Getting married later in life requires protecting the retirement nest egg you spent decades building. Modern prenuptial agreements have evolved far beyond the simple division of property, offering creative solutions for the unique financial complexities of older couples. With the divorce rate among adults 50 and older roughly quadrupling over the past three decades, a comprehensive relationship agreement is essential financial armor. Retirees are now using prenups to safeguard adult children’s inheritances, firewall against unexpected medical debts, and even outline future caregiving expectations. From navigating strict federal retirement laws to planning for long-term care, these customized legal provisions ensure both partners enter their new marriage with total financial clarity and confidence.

Why Modern Retirees Are Rethinking Prenups

If you are getting married in your 60s or 70s, you bring a lifetime of financial history to the altar. You likely have built significant home equity, accumulated funds in a 401(k) or IRA, and established an estate plan designed to care for children from a previous marriage. Blending these established financial lives requires precision—something a standard marriage contract simply does not provide.

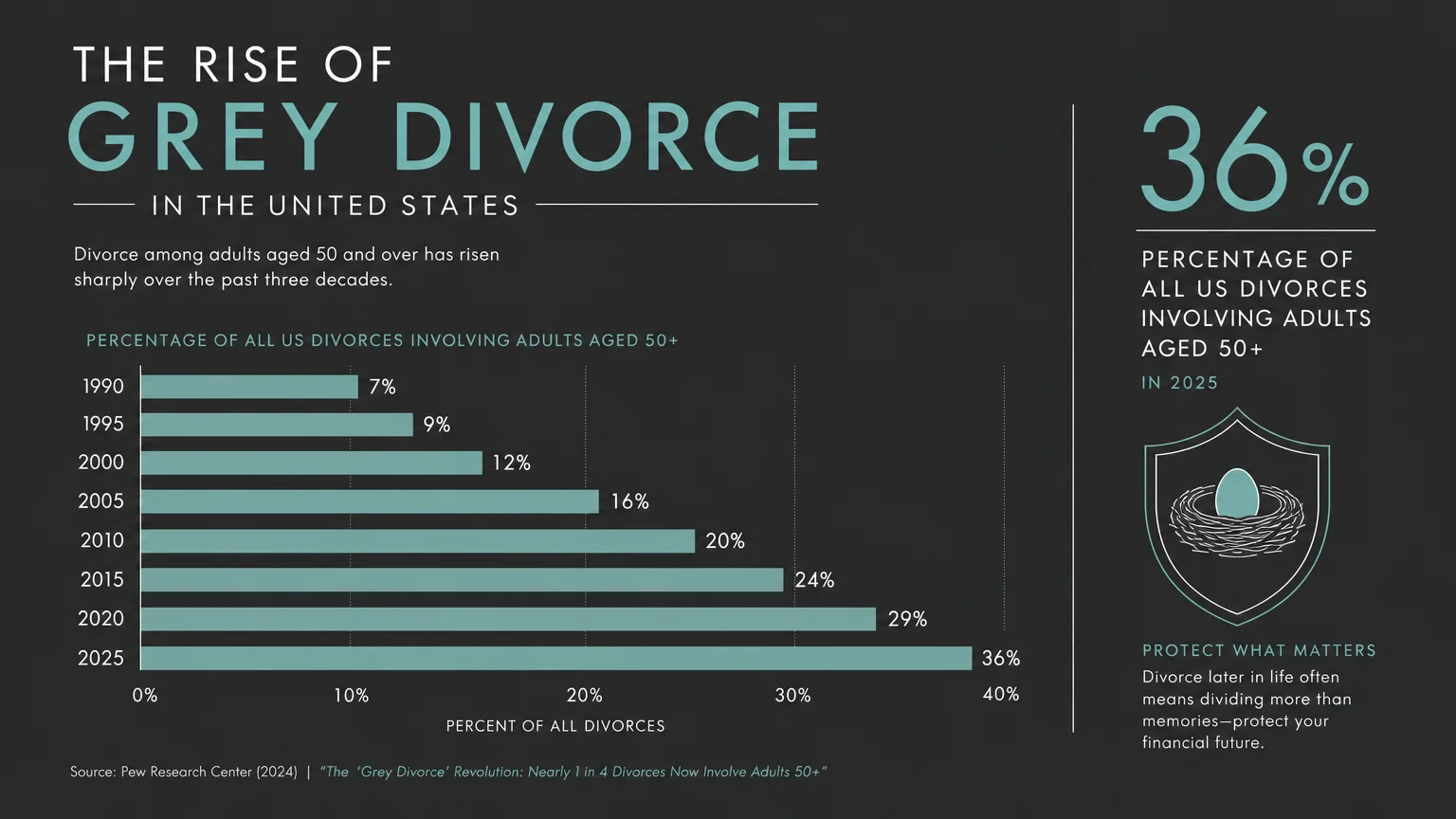

The concept of “grey divorce”—couples splitting up later in life—has changed how older adults approach remarriage. According to 2024 and 2025 demographic data, adults aged 50 and older now account for roughly 36% of all divorces in the United States. Because older adults have less time to recover financially from a sudden division of assets, a prenuptial agreement acts as an essential safety net.

“Hope is not a financial plan. The time to plan is not when you’re in a state of hate.” — Suze Orman, Personal Finance Expert

Modern prenups are no longer just for the ultra-wealthy. They are practical tools for everyday retirees who want to set clear financial expectations. Rather than serving as a pessimistic prediction of divorce, these contracts foster deep financial transparency. Couples are drafting surprisingly specific clauses to navigate complex federal laws, healthcare realities, and family dynamics.

1. The Post-Wedding ERISA Waiver Promise

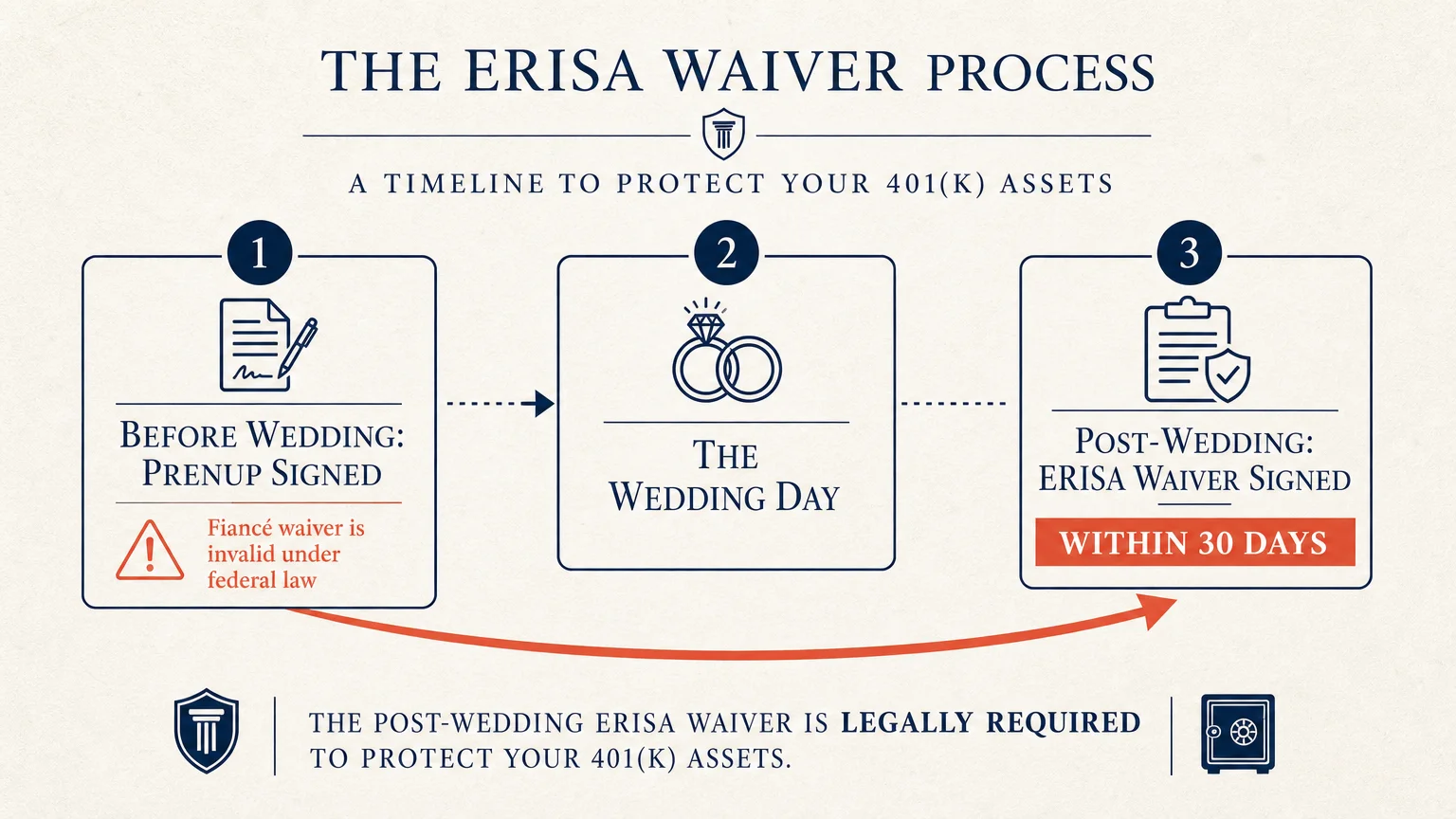

Many couples mistakenly believe a prenup can automatically shield their 401(k) from their new spouse. However, employer-sponsored retirement plans are governed by federal law—specifically the Employee Retirement Income Security Act (ERISA). Under ERISA rules, your spouse is legally entitled to be the primary beneficiary of your 401(k).

The trap? A fiancé or fiancée is not yet a “spouse” under the law. If your partner signs a prenup waiving their right to your 401(k) before the wedding, that waiver is completely legally invalid under federal law.

To fix this, lawyers now include a “Post-Wedding ERISA Waiver Promise.” This clause requires the new spouse to officially sign the plan’s spousal waiver form after the wedding takes place—usually within a strict timeframe, such as 30 days. If the spouse refuses to sign the federal waiver after the marriage, this prenup clause allows you to seek a court order enforcing the original contract.

2. The Medical Debt and Long-Term Care Firewall

Healthcare is one of the most unpredictable expenses in retirement. While the standard Medicare Part B premium is $202.90 per month in 2026, Medicare does not cover the astronomical costs of custodial long-term care. According to the Genworth/CareScout Cost of Care Survey, the median cost for a private room in a nursing home now exceeds $127,000 annually.

If one spouse develops a prolonged illness, those costs can quickly decimate the couple’s combined life savings. To prevent this, retirees are utilizing “firewall” clauses. These provisions specifically dictate that one spouse’s medical debts and long-term care expenses must be paid exclusively from their separate property, protecting the healthy spouse’s retirement accounts from being drained by healthcare facilities.

Note: While a prenup can protect against private medical debt and civil creditors, navigating federal Medicaid rules requires separate legal strategies. Medicaid looks at the combined assets of a married couple regardless of a prenup, making consulting an elder law attorney critical.

3. The Adult Children Inheritance Guarantee

A primary fear for widows, widowers, and divorced retirees getting remarried is accidentally disinheriting their children. State laws often grant a surviving spouse an “elective share”—a mandatory percentage of the deceased spouse’s estate, typically ranging from one-third to one-half.

If you intend to leave your family home or a specific brokerage account to your adult children, an elective share law could force the sale of that property to pay your new spouse. The “Inheritance Guarantee” clause solves this by having both partners formally waive their right to the elective share. It allows you to synchronize your prenup with your will and living trust, ensuring your specific assets flow exactly where you intend them to go.

4. The Social Security Offset Clause

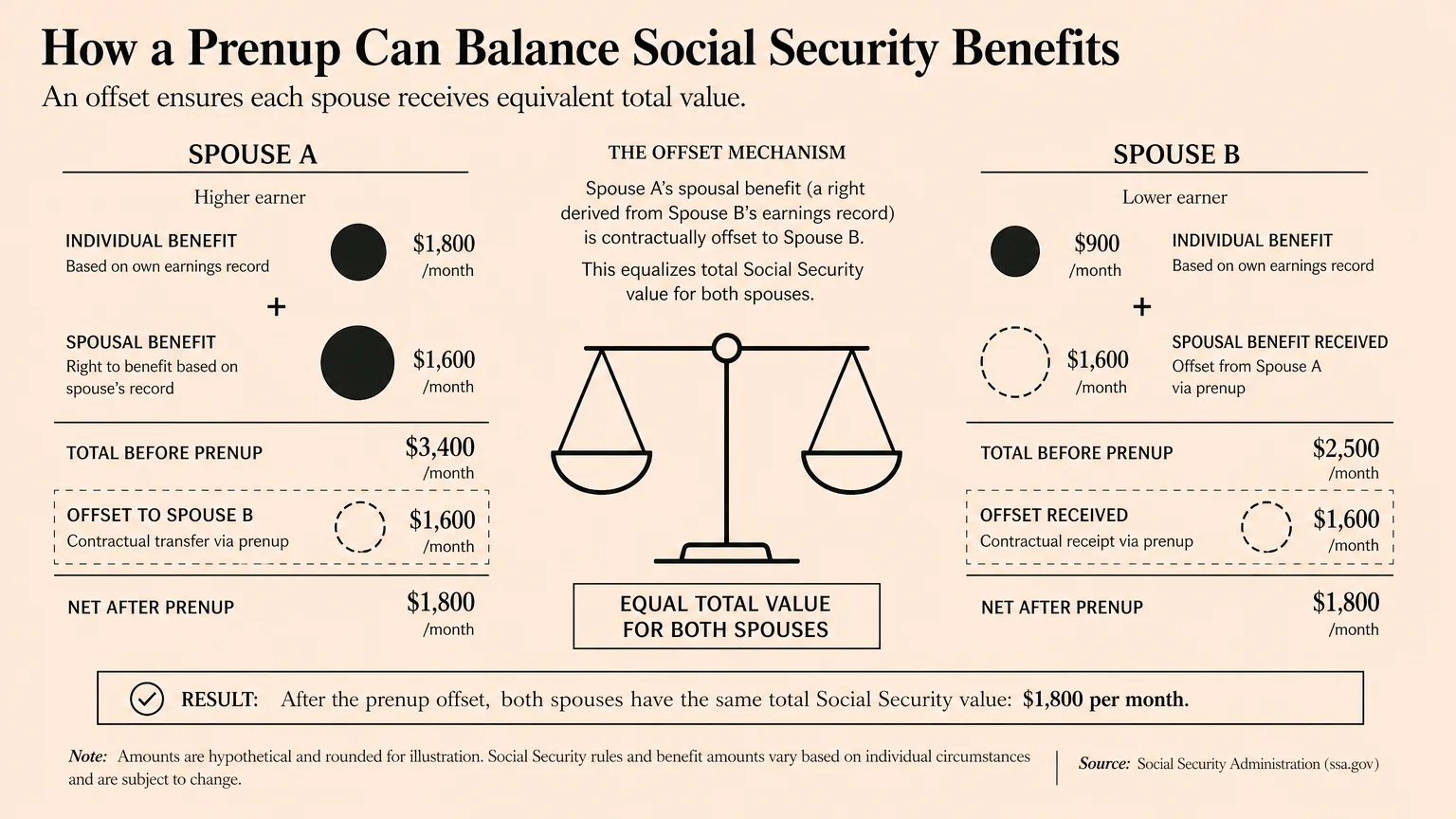

Social Security benefits create a unique challenge in late-in-life marriages. If you are married for at least 10 years and then divorce, an ex-spouse may be entitled to claim a benefit based on your earnings record. Importantly, federal law strictly prohibits you from forcing a spouse to waive their right to Social Security spousal or survivor benefits in a state-level prenuptial agreement.

Because you cannot legally sign away Social Security rights, clever attorneys use an “Offset Clause.” This provision acknowledges that federal law reigns supreme, but stipulates that if a spouse eventually claims Social Security benefits on the other’s record, their share of the other marital assets will be reduced by an equivalent dollar amount. This creative workaround protects the higher earner’s overall estate value without violating federal regulations.

5. The Dementia and Caregiving Limit Clause

As life expectancies increase, the reality of cognitive decline—such as Alzheimer’s or dementia—becomes a pressing concern. Caregiving is an immense physical and emotional burden that can destroy the health of the caregiver spouse. Modern retirees are addressing this head-on with “Caregiving Limit” clauses.

These surprising but deeply practical provisions outline exactly what happens if one spouse loses cognitive or physical function. The clause might stipulate that marital funds—or a specific separate trust—will be unlocked to hire professional in-home aides or pay for a memory care facility. By documenting this agreement while both partners are healthy, it removes the guilt from the healthy spouse and legally prevents them from being forced into a grueling, 24/7 caregiving role.

6. The Pet Custody and Veterinary Care Agreement

Pets are increasingly viewed as family members, and older couples often adopt pets together to enjoy during their retirement years. Standard property laws treat pets as personal property—no different than a television or a sofa. If the marriage dissolves, the emotional toll of fighting over a beloved dog or cat can be devastating.

To avoid this, couples are drafting detailed pet clauses. These agreements define exactly who gets custody of the pet if the marriage ends. Even more surprisingly, they outline who will pay for the animal’s ongoing expenses, including expensive late-in-life veterinary surgeries, daily medications, and premium food. Clarifying these emotional details upfront saves immense heartache later.

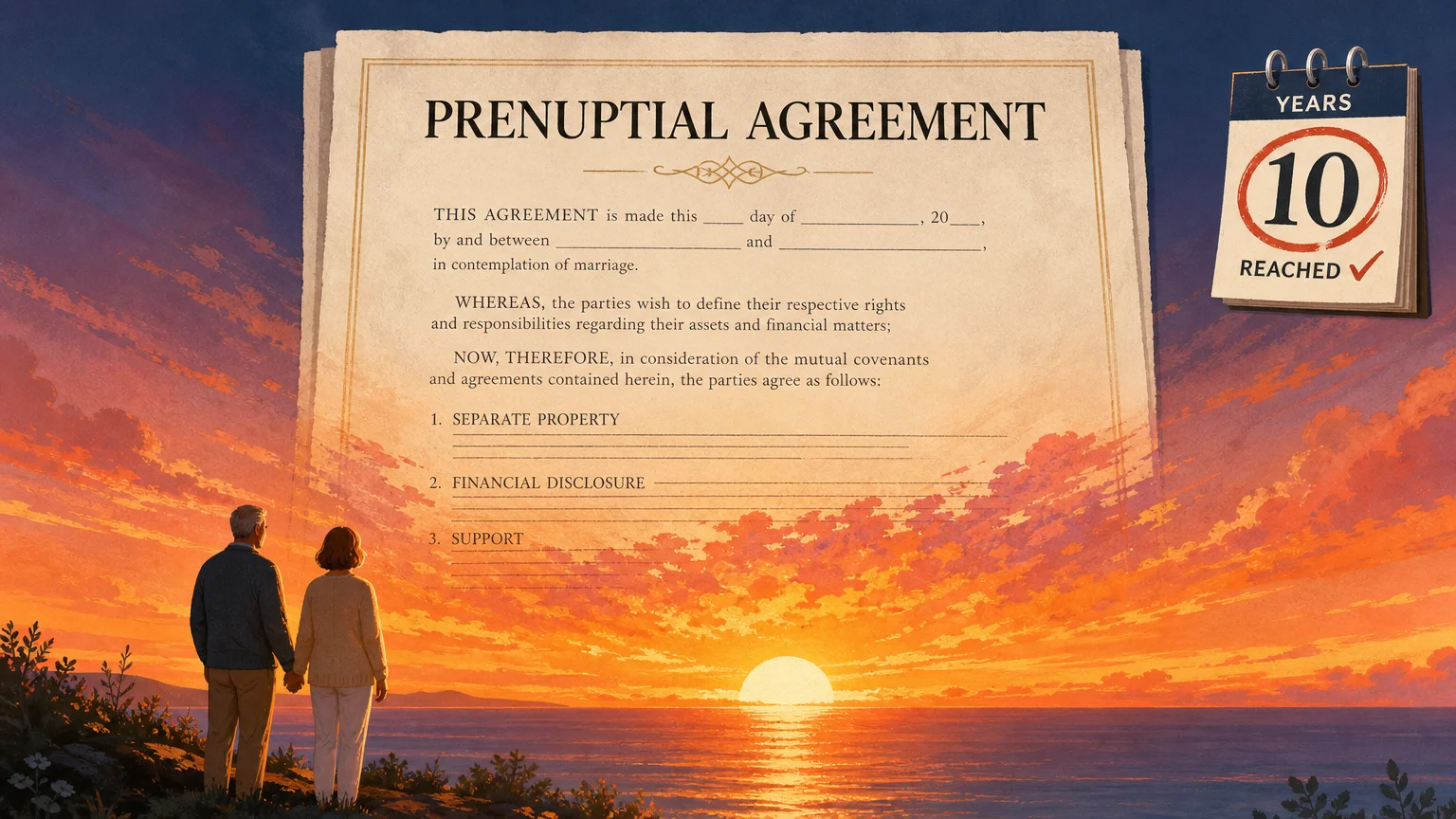

7. The “Sunset” Provision

Not every prenup is designed to last forever. A “Sunset Provision” dictates that the prenuptial agreement will expire completely, or phase out gradually, after a specific milestone—usually 10, 15, or 20 years of marriage.

For retirees, a sunset clause is a romantic but pragmatic compromise. It acknowledges the need to protect assets during the vulnerable early years of a blended marriage. However, it also recognizes that if the marriage lasts into deep old age, the couple’s lives, caregiving responsibilities, and finances will naturally become entirely intertwined. Some couples use a phased sunset, where an additional 10% of separate property converts into marital property for every year they remain married.

Common Mistakes to Avoid with Late-in-Life Prenups

Drafting a prenup as a retiree involves navigating complex federal tax laws and retirement regulations. Avoid these common pitfalls to ensure your agreement holds up in court:

- Forgetting to Update Beneficiary Forms: A prenup is just a contract; it does not automatically change the beneficiary designations on your life insurance or IRAs. You must manually update your forms with your financial institution to reflect the terms of the prenup.

- Ignoring the Standard Deduction and Taxes: How you file taxes affects your bottom line. For example, in 2026, the standard deduction for a single filer is $16,100, while married couples filing jointly receive $32,200. If your prenup forces you to file “Married Filing Separately,” you could lose lucrative tax advantages and senior bonus deductions. Make sure your tax professional reviews the agreement.

- Springing the Document at the Last Minute: Courts look unfavorably upon prenups signed under duress. Presenting a legal document to your partner a week before the wedding makes it highly susceptible to being thrown out by a judge. Begin the process at least three to six months in advance.

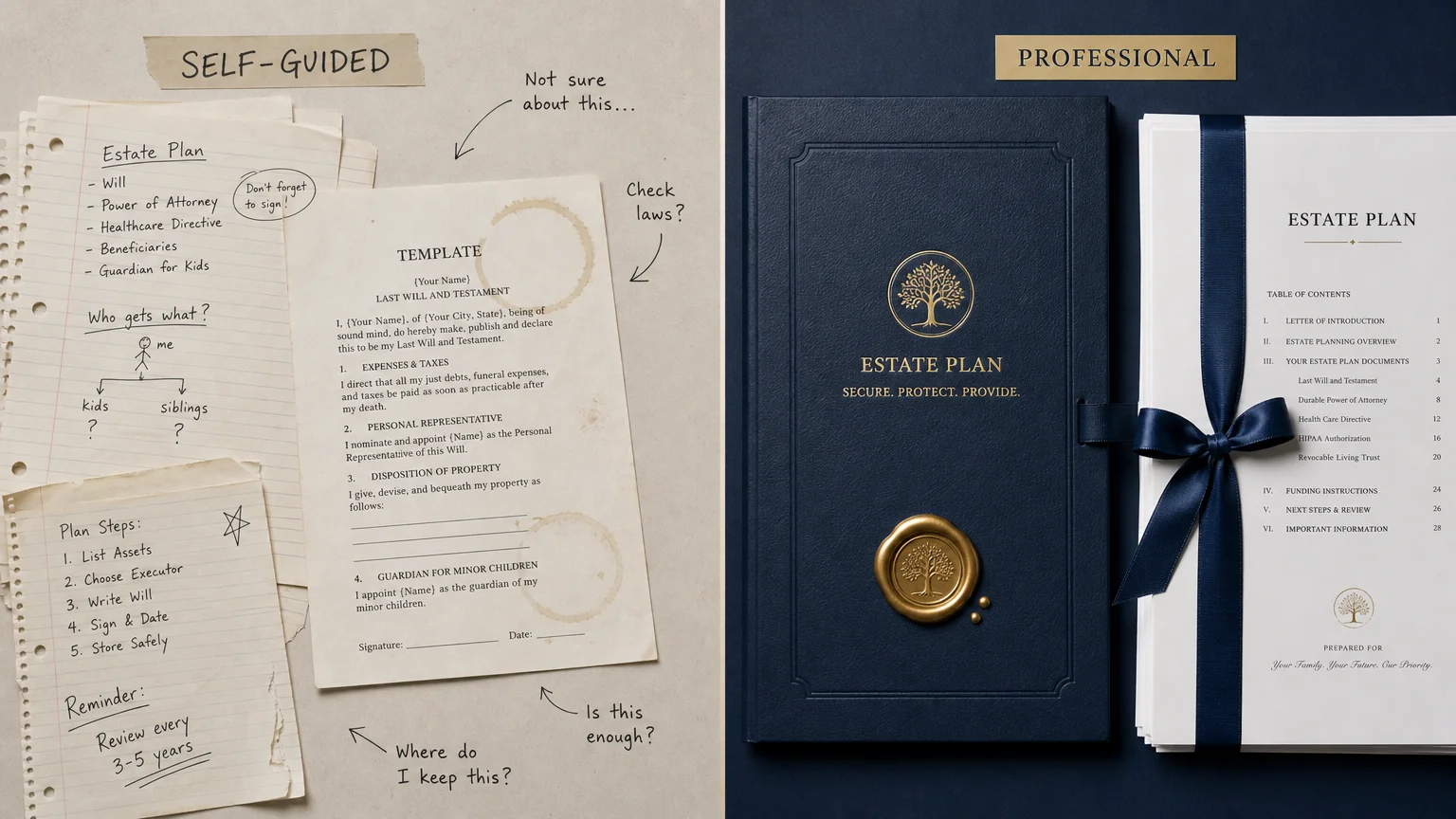

Professional vs. Self-Guided Prenuptial Agreements

While DIY legal templates are easily accessible online, relying on a self-guided prenup for a late-in-life marriage is incredibly risky. The interplay between state property laws, federal ERISA regulations, and estate planning requires specialized knowledge.

When is it safe to use an online service? If you are young, entering a first marriage, and have virtually zero assets, a basic online template might suffice. However, retirees with 401(k)s, real estate, and adult children must seek professional counsel.

For a prenup to be legally binding, most states require both parties to have their own independent legal representation. Using one lawyer for both of you creates a conflict of interest. According to recent data, couples who hire traditional family law attorneys can expect to pay an average of $3,000 to $10,000 combined. While this seems expensive, it is a fraction of what a contested divorce or a protracted probate battle would cost your estate.

Frequently Asked Questions About Prenups for Retirees

Can we create a financial agreement if we are already married?

Yes. If you are already legally married, you can draft a “postnuptial agreement.” It functions exactly like a prenup, outlining the division of assets, debt protection, and inheritance guarantees. Postnups are increasingly popular among older couples who realize they need to clarify their financial boundaries after the wedding.

Does a prenuptial agreement override my will?

A prenup and a will serve different but complementary purposes. Your will dictates where your assets go when you die, while a prenup is a binding contract between you and your spouse. If your will says you leave everything to your kids, but your state law guarantees your spouse an elective share, the state law usually wins. A prenup allows your spouse to waive that state-mandated share, ensuring your will can be executed exactly as written.

Will a prenup protect my assets from Medicaid if my spouse needs a nursing home?

Generally, no. Medicaid is a federal program with strict “spousal impoverishment” rules that look at a couple’s combined assets to determine eligibility, regardless of what a state-level prenup says. While a prenup protects you from private civil medical debt, you must consult an elder law attorney to create specialized Medicaid asset-protection trusts.

Navigating romance and finances in your later years does not have to be stressful. By having honest conversations and utilizing these strategic legal clauses, you can protect your hard-earned assets while building a strong, transparent foundation for your new marriage.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.