Protecting your pension from state taxes leaves you with significantly more spending power each month. While the IRS requires federal taxes on most retirement accounts, your home state dictates whether you face a second layer of taxation. Seven specific states—Florida, Nevada, Wyoming, Pennsylvania, Illinois, Mississippi, and Tennessee—allow you to keep more money by fully exempting pension income. Relocating to one of these destinations can save you thousands of dollars annually, depending on your specific withdrawal rate. However, a zero percent income tax rate does not automatically guarantee a cheaper lifestyle. You must carefully weigh property levies, sales taxes, and the broader cost of living against your potential tax savings to make a smart relocation decision.

The Federal Baseline: Understanding Your Tax Obligations

Before evaluating state-level exemptions, you must understand your federal tax obligations. The federal government taxes most public and private pensions, 401(k) distributions, and traditional IRA withdrawals as ordinary income. Knowing this baseline helps you calculate the true value of state tax exemptions. If you live in a state that mimics the federal tax code, you end up paying a double tax on your retirement distributions.

Recent legislative changes and inflation adjustments have altered the federal tax landscape for retirees. The Internal Revenue Service (IRS) implemented several critical updates that affect how much you pay before state taxes even enter the equation:

- Higher Standard Deductions: For the 2025 tax year, the standard deduction for married couples filing jointly sits at $31,500. Single filers receive a $15,750 standard deduction.

- Age-Based Increases: Taxpayers aged 65 or older claim an additional standard deduction. Married couples receive an extra $1,600 per eligible individual, while single filers receive an additional $2,000.

- New Senior Tax Relief: The recent One Big Beautiful Bill Act (OBBBA) introduced a powerful $6,000 senior deduction per qualifying taxpayer. This pushes the total standard deduction for eligible married couples to $46,700, shielding a massive portion of pension income from federal taxes.

- Social Security Increases: For 2026, the Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA). This pushes the average monthly benefit to roughly $2,064. Furthermore, the maximum taxable earnings limit for Social Security increased to $184,500.

Depending on your combined income, the federal government may tax up to 85% of your Social Security benefits. Since federal taxes remain constant regardless of your zip code, moving to a tax-friendly state serves as one of the most effective strategies to lower your overall lifetime tax burden.

“Someone’s sitting in the shade today because someone planted a tree a long time ago.” — Warren Buffett

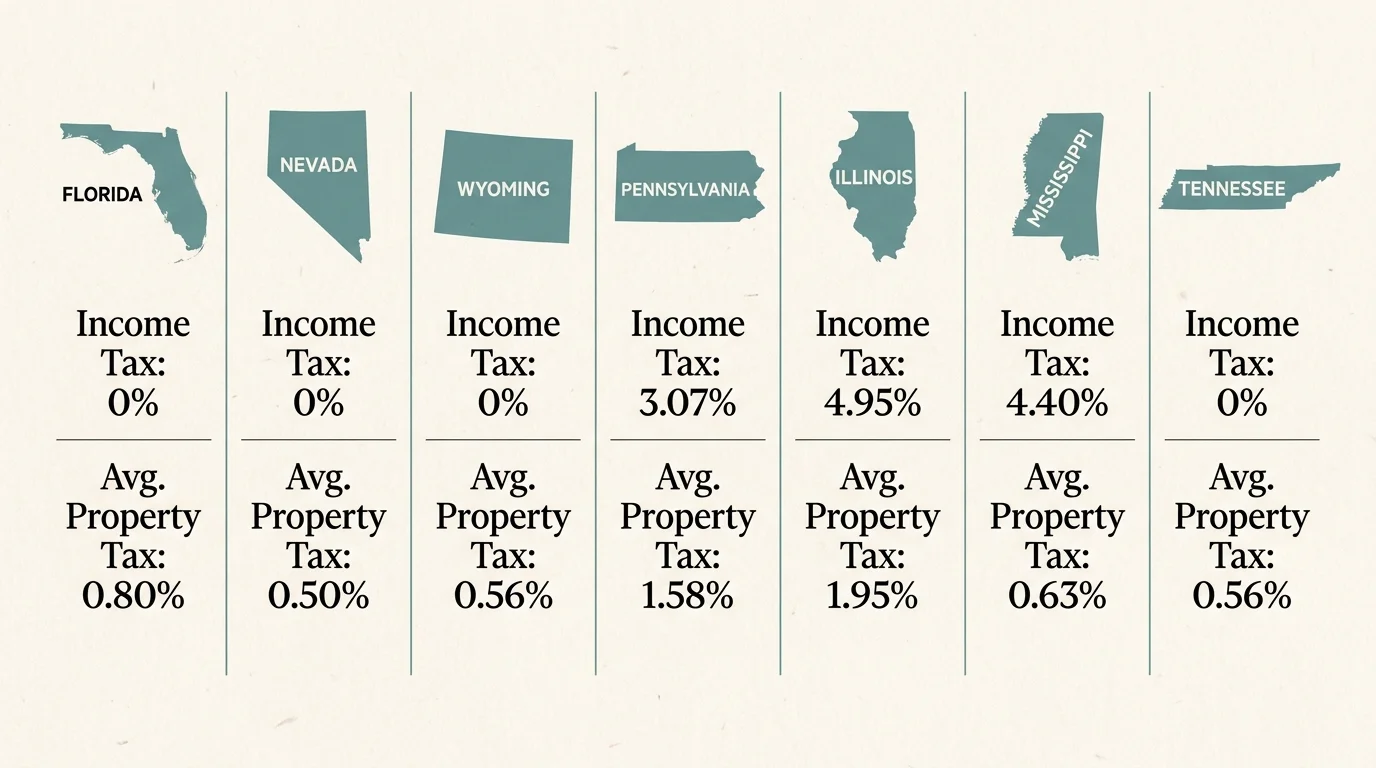

State Comparison at a Glance

To help you weigh your options, the table below highlights the income tax rates, pension tax status, and average property tax rates for seven top retirement destinations.

| State | General Income Tax Rate | Pension Tax Status | Avg. Property Tax Rate |

|---|---|---|---|

| Florida | 0% | Fully Exempt | Moderate (Varies) |

| Nevada | 0% | Fully Exempt | 0.50% |

| Wyoming | 0% | Fully Exempt | 0.56% |

| Pennsylvania | 3.07% | Exempt (Age 59.5+) | Higher than average |

| Illinois | 4.95% | Fully Exempt | 1.95% |

| Mississippi | 4.40% | Fully Exempt | 0.63% |

| Tennessee | 0% | Fully Exempt | Low |

1. Florida: The Benchmark for Tax-Free Retirement

Florida remains the gold standard for retirees, largely due to its aggressive protection of retirement wealth. The state levies no personal income tax whatsoever. You pay zero state tax on your pension, 401(k) withdrawals, traditional IRA distributions, and Social Security benefits. Whether you withdraw $30,000 or $300,000 from your retirement accounts, Florida takes nothing.

The state relies heavily on consumption and property taxes to fund its infrastructure. The base state sales tax stands at 6%, though local municipalities can push that rate up to 7.5%. To protect long-term residents from surging real estate values, Florida offers a generous homestead exemption that reduces your primary home’s assessed value by up to $50,000. Furthermore, the Save Our Homes cap legally restricts annual property tax assessment increases to 3% or the Consumer Price Index, whichever is lower.

Despite the tax advantages, you must budget for localized expenses. Property insurance premiums in coastal areas often consume the money you save on income taxes. You should also anticipate higher homeowner association (HOA) fees if you move into a managed retirement community.

2. Nevada: Keep Your Pension in a Low-Tax Haven

Nevada offers a massive financial draw for retirees looking to escape the high taxes of neighboring California. Like Florida, Nevada applies no state income tax, meaning your pension and Social Security checks remain entirely tax-free.

Nevada separates itself from other no-tax states through exceptionally favorable property tax laws. The state’s average property tax rate sits at just 0.50% of assessed value. To prevent retirees from being priced out of their homes, Nevada state law caps annual property tax assessment increases at a strict 3% for primary residences. You also avoid estate and inheritance taxes entirely.

You fund these tax breaks every time you shop. Nevada relies heavily on the hospitality and retail sectors for revenue. The state sales tax sits at 6.85%, and local add-ons frequently push the combined average sales tax rate to 8.24%. While cities like Reno and Henderson offer excellent healthcare systems, rural Nevada struggles with limited medical access. You must balance the tax savings against your ongoing healthcare needs.

3. Wyoming: Maximum Tax Relief in the West

For retirees who prioritize open spaces over warm winters, Wyoming delivers unmatched tax efficiency. The state charges no personal income tax, leaving your pension, Social Security, and investment income completely untouched.

Wyoming pairs its zero percent income tax with incredibly low holding costs. Property taxes average just 0.56% of assessed value. The state sales tax is among the lowest in the country at a mere 4%. If you plan to leave a legacy to your children, Wyoming makes the process highly efficient by imposing no estate or inheritance tax.

The low cost of living outside resort towns like Jackson Hole allows retirees on fixed pensions to stretch their dollars significantly further. However, the state’s harsh winters and sparse population density mean you may need to travel substantial distances for specialized medical care. Wyoming suits active, independent retirees who want absolute maximum tax relief.

4. Pennsylvania: A Northern Exemption for Seniors

Pennsylvania frequently surprises retirees who assume only Southern states offer tax havens. Pennsylvania runs on a flat 3.07% income tax system. If you take a part-time job or earn rental income, the state taxes those earnings at that 3.07% rate. However, the state provides a massive structural carve-out specifically designed to attract and retain seniors.

Pennsylvania completely exempts pension income, 401(k) distributions, and IRA withdrawals from state taxes, provided you take those distributions after reaching retirement age (or age 59.5 for IRAs). Additionally, the state fully exempts Social Security benefits regardless of your total income. This means a retiree living entirely on Social Security and a traditional pension pays exactly zero dollars in state income tax.

The state also exempts essentials like groceries, clothing, and prescription drugs from its 6% sales tax. The primary financial threat in Pennsylvania involves legacy planning. The state aggressively levies an inheritance tax. While direct descendants pay 4.5%, non-lineal heirs face tax rates up to 15% on inherited assets.

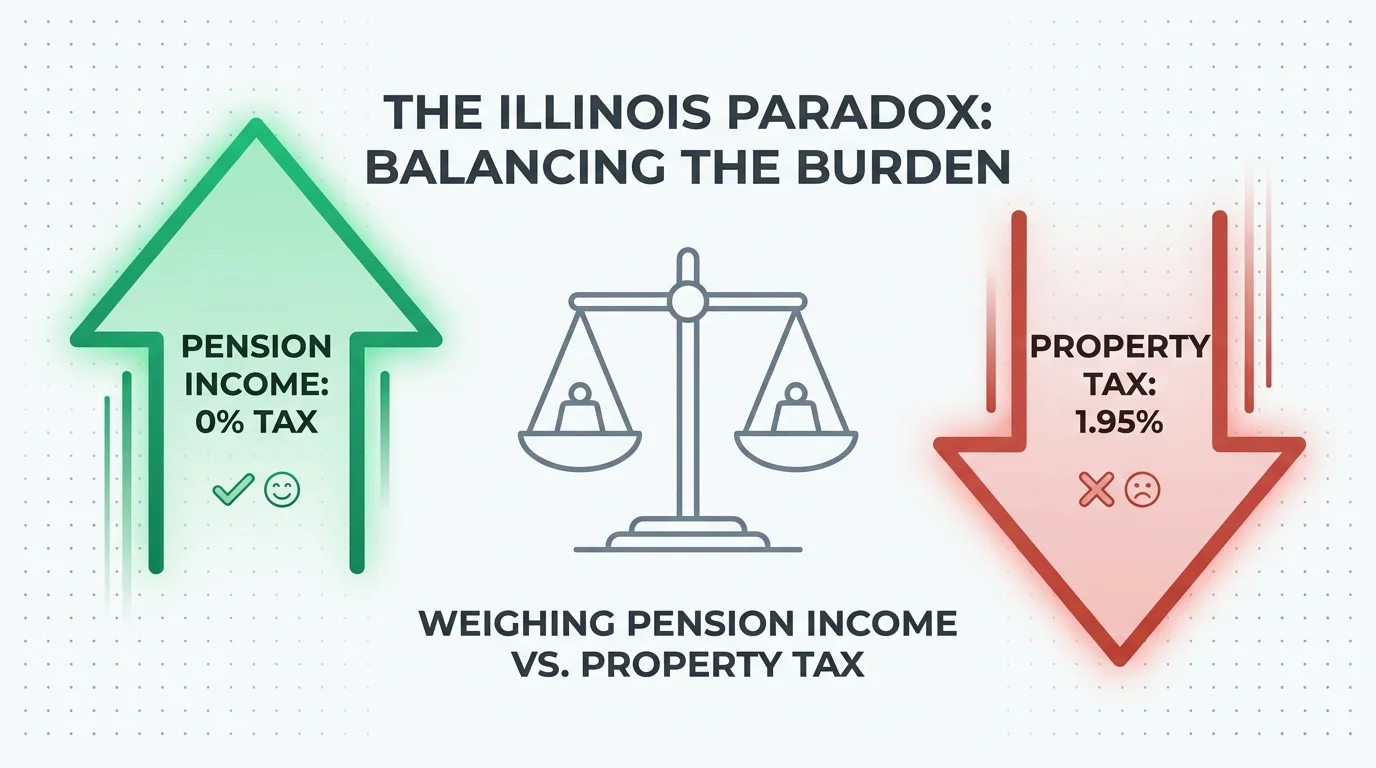

5. Illinois: Broad Exemptions Despite High Property Taxes

Illinois represents another complex but highly rewarding tax environment for retirees. The state utilizes a flat 4.95% income tax rate on general wages and business income. Yet, Illinois stands out as one of the most generous states in the nation regarding retirement accounts.

Illinois fully exempts all qualified retirement income. This exemption covers public pensions, private pensions, 401(k) distributions, IRA withdrawals, and Social Security benefits. Unlike states that cap exemptions based on income thresholds, Illinois allows you to pull massive distributions from your retirement accounts without owing a dime to the state revenue department.

You must remain extremely cautious regarding real estate. Illinois offsets its retirement income exemptions with some of the highest property taxes in the United States, averaging a brutal 1.95% of assessed value. Furthermore, Illinois enforces an estate tax on estates exceeding $4 million. If you plan to rent an apartment, Illinois offers fantastic tax efficiency. If you plan to buy a large home, the property taxes may negate your pension tax savings entirely.

6. Mississippi: The Most Affordable Southern Option

Mississippi combines comprehensive retirement tax exemptions with the lowest overall cost of living in the United States. For the 2025 tax year, Mississippi utilizes a flat 4.40% income tax rate on wages and business earnings. However, the state broadly exempts all qualified retirement income.

If you live in Mississippi, the state takes zero taxes from your pension, IRA distributions, 401(k) withdrawals, or Social Security checks. Military retirees also enjoy full exemptions on their military retirement pay.

Beyond income taxes, Mississippi keeps ongoing costs highly manageable. The effective property tax rate hovers around a mere 0.63%. Homeowners aged 65 or older qualify for a specialized property tax exemption covering the first $7,500 of their home’s assessed value. The state does not levy estate or inheritance taxes. The only notable tax drawback involves the grocery store; Mississippi applies a 5% sales tax to food purchases.

7. Tennessee: Zero Income Tax in the Sunbelt

Tennessee finalized the elimination of its Hall Income Tax (which previously targeted interest and dividends), transitioning into a true zero-income-tax state. Retirees pay absolutely no state tax on pensions, 401(k) distributions, IRAs, or Social Security benefits.

The state continues to attract retirees with its relatively affordable housing markets, four distinct but mild seasons, and strong cultural hubs like Nashville and Memphis. Tennessee also protects your legacy by refusing to levy any estate or inheritance tax.

Because the state cannot rely on income taxes, it leans heavily on retail sales. Tennessee imposes a high state sales tax, and local municipalities frequently add their own percentages. Depending on your county, you may pay nearly 10% in sales tax on major purchases. You must budget carefully for sales taxes if you plan to buy vehicles, furniture, or luxury goods during your retirement years.

“It is not just about the numbers; it’s about the peace of mind and quality of life that comes from financial security in retirement.” — Brennan Rhule, Retirement Tax Researcher

When DIY Isn’t Enough

Relocating across state lines involves complex legal and financial maneuvers. While some retirees can manage a move independently, you should consult a Certified Financial Planner (CFP) or a qualified tax professional if you encounter the following scenarios:

- Splitting Residency: If you plan to spend winters in Florida and summers in New York, you must navigate strict domicile laws. Most states utilize the 183-day rule to determine residency. Claiming a tax-free state as your domicile while spending too much time in a high-tax state frequently triggers painful tax audits.

- Managing Early Pension Withdrawals: State laws differentiate between qualified retirement distributions and early withdrawals. For instance, Pennsylvania aggressively protects pension income, but if you take an early withdrawal before reaching age 59.5, the state may classify that money as taxable compensation.

- Navigating Inheritance Laws: If you relocate to a state like Pennsylvania, you must proactively build a strategy to shield your assets from the 4.5% to 15% inheritance tax. An estate attorney can help you utilize trusts to bypass these aggressive levies.

Avoiding Common Relocation Errors

Moving for tax benefits requires a holistic view of your finances. Do not let a zero percent income tax rate blind you to other structural costs. Financial industry regulators consistently warn against making major life changes based on a single data point. Avoid these frequent missteps:

- Ignoring the Total Tax Burden: Eliminating a 5% state income tax means nothing if you move to an area where property taxes and homeowner’s insurance premiums double. Always calculate your “effective tax rate,” which includes income, property, sales, and localized excise taxes.

- Misunderstanding Out-of-State Pensions: Thanks to federal legislation passed in 1996, your former state cannot tax your pension once you establish a new legal domicile elsewhere. However, you must proactively file updated withholding forms with your pension administrator. If you fail to update your status, your former state will continue pulling taxes from your monthly checks.

- Working Part-Time in Retirement: States like Illinois and Pennsylvania offer incredible tax breaks for passive pension income, but they do not extend those breaks to active wages. If you plan to consult or work part-time, states will fully tax those earnings at their standard flat rates.

Frequently Asked Questions

Do these states tax Social Security benefits?

None of the seven states listed above tax Social Security benefits. In fact, as of 2026, 38 states and Washington D.C. fully exempt Social Security from state income taxes. You only face state taxes on Social Security in a small minority of jurisdictions.

Does moving to a tax-free state lower my federal taxes?

No. Your physical zip code does not alter your federal tax bracket or your Medicare obligations. If you earn above specific thresholds, the IRS will still tax up to 85% of your Social Security benefits. Furthermore, standard Medicare Part B premiums—which increased to $202.90 per month in 2026—apply universally regardless of where you live.

Are military pensions treated differently?

Yes. Many states that normally tax private pensions offer deep carve-outs for veterans. States like Mississippi fully exempt military retirement pay from state income taxes, ensuring veterans keep the entirety of their benefits. Always check specific military exemptions before deciding on a retirement destination.

Choosing where to spend your retirement years requires a careful balancing act between financial efficiency and personal comfort. While eliminating state taxes on your pension rapidly accelerates your wealth preservation, you must ensure your destination provides the healthcare access, community, and lifestyle you desire. Take the time to visit these states, run the math on your specific withdrawal rates, and build a retirement plan that offers both prosperity and peace of mind.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.