Understanding Healthcare and Taxes Overseas

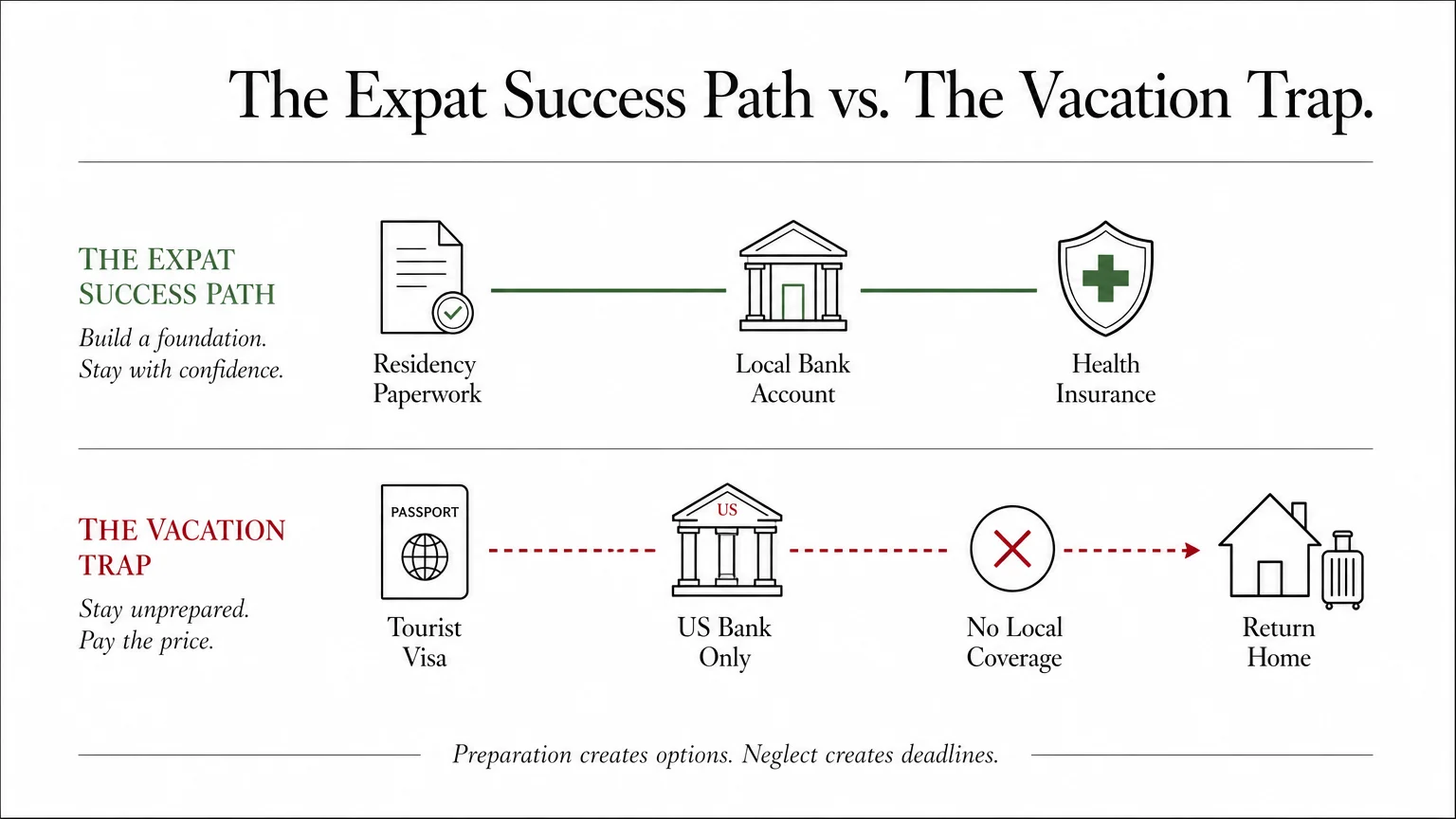

Managing your money and your health represent the two largest hurdles when moving abroad. First, understand how your current benefits translate internationally. The Social Security Administration (SSA) allows you to receive your monthly retirement benefits in most countries worldwide. You can even set up direct deposit with international banks in many participating nations, ensuring a seamless income stream.

However, your domestic health coverage does not follow you. As clearly outlined by Medicare.gov, Medicare generally provides zero coverage for medical care received outside the United States.

You will need to either purchase a comprehensive international health insurance policy or buy into your new country’s national public healthcare system. Many expats maintain Medicare Part B just in case they decide to return to the US for a major surgery, though this adds a significant monthly expense to the budget.

Finally, moving abroad does not sever your relationship with the tax man. The Internal Revenue Service (IRS) requires all United States citizens to file annual tax returns and report global income, regardless of where they reside. While tools like the Foreign Earned Income Exclusion or Foreign Tax Credits often prevent double taxation, the reporting requirements—including the mandatory declaration of foreign bank accounts (FBAR)—remain strict.

What Can Go Wrong: Common Expat Retirement Mistakes

Transitioning to a foreign country involves a massive learning curve. Avoid these common pitfalls to ensure your international retirement thrives rather than flounders:

- Buying property immediately: Never buy a home before living in a country for at least a year. Renting allows you to understand the neighborhoods, weather patterns, and local infrastructure without tying up your liquidity. If the location is not a good fit, a lease is much easier to break than a house is to sell.

- Underestimating the emotional toll: Culture shock is real. The honeymoon phase of a new country eventually fades, revealing the frustrations of foreign bureaucracy, language barriers, and missing major family milestones back home.

- Ignoring currency fluctuations: If your income is in US dollars but your expenses are in Euros or Pesos, exchange rate shifts dictate your purchasing power. A 15 percent drop in the dollar’s value instantly increases your cost of living by 15 percent.

- Assuming things work like they do at home: Plumbers may not show up on time, the internet might drop during rainstorms, and banking can involve mountains of paperwork. Flexibility and patience serve as your most valuable assets.