You might picture retirement as an endless weekend, but the reality for millions of Americans looks entirely different. A quiet but massive shift is reshaping the workforce, as older adults trade their leisure time for a return to the time clock, the gig economy, or the consulting firm.

According to a February 2026 survey by AARP, 7% of retirees have reentered the labor force in the past six months alone. Another January 2026 study from ResumeBuilder found that 1 in 8 seniors have either already returned to work or plan to rejoin the workforce this year. This growing movement—often dubbed “unretiring”—is driven by a complex mix of financial pressures, changing lifestyle expectations, and a tight labor market that desperately needs experienced talent.

Whether you want to pad your savings account, cover rising healthcare costs, or simply find a sense of purpose and social connection, returning to work can be incredibly rewarding. However, taking on a new job in your sixties or seventies triggers a domino effect across your entire financial life. Extra income impacts your tax bracket, your Social Security benefits, and even the premiums you pay for Medicare.

If you are considering dusting off your resume or downloading a gig-work app, you need a clear strategy. Navigating the rules surrounding earned income in retirement requires precision. Here is exactly what you need to know about the unretirement trend, the hidden tax traps to avoid, and how to maximize the money you bring home.

The Essentials: What to Know Before You Return to Work

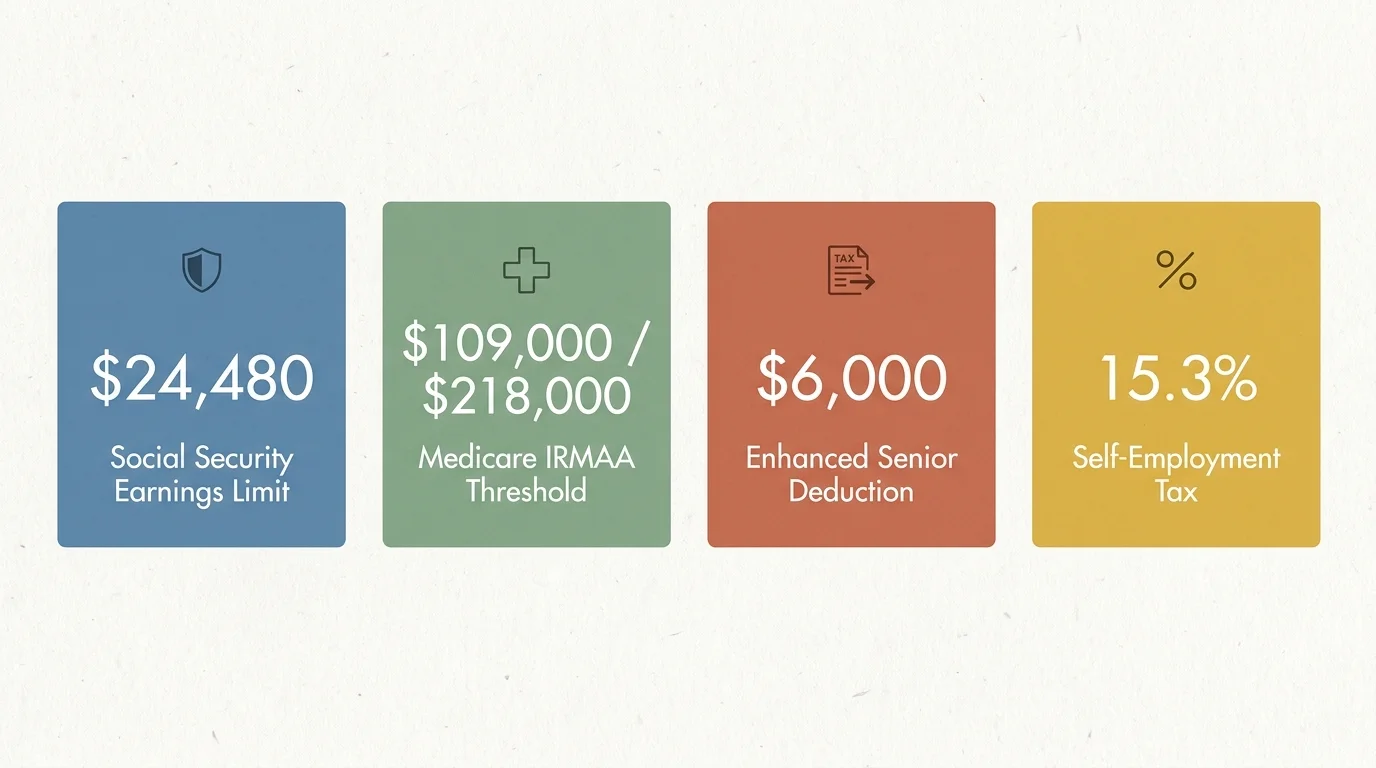

- Social Security limits apply: If you collect benefits before your Full Retirement Age (FRA), earning more than $24,480 in 2026 triggers benefit withholding.

- Medicare premiums could spike: Earning extra money might push your income over the 2026 threshold of $109,000 for singles or $218,000 for couples, triggering costly Medicare Part B and Part D surcharges known as IRMAA.

- New tax benefits are available: The tax landscape for seniors has shifted; the IRS standard deduction increased for 2026, and a new $6,000 enhanced senior deduction helps shelter more of your income if you meet the criteria,.

- Self-employment taxes still exist: If you take on gig work or consulting, you owe a 15.3% self-employment tax on your net earnings, regardless of your age.

The Driving Forces Behind the Unretirement Trend

The decision to unretire is rarely made on a whim. For decades, the traditional American retirement model involved working until 65 and then relying on a three-legged stool of pensions, personal savings, and Social Security. Today, that stool is notoriously wobbly. Pensions have largely vanished in favor of 401(k)s, placing the burden of market risk entirely on the retiree. When stock market volatility meets persistent inflation, many older adults feel their nest eggs are insufficient.

Financial necessity is undeniably the primary catalyst for unretiring. According to the 2026 AARP data, 48% of older adults reentering the labor force explicitly state that making money is their primary motivation, driven heavily by basic living expenses. Another study noted that 41% of older adults feel they cannot currently support their ideal retirement lifestyle without supplemental income. When grocery bills, property taxes, and utility costs rise faster than your fixed income, picking up a part-time job becomes the most reliable safety valve.

Yet, money is not the only motivator. Approximately 14% of returning workers tell researchers they go back primarily to stay active. The abrupt transition from a busy, socially engaging career to a completely unstructured retirement can lead to profound isolation. Many unretirees discover that work provides a vital sense of identity, intellectual stimulation, and community that golf or gardening simply cannot replace.

“Retirement is not a finish line, it is a transition. For many, work provides the structure, purpose, and social connection that a purely leisure-focused retirement lacks.” — Jean Chatzky, Financial Editor and Author

The Landscape of Post-Retirement Work

If you decide to return to work, you will find that the modern labor market offers far more flexibility than it did twenty years ago. You no longer have to commit to a traditional 9-to-5 schedule to earn a meaningful income. The 2026 job market for seniors is defined by choice, adaptability, and the rise of the gig economy.

Gig work has exploded in popularity among retirees because it provides ultimate control over your schedule. According to labor market analyses, seniors are increasingly driving for rideshare platforms, delivering groceries, and utilizing freelance platforms to offer administrative support. If you want to work three hours on a Tuesday and take the rest of the week off to visit your grandchildren, app-based platforms allow you to do exactly that.

Beyond app-based jobs, many retirees are leveraging their decades of professional experience to pivot into consulting or tutoring. Companies are actively struggling with a loss of institutional knowledge as the Baby Boomer generation exits the workforce en masse. Many employers are eager to hire former executives, engineers, and managers as part-time consultants. This arrangement allows you to command a high hourly rate without dealing with corporate politics, mandatory meetings, or rigid vacation policies.

More traditional roles remain popular as well. Retailers, garden centers, and hardware stores frequently recruit older workers for their reliability, deep product knowledge, and exceptional customer service skills. Specialized roles, such as pet sitting, freelance bookkeeping, and household organizing, are also incredibly lucrative niches for older adults who want to operate small, low-stress local businesses.

Navigating the Social Security Earnings Test

One of the most critical factors to evaluate before you accept a job offer is how your wages will impact your Social Security benefits. The Social Security Administration enforces strict rules regarding earned income for those who claim benefits early.

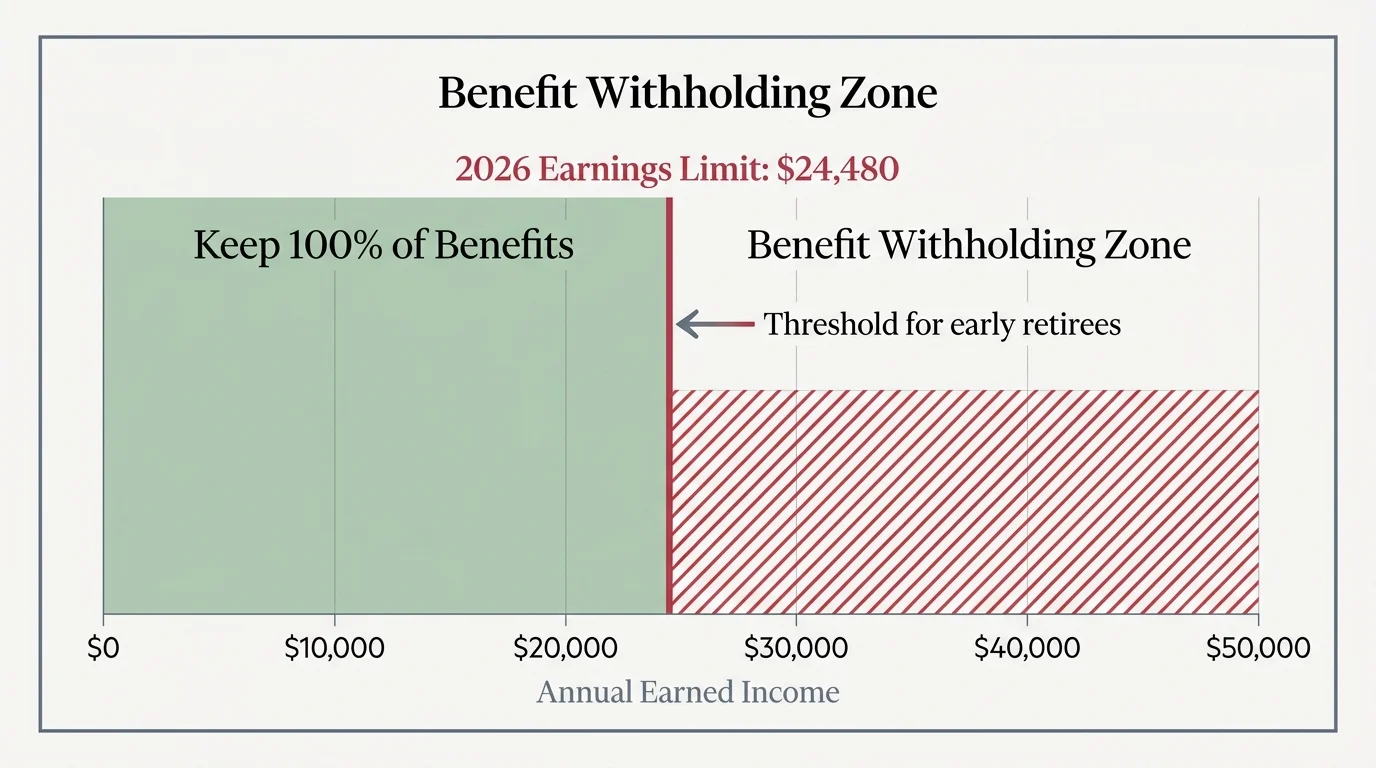

When you begin receiving Social Security retirement benefits, you are considered retired by the government. However, the SSA allows you to work and receive benefits simultaneously—subject to the earnings test. If you have not yet reached your Full Retirement Age (FRA), your earned income is capped. Exceeding this cap results in the temporary withholding of your benefits.

For 2026, if you remain under your Full Retirement Age for the entire year, the annual earnings limit is $24,480. If you earn more than this amount, the SSA will deduct $1 from your benefit payments for every $2 you earn above the threshold.

The rules change favorably during the calendar year you actually reach your Full Retirement Age. In 2026, the limit jumps significantly to $65,160 for the months prior to your birth month. If you exceed this higher limit, the penalty drops as well; the government only withholds $1 for every $3 you earn above the threshold.

| Your Age Status in 2026 | Annual Earnings Limit | Benefit Withholding Penalty |

|---|---|---|

| Under Full Retirement Age all year | $24,480 | $1 withheld for every $2 above limit |

| Reaching Full Retirement Age this year | $65,160 (counts only earnings before birth month) | $1 withheld for every $3 above limit |

| At or past Full Retirement Age | No limit | No benefits withheld |

It is vital to understand that the earnings test only applies to wages from a job or your net earnings from self-employment. Investment income, pension payments, annuities, and capital gains do not count toward these limits.

Furthermore, the benefits withheld by the SSA are not gone forever. Once you reach your Full Retirement Age, the SSA recalculates your monthly payment upward to account for the months your benefits were withheld. Over your remaining lifetime, you will gradually recoup those lost dollars.

Does Returning to Work Increase Your Social Security Benefit?

Many retirees are surprised to learn that going back to work can actually permanently increase their monthly Social Security checks. The SSA calculates your retirement benefit based on your highest 35 years of indexed earnings. If you go back to work and your new salary is higher than one of the lowest-earning years used in your original calculation, the SSA will automatically drop the low year, substitute the new high year, and increase your benefit amount.

This recalculation happens automatically each year as long as you continue to pay Social Security payroll taxes. If you had several years of zero or low income earlier in your career, working part-time in your late sixties could provide a permanent boost to your guaranteed lifetime income.

The Tax Bite: What You Keep vs. What You Earn

Many retirees assume that once they stop working full-time, their tax headaches disappear. Returning to the workforce quickly shatters that illusion. The moment you start earning wages or gig income again, you invite the Internal Revenue Service back into your financial life.

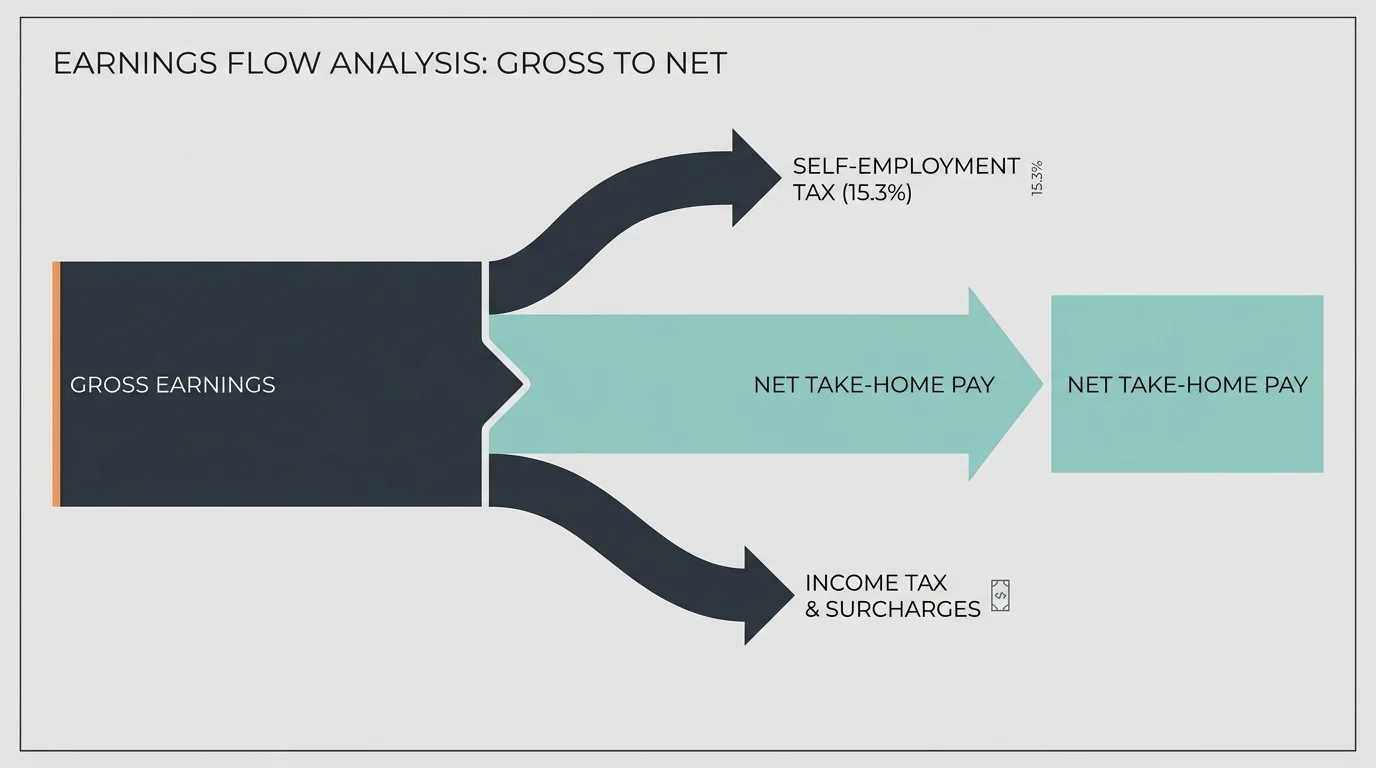

First, you must resume paying FICA taxes (Social Security and Medicare). If you are a traditional W-2 employee, your employer will deduct 7.65% from your paycheck. The Social Security tax limit in 2026 is $184,500, meaning you pay Social Security taxes on all wages up to that cap, while the 1.45% Medicare tax applies to all your earnings with no maximum limit,.

If you choose to work as an independent contractor, consultant, or gig worker, the tax burden is significantly heavier. Self-employed individuals are responsible for both the employee and employer portions of FICA taxes. This means you will owe a 15.3% self-employment tax on your net earnings above $400. This tax is calculated in addition to your standard federal and state income taxes. Because no employer is withholding taxes on your behalf, you must diligently set aside a portion of your earnings and make quarterly estimated tax payments to avoid IRS penalties.

Earning extra income can also trigger the taxation of your Social Security benefits. The IRS determines the taxability of your benefits using a metric called “provisional income.” You calculate provisional income by adding your Adjusted Gross Income, your non-taxable interest, and exactly half of your Social Security benefits. If your provisional income exceeds $34,000 as a single filer or $44,000 as a married couple, up to 85% of your Social Security benefits become taxable at your standard federal income tax rate. A new part-time job can easily push a modest, tax-free retirement into this heavily taxed zone.

Fortunately, the tax code also offers substantial protections for older workers. The standard deduction in 2026 has increased to $16,100 for single filers and $32,200 for married couples filing jointly. Furthermore, taxpayers age 65 and older receive an additional standard deduction of $2,050 for singles and $1,650 for married taxpayers (per qualifying spouse).

Most notably, recent tax legislation known as the One Big Beautiful Bill Act (OBBBA) introduced an exceptional new tax break for seniors. Effective for tax years 2025 through 2028, individuals age 65 and older can claim an additional $6,000 deduction on top of the standard deduction. A married couple who are both 65 or older can claim up to $12,000. However, this new deduction comes with strict phase-outs. If your modified adjusted gross income exceeds $75,000 for singles or $150,000 for joint filers, the deduction begins to phase out. Going back to work requires careful income management so you do not accidentally earn your way out of this valuable tax break.

“The biggest threat to a secure retirement is taxes. Earning extra income is great, but if it pushes you into an invisible tax trap like IRMAA or increases the tax on your Social Security benefits, you could end up working just to pay the IRS.” — Ed Slott, CPA and Retirement Tax Expert

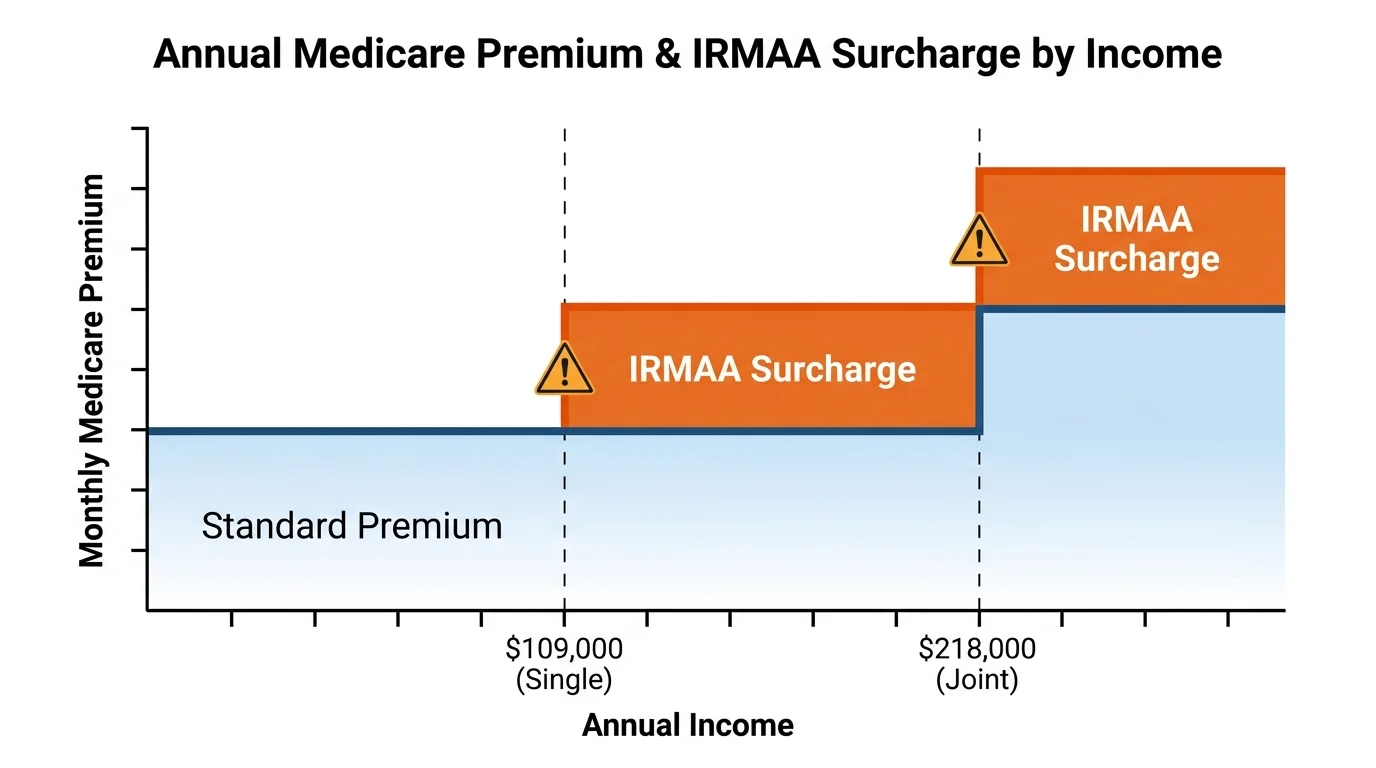

Medicare and the IRMAA Trap

Healthcare costs are a significant driver of the unretirement trend, but returning to work can paradoxically increase the cost of your Medicare coverage. If your income exceeds specific thresholds, the government imposes a surcharge on your Medicare Part B and Part D premiums. This surcharge is known as the Income-Related Monthly Adjustment Amount, or IRMAA.

In 2026, the standard Medicare Part B premium is $202.90 per month, with an annual deductible of $283. However, the Centers for Medicare and Medicaid Services estimate that about 8% of beneficiaries pay higher, income-adjusted premiums.

IRMAA functions as a hidden tax on successful retirees. Medicare uses your Modified Adjusted Gross Income (MAGI) from two years prior to determine your current premium. This means your 2026 Medicare premiums are based on the income reported on your 2024 tax return. If you go back to work today, the income you earn in 2026 will dictate your Medicare premiums in 2028.

The IRMAA brackets operate as hard cliffs. Earning just one dollar over a threshold pushes you entirely into the next bracket, dramatically increasing your monthly healthcare costs. Here are the 2026 Medicare Part B IRMAA brackets based on your tax filing status:

- Tier 1 (Base Premium): MAGI of $109,000 or less (single) or $218,000 or less (joint). You pay the standard $202.90 per month.

- Tier 2: MAGI between $109,001 and $137,000 (single) or $218,001 and $274,000 (joint). Your Part B premium rises to $284.10 per month.

- Tier 3: MAGI between $137,001 and $171,000 (single) or $274,001 and $342,000 (joint). Your Part B premium rises to $405.80 per month.

- Tier 4: MAGI between $171,001 and $205,000 (single) or $342,001 and $410,000 (joint). Your Part B premium rises to $527.50 per month.

- Tier 5: MAGI between $205,001 and $499,999 (single) or $410,001 and $749,999 (joint). Your Part B premium rises to $649.20 per month.

- Tier 6: MAGI of $500,000 or more (single) or $750,000 or more (joint). Your Part B premium caps out at $689.90 per month.

Keep in mind that these surcharges apply to Medicare Part D (prescription drug coverage) as well. In 2026, the Part D IRMAA surcharges range from an additional $14.50 to $91.00 per month, applied on top of your base plan premium.

Evaluating Your Healthcare Options

If your return to the workforce includes an offer for comprehensive employer-sponsored health insurance, you face an important decision regarding your Medicare enrollment.

If your employer has 20 or more employees, the group health plan generally becomes your primary insurance, and Medicare acts as a secondary payer. In this scenario, you may choose to drop Medicare Part B to save on the $202.90 monthly premium, knowing you can re-enroll during a Special Enrollment Period once you stop working. However, if your employer has fewer than 20 employees, Medicare typically remains your primary coverage, and dropping Part B would leave you dangerously uninsured. Always coordinate closely with your employer’s human resources department and the Social Security Administration before canceling any Medicare coverage.

Avoiding Common Errors

Returning to work alters your financial ecosystem. Without careful planning, you can easily fall into costly traps. Protect your income by avoiding these widespread mistakes:

- Failing to Remit Quarterly Estimated Taxes: If you pivot into gig work or consulting, you are now a business owner in the eyes of the IRS. Waiting until April to pay your 15.3% self-employment tax and income tax can result in massive underpayment penalties. You must calculate and submit estimated tax payments four times a year.

- Misunderstanding the IRMAA Lookback Period: Many retirees celebrate a high-paying consulting contract in 2026, spend the money in 2027, and are utterly shocked when their Social Security checks are slashed in 2028 to cover IRMAA surcharges. You must plan for the two-year delay between earning the income and paying the premium.

- Forgetting About Required Minimum Distributions (RMDs): If you are over age 73, you are legally required to withdraw money from your traditional IRAs and 401(k)s. When you combine mandatory taxable withdrawals with your new part-time salary, you can easily blast through the IRMAA thresholds and into a much higher federal tax bracket.

When DIY Isn’t Enough

Managing a few extra thousand dollars from a seasonal retail job is generally straightforward. However, modern unretirement often involves complex income streams. You should consult a qualified financial planner or tax professional in the following scenarios:

- Navigating the Widow’s Penalty: When a spouse passes away, the survivor transitions from married filing jointly to single filing status. This drastically lowers the IRMAA threshold from $218,000 down to $109,000 in 2026. The loss of a spouse combined with continuing work income often pushes the survivor into a brutal tax and Medicare surcharge trap. Professional planning is crucial to mitigate this blow.

- Structuring a Consulting Business: If your former employer hires you back as an independent contractor, you must navigate self-employment taxes, business deductions, and potential SEP IRA or Solo 401(k) contributions. A CPA can ensure your business entity is structured optimally to legally shield as much income as possible.

- Managing High Taxable Income: If you must take RMDs while simultaneously earning a salary, professionals can help deploy tax-mitigation strategies. They may advise you to utilize Qualified Charitable Distributions (QCDs) to satisfy your RMD without adding to your Adjusted Gross Income, effectively keeping you under the IRMAA phase-outs and protecting your $6,000 OBBBA senior tax deduction.

Frequently Asked Questions

Do I still pay Social Security and Medicare taxes if I work after retirement?

Yes. FICA taxes (Social Security and Medicare payroll taxes) apply to your earned income regardless of your age or whether you are already drawing Social Security benefits. As a W-2 employee, 7.65% is deducted from your paycheck. If you are self-employed, you must pay the full 15.3% self-employment tax.

Are my withheld Social Security benefits gone forever if I exceed the earnings limit?

No. If the Social Security Administration withholds a portion of your benefits because you earned over the 2026 limit of $24,480 (or $65,160 in the year you reach FRA), those funds are not lost. Once you reach your Full Retirement Age, the SSA will recalculate your monthly payment upward to account for the months your benefits were withheld.

Does my spouse’s income count toward my Medicare IRMAA surcharge?

Yes. If you file your taxes as Married Filing Jointly, Medicare looks at your combined Modified Adjusted Gross Income. If your spouse takes a high-paying job, it could trigger IRMAA surcharges for both of you, increasing the Medicare Part B and Part D premiums for your entire household,.

Can I pause my Social Security benefits if I go back to work?

If you have reached your Full Retirement Age but are not yet 70, you have the option to voluntarily suspend your Social Security benefits. While suspended, your benefits earn delayed retirement credits of 8% per year, permanently increasing your future monthly payouts. This is an excellent strategy if a new job provides enough income to cover your living expenses.

Returning to work in your senior years is a powerful way to enhance your financial security, retain your mental sharpness, and build social connections. By understanding the rules surrounding Social Security limits, tax brackets, and Medicare premiums, you can confidently accept that job offer or launch your consulting business without surrendering your hard-earned money to the IRS.

Take the time to project your total income, calculate your exact tax liabilities, and consult a professional if your situation involves self-employment or significant retirement account withdrawals. The unretirement trend offers incredible opportunities, provided you navigate the financial details with your eyes wide open.

Last updated: April 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources. The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.