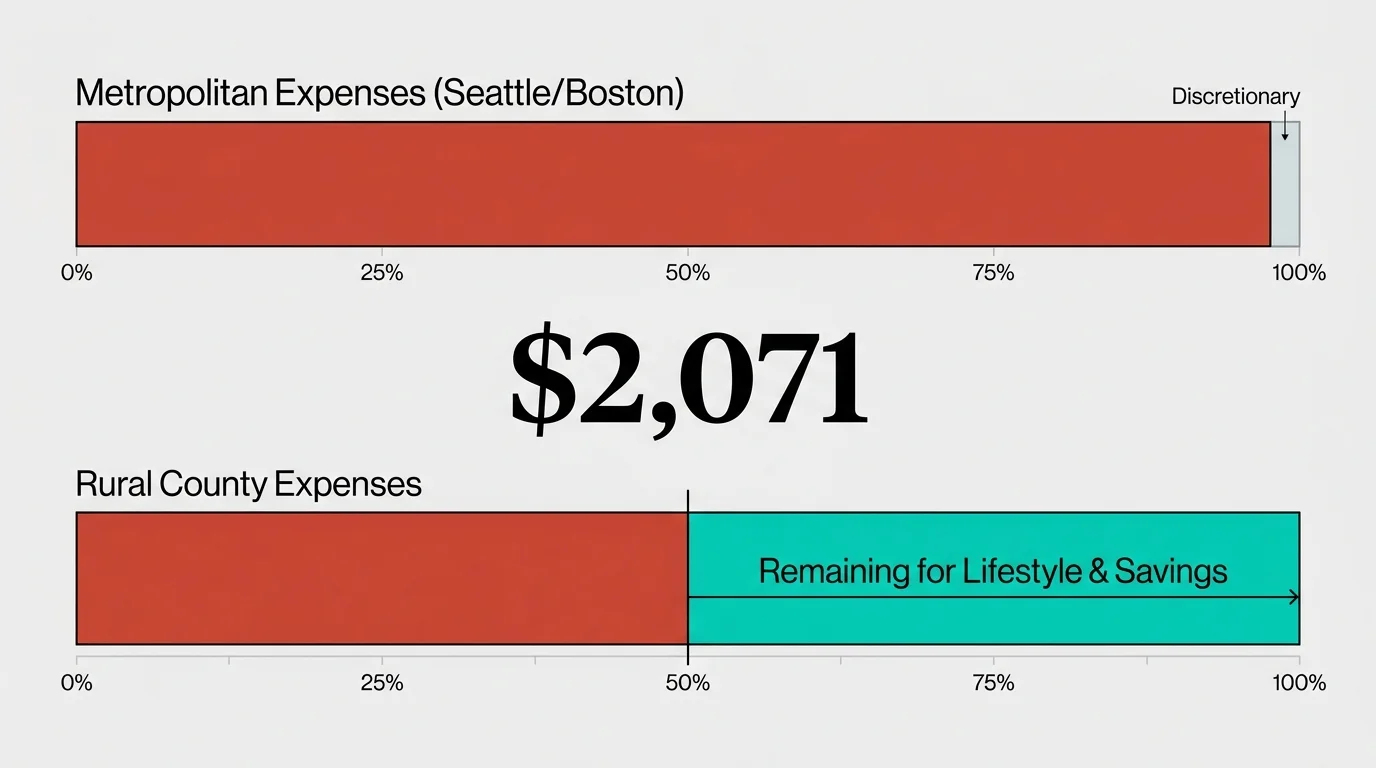

Living on a fixed income requires meticulous budgeting, especially when inflation drives up the cost of everyday necessities. Following the 2026 cost-of-living adjustment, the Social Security Administration reports that the average monthly benefit for retired workers sits at approximately $2,071. In cities like Seattle or Boston, that entire check might barely cover an apartment rental and basic utilities. However, in a rural area, a $2,071 monthly benefit goes significantly further. Lower housing costs, cheaper utilities, and reduced local taxes transform your Social Security check from a mere supplemental payment into a robust foundation that covers your actual baseline expenses.

“Retirement is not an age; it’s a financial number.” — Dave Ramsey, Personal Finance Expert

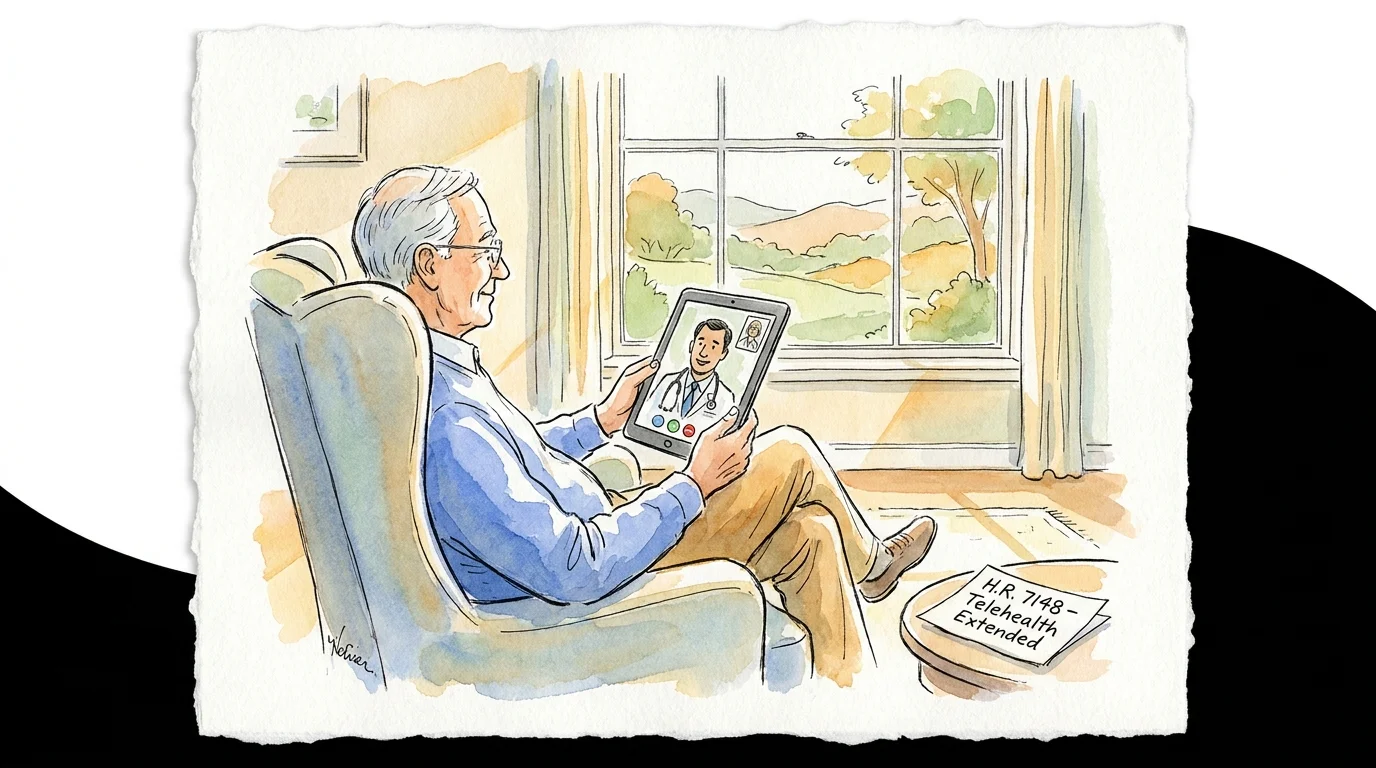

3. Expanded Medicare Telehealth Access

Historically, the biggest hesitation surrounding rural retirement centered on healthcare access. Retirees rightly worried about the logistical challenge of reaching specialists. Fortunately, the virtual healthcare revolution has permanently shifted the landscape. In February 2026, the federal government resolved the looming telehealth cliff by passing H.R. 7148, which officially extended expanded Medicare telehealth flexibilities through December 31, 2027. This critical legislation ensures that the strict “rural-only” facility requirements remain waived. You can now consult with top-tier specialists, physical therapists, and mental health professionals directly from your living room. You no longer have to reside within ten miles of a major hospital to receive excellent, routine care. You can verify current telehealth coverage specifics at Medicare.gov.

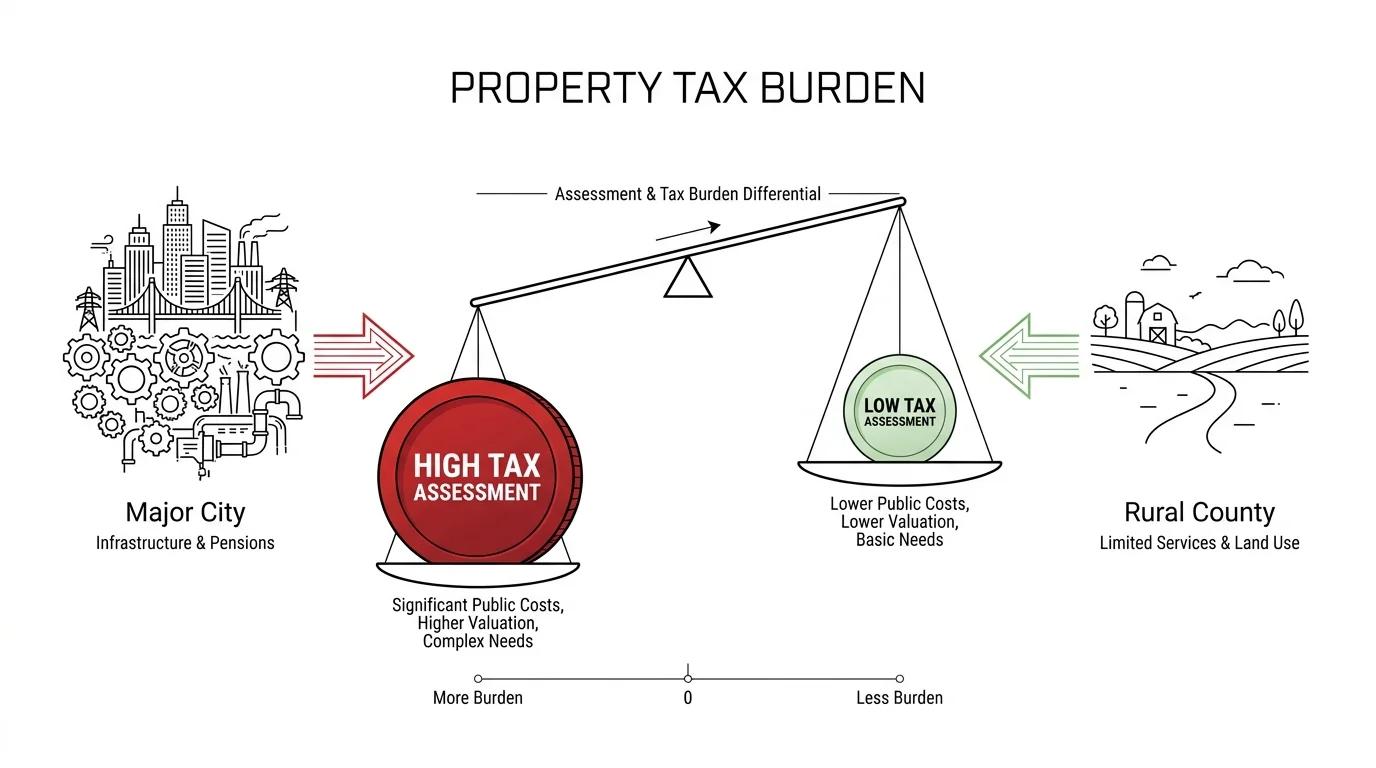

4. Dramatically Lower Property Taxes

Property taxes act as the silent killer of many retirement budgets. While you can pay off your mortgage, you can never outlive property tax assessments. Sprawling cities require massive infrastructure projects, vast public transportation networks, and complex municipal pensions, all of which drive up your annual tax bill. Rural counties generally operate on significantly leaner budgets and feature much lower assessed property values. This combination results in a fraction of the tax burden, allowing you to keep thousands of dollars in your pocket every single year.

| Expense Category | Typical Metropolitan Area | Typical Rural Area |

|---|---|---|

| Median Home Price | High (Often exceeding $450,000) | Low (Often available under $250,000) |

| Property Taxes | High (Funding massive city infrastructure) | Low (Funding basic county services) |

| Auto Insurance | High (Heavy traffic and frequent claims) | Low (Fewer accidents and thefts) |

| Entertainment | Expensive (Premium restaurants, shows) | Affordable (Nature trails, community events) |

5. Reduced Daily Living Expenses

When you relocate to a smaller town, you naturally spend less on everyday consumer items. Auto insurance premiums typically plunge due to reduced traffic density and vastly lower theft rates. You spend less on premium services, and local labor rates for mechanics, plumbers, and home repair professionals are generally much friendlier than their city counterparts. Even your entertainment budget shrinks organically, as rural living naturally emphasizes affordable outdoor activities over expensive dining and costly theater tickets.

6. A Tighter, More Supportive Community

In sprawling cities, it is remarkably easy to feel isolated despite living surrounded by millions of people. Rural towns offer an entirely different social dynamic. Communities operate on a smaller scale, and neighbors genuinely rely on one another. Whether you decide to join a local church group, assist the volunteer fire department, or serve on a small town library board, you will find it incredibly easy to integrate and build meaningful relationships. Strong social ties remain a critical component of healthy aging, helping to stave off cognitive decline and combat loneliness.

7. Immediate Access to Nature and Better Health

Rural areas provide inherent opportunities to stay active and healthy. Instead of paying a premium for a crowded gym membership, your daily routine might involve tending a garden, walking local woodland trails, or fishing at a nearby lake. This constant access to open green space actively lowers stress hormones, reduces resting blood pressure, and encourages a naturally active lifestyle that promotes cardiovascular health.

8. Lower Crime Rates and Increased Safety

Physical safety and peace of mind stand as top priorities for older adults. Statistically, rural counties report significantly lower rates of violent crime and property theft compared to metropolitan hubs. This increased safety provides invaluable comfort. You can enjoy evening walks through your neighborhood, leave your windows open during the summer, and feel entirely secure in your own home without investing in complex urban security systems.

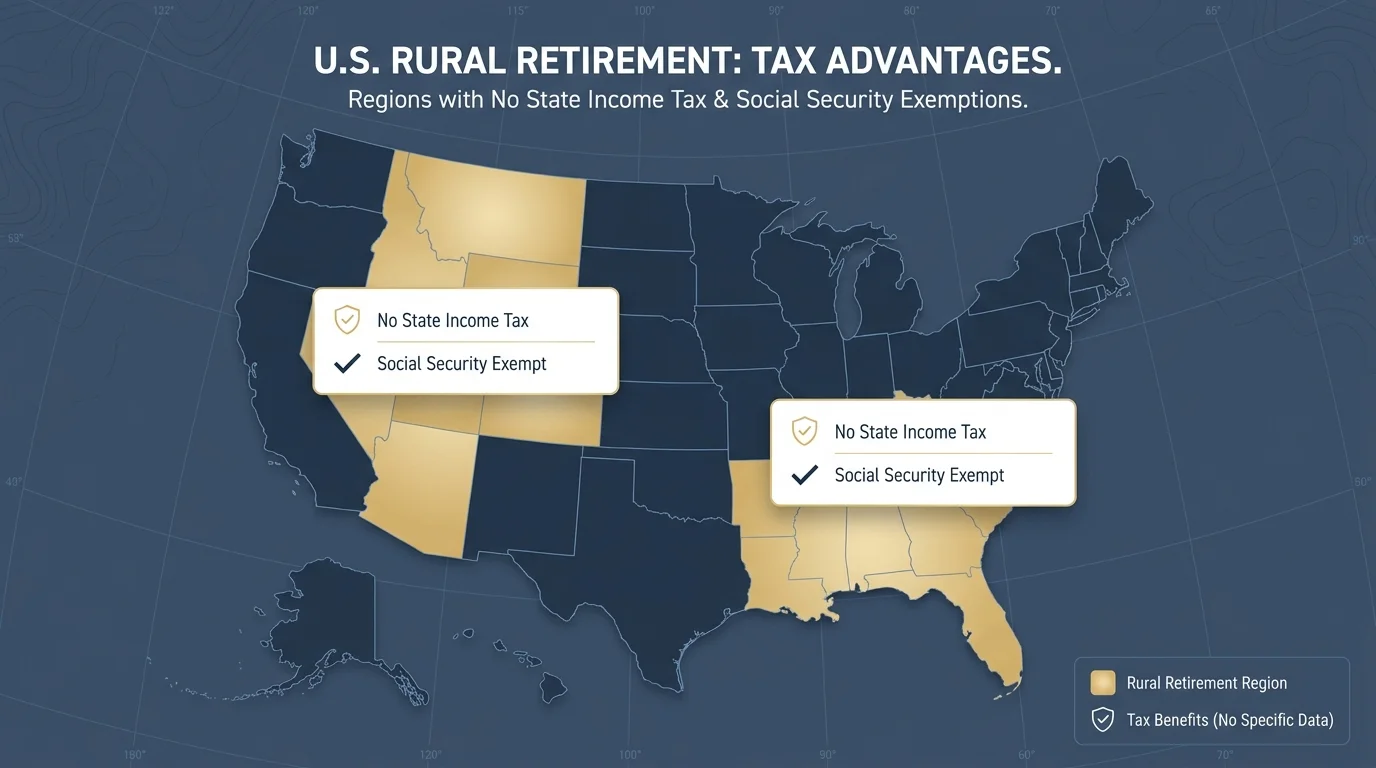

9. Tax-Friendly State Options

Many of the most beautiful rural landscapes across America sit squarely inside incredibly tax-friendly states. Wyoming, South Dakota, Nevada, and Tennessee offer stunning countryside living combined with zero state income tax. Moving to these states ensures your Social Security benefits, IRA withdrawals, and pension payouts remain fully yours. You can model how different state tax rates impact your withdrawal strategies using the free tools available at Investor.gov.

“Resilience isn’t just about bouncing back; it’s about moving forward and making proactive choices with your money.” — Jean Chatzky, Financial Editor

10. Less Traffic and Transportation Stress

Navigating city traffic becomes increasingly stressful and dangerous as our eyesight and reflexes change with age. Gridlock, aggressive drivers, and complex multi-lane highway systems take a daily toll on your nerves. Rural living offers quiet, scenic roads. Running weekly errands transforms from a stressful chore into a pleasant drive, completely removing the friction of daily urban transportation.

11. Fewer Zoning Restrictions for Retirement Projects

City zoning boards and strict Homeowner Associations (HOAs) often dictate exactly what you can and cannot do with your property. In the city, building an accessory dwelling unit (ADU) for visiting grandchildren or erecting a detached woodworking shop takes years of permits and thousands of dollars in fees. Rural properties generally grant you much more freedom. You can easily build a greenhouse, park a luxury RV in your driveway, or customize your acreage to fit your exact retirement vision. If you plan to buy rural land to develop, the Department of Housing (HUD) provides excellent guidance on rural housing loans and property standards.

12. Opportunities for “Encore” Pursuits and Hobby Farming

Retirement does not mean you stop working entirely; it simply means you stop working for someone else. Rural living provides the physical space and the operational freedom to pursue passions that are completely impossible in an apartment. You can start a massive vegetable garden, raise backyard chickens, sell handmade crafts at local farmers’ markets, or offer consulting services to small local businesses. These “encore” pursuits provide mental stimulation and often generate a modest supplemental income.

Common Mistakes to Avoid When Retiring to a Small Town

- Buying Before Renting: Rural life moves at a different pace, and the everyday reality of a town might differ drastically from your vacation memories. Rent a home for six months to experience the off-season weather and daily lifestyle before committing your hard-earned equity. Organizations like AARP offer livability indexes that can help you evaluate a town’s long-term suitability.

- Ignoring Infrastructure Realities: City dwellers take municipal water and sewer lines for granted. Rural homes frequently rely on private wells and independent septic systems. These systems require routine maintenance and significant repair budgets. Additionally, you must verify broadband internet availability before buying, especially if you plan to rely on streaming entertainment or telehealth services.

- Underestimating Travel Distances: Moving away from major metropolitan hubs inherently means moving away from large international airports. Factor in the additional drive time, parking logistics, and potential connecting flights when you plan your visits to grandchildren or schedule major international travel.

Choosing where to spend your retirement years requires balancing your financial realities with your lifestyle goals. By carefully researching your chosen destination and understanding the local housing market, you can secure a peaceful, affordable, and deeply fulfilling rural retirement.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.